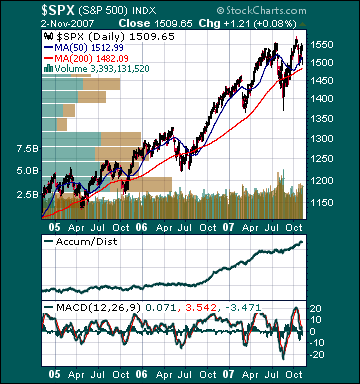

S&P 500 1,509.65 -1.67%*

*5-Day Change

Indices

S&P 500 1,509.65 -1.67%

DJIA 13,595.10 -1.53%

NASDAQ 2,810.38 +.22%

Russell 2000 797.78 -2.87%

Wilshire 5000 15,194.27 -1.63%

Russell 1000 Growth 629.14 -.24%

Russell 1000 Value 820.02 -2.97%

Morgan Stanley Consumer 737.33 -.78%

Morgan Stanley Cyclical 1,044.66 -.92%

Morgan Stanley Technology 673.42 +.60%

Transports 4,802.75 -1.32%

Utilities 525.84 +.62%

MSCI Emerging Markets 160.98 -.52%

Sentiment/Internals

NYSE Cumulative A/D Line 69,033 +.41%

Bloomberg New Highs-Lows Index -197 -3,183%

Bloomberg Crude Oil % Bulls 60.0 +43.2%

CFTC Oil Large Speculative Longs 246,342 +.99%

Total Put/Call 1.15 +42.0%

NYSE Arms 1.11 +89.47%

Volatility(VIX) 23.01 +18.0%

ISE Sentiment 136.0 -15.72%

AAII % Bulls 44.7 +43.1%

AAII % Bears 36.5 -24.3%

Futures Spot Prices

Crude Oil 95.98 +4.59%

Reformulated Gasoline 243.85 +7.45%

Natural Gas 8.38 +7.99%

Heating Oil 257.02 +5.1%

Gold 809.80 +2.74%

Base Metals 245.84 -1.23%

Copper 335.95 -6.07%

Economy

10-year US Treasury Yield 4.32% -8 basis points

4-Wk MA of Jobless Claims 327,000 +.5%

Average 30-year Mortgage Rate 6.26% -7 basis points

Weekly Mortgage Applications 681.70 +3.84%

Weekly Retail Sales +2.2%

Nationwide Gas $2.94/gallon +.12/gallon

US Heating Demand Next 7 Days 4% below normal

ECRI Weekly Leading Economic Index 139.40 -.21%

US Dollar Index 76.27 -.90%

CRB Index 353.57 +2.23%

Best Performing Style

Large-cap Growth -.24%

Worst Performing Style

Small-cap Value -4.0%

Leading Sectors

Software +4.4%

Gold +4.11%

Disk Drives +2.8%

Defense +1.4%

Computer Hardware +1.0%

Lagging Sectors

Insurance -4.0%

Homebuilders -4.63%

Steel -4.2%

Banks -6.7%

Coal -7.49%

- The Change in Non-farm Payrolls for October was 166K versus estimates of 85K and 96K in September.

- The Unemployment Rate for October was 4.7% versus estimates of 4.7% and 4.7% in September.

- Average Hourly Earnings for October rose .2% versus estimates of a .3% gain and a .3% increase in September.

- Factory Orders for September rose .2% versus estimates of a .7% decline and a 3.5% decline in August.

BOTTOM LINE: American employers added almost twice as many jobs as forecast in October, Bloomberg reported. The unemployment rate held at a historically low 4.7%. Service industries, which includes banks, insurance companies, restaurants and retailers, added 190,000 jobs. Average Hourly Earnings rose 3.8%, which is very high by historic stands and almost twice most measures of inflation. For two years, we have been hearing that the housing downturn would lead to imminent massive job loss, and there remains little evidence of this. Fed fund futures now imply a 72% chance for another 25 basis-point-cut at the upcoming December meeting, up from a 60% chance yesterday. I continue to believe the

Orders to US factories unexpectedly rose in September, suggesting companies remain confident the economy will continue to grow, Bloomberg reported. Excluding transports, demand jumped 1.4%. Bookings for capital goods excluding aircraft and military equipment, a measure of future business investment, rose .6% versus a .1% gain in August. Manufacturers had enough goods on hand to last 1.24 months, the same as the prior month. I continue to believe manufacturing will help boost overall

Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes