Click here for The Week Ahead by Reuters

Click here for Stocks in Focus for Tuesday by MarketWatchEconomic Calendar

Earnings Calendar

Conference Calendar

Click here for The Week Ahead by Reuters

Click here for Stocks in Focus for Tuesday by MarketWatchIndices

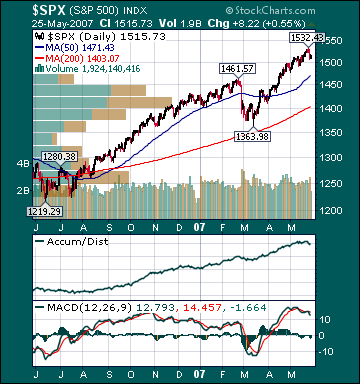

S&P 500 1,515.73 -.46%

DJIA 13,507.28 -.36%

NASDAQ 2,557.19 -.05%

Russell 2000 829.93 +.76%

Wilshire 5000 15,243.28 -.29%

Russell 1000 Growth 595.82 -.27%

Russell 1000 Value 873.61 -.55%

Morgan Stanley Consumer 743.97 -.28%

Morgan Stanley Cyclical 1,060.21 -.48%

Morgan Stanley Technology 608.42 -.24%

Transports 5,147.58 -1.27%

Utilities 512.63 -3.89%

MSCI Emerging Markets 125.54 -.67%

Sentiment/Internals

NYSE Cumulative A/D Line 76,093 -.63%

Bloomberg New Highs-Lows Index +93 -77.6%

Bloomberg Crude Oil % Bulls 36.0 -28.0%

CFTC Oil Large Speculative Longs 175,892 -8.52%

Total Put/Call 1.02 +5.2%

NYSE Arms .82 +43.86%

Volatility(VIX) 13.34 +4.5%

ISE Sentiment 117.0 -9.3%

AAII % Bulls 37.35 -2.71%

AAII % Bears 38.55 +5.30%

Futures Spot Prices

Crude Oil 65.20 -1.21%

Reformulated Gasoline 240.37 +.13%

Natural Gas 7.64 -3.41%

Heating Oil 193.91 +1.23%

Gold 661.40 -.94%

Base Metals 261.23 -1.02%

Copper 332.05 5 +.01%

Economy

10-year US Treasury Yield 4.86% +5 basis points

4-Wk MA of Jobless Claims 302,800 -1.1%

Average 30-year Mortgage Rate 6.37% +16 basis points

Weekly Mortgage Applications 686.20 +1.58%

Weekly Retail Sales +2.3%

Nationwide Gas $3.23/gallon +.07/gallon

US Heating Demand Next 7 Days 58% below normal

ECRI Weekly Leading Economic Index 142.40 -.14%

US Dollar Index 82.33 +.16%

CRB Index 313.10 -.02%

Leading Sectors

Gaming +3.73%

Alternative Energy +2.25%

Homebuilders +1.95%

Wireless +1.19%

Medical Equipments +1.05%

Lagging Sectors

Gold -1.61%

Steel -1.72%

Road & Rail -2.01%

Semis -2.27%

Utilities -3.89%

BOTTOM LINE: The Portfolio is higher into the final hour on gains in my Internet longs, Retail longs, Medical longs and Computer longs. I covered some of my (EEM) short, all of my (IWM)/(QQQQ) hedges, added (AMSC) long and added to a few shorts this morning, thus leaving the Portfolio 100% net long. The tone of the market is positive as the advance/decline line is higher, most sectors are higher and volume is light. Dow Jones is reporting that the April Comscore data shows that Google (GOOG) has 49.7% share of the search engine market vs. 48.3% in March. As well, Yahoo!'s (YHOO) share fell to 26.8% vs. 27.5% in March. Microsoft's (MSFT) share fell to 10.3% from 10.9% in March. In my opinion, it is beyond comprehension why investors are willing to pay 50x forward earnings estimates for YHOO and only 32x conservative forward estimates for GOOG. I continue to believe that investors dramatically underestimate how long GOOG can grow at relatively high rates. I still expect the stock to rise substantially from current levels as it exceeds conservative long-term estimates and the P/E multiple expands significantly. Google remains my largest long position, just ahead of Apple Inc.(AAPL). Yesterday after the close, the Nasdaq reported that short interest on the exchange surged another 5.1% to 8,400,000,000 shares, from mid April through mid May, hitting another all-time high. Moreover, like the NYSE, the last three months have see Nasdaq short interest soar 22%, the largest three-month percentage increase since at least 1991, according to Bloomberg data. The bullish implications of such a large surge in short interest are severely underestimated, in my opinion.

Here are the 20 Nasdaq stocks with the largest percentage increase in their short interest relative to their float from mid-April through mid-May:

1. USNA +32.6%

2. INWK +21.1%

3. CPLP +21.1%

4. CCRT +16.6%

5. IDMI +13.2%

6. OUTD +10.8%

7. MOVI +10.2%

8. IDSA +9.9%

9. SCRX +8.9%

10. MNTA +8.6%

11. MDTL +8.5%

12. NRMX +7.7%

13. DNDN +7.7%

14. UTHR +7.6%

15. MDII +7.5%

16. AVTR +7.4%

17. HERO +7.4%

18. PPCO +7.3%

19. ILMN +7.2%

20. TZIX +7.0%

The S&P 500 also reported data. Here are the five industries in the S&P 500 with the largest percentage increase in their short interest from mid April through mid May:

1. Telcom Services +25.6%

2. Consumer Services +23.2%

3. Food & Staples Retailing +23.0%

4. Insurance +21.8%

5. Real Estate +20.1%

Here are the 20 S&P 500 stocks with the largest percentage increase in their short interest relative to their float from mid April through mid May:

1. STZ + 6.9%

2. VLO +6.7%

3. AMD +5.1%

4. BOL +4.1%

5. WFMI +3.2%

6. FDO +3.1%

7. CVS +3.0%

8. JDSU +2.6%

9. BIG +2.6%

10. ABK +2.6%

11. VMC +2.5%

12. RF +2.5%

13. HCR +2.4%

14. JNS +2.3%

15. CMCSA +2.3%

16. MMC +2.3%

17. RDC +2.2%

18. NVLS +2.2%

19. BTU +2.1%

20. AMZN +2.0%

Bloomberg:

- Coca-Cola Co.(KO) agreed to buy the maker of Glaceau Vitaminwater for $4.1 billion to narrow the gap with PepsiCo Inc. in sales of noncarbonated drinks.

- A plan to screen every American for HIV is set to receive $45 million in funding, raising hopes of improved AIDS prevention and boosting the outlook of testing companies.

- Venezuelan President Hugo Chavez’s pledge to withdraw from the International Monetary Fund may violate terms of the country’s foreign bonds, allowing investors to demand their money back.

- Shares of Archstone-Smith Trust(ASN), the second-largest

- GM and Delphi Corp. management and investors are nearing an agreement with the United Auto Workers that would defuse a strike threat at the former GM auto-parts unit.

- The US dollar headed for a fourth straight weekly gain versus the euro as signs of a recovery in the

- China’s oil imports from Sudan soared over 600% in April amid increased international pressure to cut economic support for the African nation, accused by the US of supporting genocide.

Wall Street Journal:

- A proposed US Senate bill would require utilities to generate 15% of their power from wind, the sun, and other cleaner energy sources by 2020. The amount compares with about 2% currently. The measure has bipartisan support and is backed by environmental groups.

- Chinese imports of copper slowed in April from the previous month’s record pace amid concern that the world’ biggest consumer of the metal may be oversupplied.

- Two new books about Senator Hillary Rodham Clinton depict a tortured relationship with her husband and challenge the image she has presented on the presidential campaign trail. The books were both written by longtime

AP:

- The US Institute of Medicine called yesterday for tobacco to be regulated by the FDA, with nicotine levels to be reduced.

- Drivers in

- Existing Home Sales for April fell to 5.99M versus estimates of 6.12M and an upwardly revised 6.15M in March.