Click here for a weekly preview by MarketWatch.com.

Click here for Stocks in Focus for Monday by MarketWatch.com.

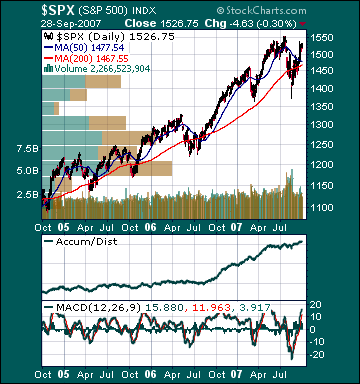

There are several economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. – ISM Manufacturing, ISM Prices Paid

Tues. – Pending Home Sales, Total Vehicle Sales, weekly retail sales

Wed. – Weekly MBA Mortgage Applications report, weekly EIA energy inventory report, Challenger Job Cuts, ADP Employment Change, ISM Non-Manufacturing

Thur. – Initial Jobless Claims, Factory Orders

Fri. – Change in Non-farm Payrolls, Unemployment Rate, Average Hourly Earnings, Consumer Credit

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. – Walgreen(WAG), Palm Inc.(PALM)

Tues. – Pepsi Bottling(PBG), Micron Tech(MU)

Wed. – Wolverine Worldwide(WWW), Immucor Inc.(BLUD), Arrow Intl.(ARRO), Gerber Scientific(GRB), IDT Corp.(IDT)

Thur. – Constellation Brands(STZ), Marriott Intl.(MAR), Acuity Brands(AYI), Family Dollar(FDO), Research In Motion(RIMM), Solectron(SLR)

Fri. – None of note

Other events that have market-moving potential this week include:

Mon. – Jeffries Technology Conference

Tue. – Citigroup Ethanol Conference, CIBC Industrials Conference, (IRM) analyst meeting, (KSS) investor day, (CIEN) analyst day, Deutsche Bank Leveraged Finance Conference, Jeffries Technology Conference

Wed. – Deutsche Bank Leveraged Finance Conference, William Blair Small-cap Growth Conference, CIBC Industrials Conference, BOE Policy Meeting, (CBRL) analyst meeting, (NSM) analyst meeting, (RENT) analyst presentation

Thur. – Fed’s Mishkin speaking, Fed’s Fisher speaking, ThinkEquity Healthcare Forum, (FLO) analyst meeting, Deutsche Bank Leveraged Finance Conference, BOE Policy Meeting, ECB Policy Meeting, (PRX) analyst meeting, (AEP) analyst meeting, (NSTK) analyst meeting

Fri. – None of note