Click here for the Wall St. Week Ahead by Reuters.

Click here for Stocks in Focus for Monday by MarketWatch.com.

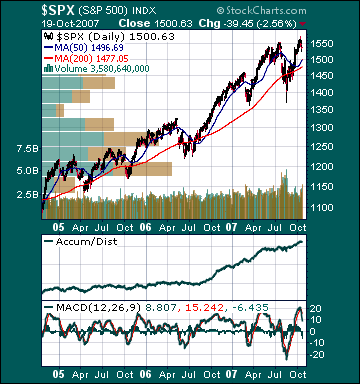

There are a few economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. – None of note

Tues. – Weekly retail sales reports, Richmond Fed Manufacturing Index

Wed. – Weekly MBA Mortgage Applications report, weekly EIA energy inventory data, Existing Home Sales

Thur. – Durable Goods Orders, Initial Jobless Claims, New Home Sales

Fri. –

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. – Halliburton(HAL), Hasbro(HAS), Merck(MRK), Schering-Plough(SGP), American Express(AXP), Apple Inc.(AAPL), Kimberly-Clark(KMB), Royal Carribean(RCL),

Tues. – Biogen Idec(BIIB), Brinker Intl.(EAT),

Wed. – Autonation(AN),

Thur. – Apache Corp.(APA), Black & Decker(BDK), Comcast Corp.(CMCSA), Goodrich Corp.(GR), Intercontinental Exchange(ICE), L-3 Communications(LLL), Starwood Hotels(HOT), XM Satellite Radio(XMSR), Zimmer Holdings(ZMH), Aetna Inc.(AET), Motorola Inc.(MOT), Raytheon(RTN), Southern Co.(SO), Kla-Tencor(KLAC), Baidu.com(BIDU), Ingram Micro(IM), Kenneth Cole(KCP), McAfee Inc.(MFE), Microsoft Corp.(MSFT), CB Richard Ellis(CBG), Celegene(CELG), Cummins Inc.(CMI), Deckers Outdoor(DECK), Diamond Offshore(DO), Dow Chemical(DOW), EMC Corp.(EMC), Estee Lauder(EL), General Motors(GM), Harrah’s Entertainment(HET), ImClone Sytems(IMCL), MBIA Inc.(MBI), Sybase Inc.(SY), Wendy’s International(WEN)

Fri. – Baker Hughes(BHI), Countrywide Financial(CFC), Tidewater Inc.(TDW), BearingPoint(BE), Fortune Brands(FO), Ingersoll-Rand(IR), ITT Corp.(ITT), Southern Copper(PCU)

Other events that have market-moving potential this week include:

Mon. – Fed’s Kroszner speaking, (WSO) analyst meeting, (NCI) Investor Day

Tue. – (BSX) analyst meeting, (WMT) analyst meeting

Wed. – (ARTC) analyst meeting, (EW) analyst lunch, (GOOG) analyst day

Thur. – None of note

Fri. – None of note