Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

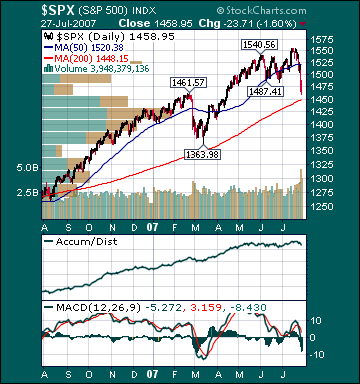

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes

Monday, July 30, 2007

Links of Interest

Sunday, July 29, 2007

Moday Watch

Weekend Headlines

Bloomberg:

- Investors are preparing to snap up shares of telephone, health-care and computer companies after last week’s $2.1 trillion global stock market rout left US equities the cheapest in 16 years.

- Schroder, ABN, Wells Load Up on Stocks in Worst Rout Since 2002.

- Barclays Plc shares may rise this week after reports that ABN Amro Holding NV’s board will withdraw its support for a bid from the

- Doosan Infracore Co., South Korea's largest construction-equipment maker, said it signed an agreement to buy a unit of Ingersoll-Rand Co. for $4.9 billion to expand its overseas business.

- New York state voters say Democratic Governor Eliot Spitzer should testify under oath about how much he knew of his staff’s actions to use state police in an effort to spy on a political opponent, according to a WNBC/Marist poll.

-

- US Treasury Secretary Henry Paulson, rejecting claims from Congress that he’s too soft on China, said negotiations rather than sanctions have led to a faster appreciation of the yuan.

- Automakers are embracing legislation in the US House that would raise fuel-economy standards, abandoning years of resistance because of concerns they might otherwise be forced to accept even tougher measures.

- Japan’s industrial production increased in June, ending the worst manufacturing slump in almost two years and easing concern that growth in the world’s second-largest economy may falter. Higher overseas demand is driving profits at Toshiba Corp. and Toyota Motor and encouraging them to make more chips and cars.

Wall Street Journal:

- Investors wondering what to do after the past week’s stock-market turbulence shouldn’t be throwing in the towel. Fast-growing big companies could be poised to move higher in coming months.

- A rice research institute in the

- The turmoil in the credit markets is beginning to wound some high-profile hedge-fund managers – but it’s prompting others to swoop in an snap up some beaten-down assets.

- Some Hard-Hit Cities See Signs of a Housing Market Turnaround.

NY Times:

- A senior member of the Bancroft family, which controls Dow Jones(DJ), has changed his mind and now supports selling the company to News Corp.(NWS/A).

- Hedge-fund firm Sowood Capital, founded by a former Harvard Management manager, is down about 10% this year after bond losses stemming from subprime mortgage turmoil.

- When it comes to making asset allocation decisions in your portfolio, it is best not to be dogmatic. That is the conclusion of a new study, which found that investors are likely to do better over the long term by resisting the advice of those who take extreme positions about how much of their portfolios should be allocated among the various assets classes.

- After years of being accused by Western nations of making only token gestures to fight fake goods and months of complaints about the safety of its exports, China is taking extraordinary steps to change its image.

- Microsoft is beset with competition from all sides, unlike any it has seen in decades, and Bill Gates, who co-founded the company 32 years ago, still intends to step away next year as planned.

- Facebook, the online social network, has stolen some of MySpace’s momentum with users and the news media. Now, it is being subjected to the same accusations that it does not do enough to keep sexual predators off its site.

TheStreet.com:

- Seven Reasons to Be Bullish Now.

MarketWatch.com:

- Despite Thursday, top market timing newsletters remain bullish.

- Duo of Google and Sprint could put AT&T in a headlock.

AP:

- Google Inc. may install by September a system to prevent copyright-infringing videos from being posted on its YouTube Web site, citing company lawyer Phillip Beck.

- EBay Inc.(EBAY) may use its “buy it now” feature even though the US Supreme Court ruled its infringed upon MercExchange’s patent, citing US District Judge Jerome Friedman.

LA Times:

- Walt Disney(DIS) dropped its plan to sell wine named after the Disney-Pixar movie “Ratatouille” at Costco Wholesale Corp.(COST) stores because of complaints from California winemakers and concerns over underage drinking, citing company spokesman Gary Foster.

CNNMoney.com:

- Is sourcing in China worth it? Businesses weigh the costs and benefits, in the wake of product recalls and bans.

- ‘Aesthetic medicine’ firms hope vanity has its price.

- Boston’s Brigham and Women’s Hospital plans to let a group of surgeons provide partial face transplants to patients with disfigured features.

NY Post:

- Tom Cruise’s United Artists movie studio and Merrill Lynch(MER) may complete a $500 million film-financing agreement by mid-August.

- More than half of all babies born in

- Microsoft Corp.(MSFT) co-founder Paul Allen is funding more documentary films, including one on climate change, adding to 20 movies financed by his production company.

Reuters:

- The technology company Google Inc.(GOOG) is the biggest gainer in Interbrand’s annual ranking of the top 100 Global Brands.(video)

- US average retail gasoline prices fell 17 cents per gallon over the past two weeks as Midwest refiners recovered from recent “difficulties” and produced more gas, an industry analyst said.

Financial Times:

- China’s steelmakers received more than $52 billion of government subsidies over the past decade, enabling them to sell products cheaper than international rivals, citing a report commissioned by the American Iron and Steel Institute.

- Carlos Ghosn, Nissan Motor’s CEO, said he will continue to seek an alliance with one of the three

Daily Telegraph:

- China and the other emerging giants have started to use their colossal reserves to buy Western companies.

Spiegel:

- Deutsche Bank AG,

IMF Survey Magazine:

- Global Growth Seen at 5.2% in 2007.

Weekend Recommendations

Barron's:

- Made positive comments on (CME), (DD), (INAP), (HD), (GRMN) and (IBKR).

- Made negative comments on (REDF) and (AMZN).

Citigroup:

- Reiterated Buy on (MSFT), target $36.

- Upgraded (VECO) to Buy, target $25.

Night Trading

Asian indices are -1.0% to -.25% on average.

S&P 500 futures +.08%.

NASDAQ 100 futures unch.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Pre-market Stock Quote/Chart

Before the Bell CNBC Video(bottom right)

Global Commentary

WSJ Intl Markets Performance

Commodity Movers

Top 25 Stories

Top 20 Business Stories

Today in IBD

In Play

Bond Ticker

Economic Preview/Calendar

Daily Stock Events

Macro Calls

Upgrades/Downgrades

Rasmussen Business/Economy Polling

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (ACV)/.24

- (APC)/.77

- (ANDW)/.17

- (ADM)/.58

- (CBG)/.42

- (CNA)/1.09

- (FPL)/.80

- (HUM)/1.28

- (JAH)/.57

- (LTR)/.98

- (MNST)/.34

- (OSIP)/.27

- (PBI)/.70

- (PPS)/.04

- (RSH)/.25

- (SUNW)/.05

- (TSN)/.24

- (VZ)/.59

- (VMC)/1.46

Upcoming Splits

- (SJR) 2-for-1

Economic Releases

- None of note

Today’s Other Potential Market Movers

- None of note

Weekly Outlook

Click here for Economic Preview by MarketWatch.com.

Click here for Stocks in Focus for Monday by MarketWatch.com.

There are several economic reports of note and a number of significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. – None of note

Tues. – Personal Income, Personal Spending, PCE Deflator, 2Q Employment Cost Index, S&P/CS Composite Home Price Index, Chicago Purchasing Manager, Consumer Confidence, Construction Spending, weekly retail sales

Wed. – Weekly MBA Mortgage Applications report, weekly EIA energy inventory report, Challenger Job Cuts, ADP Employment Change, Pending Home Sales, ISM Manufacturing, ISM Prices Paid, Total Vehicle Sales

Thur. – Initial Jobless Claims, Factory Orders

Fri. – Change in Non-farm Payrolls, Unemployment Rate, Average Hourly Earnings, ISM Non-Manufacturing

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. – Anadarko Petroleum(APC), Andrew Corp.(ANDW), Archer-Daniels-Midland(ADM), CB Richard Ellis(CBG), CNA Financial(CNA), Humana(HUM), Loews Corp.(LTR), Monster Worldwide(MNST), Pitney Bowes(PBI), Post Properties(PPS), RadioShack(RSH), Tyson Foods(TSN), Verizon Communications(VZ), Vulcan Materials(VMC)

Tues. – Automatic Data Processing(ADP), Avon Products(AVP), Buffalo Wild Wings(BWLD), Cephalon(CEPH), Chipotle Mexican Grill(CMG), Coach Inc.(COH), Diebold(DBD), DreamWorks(DWA), General Motors(GM), Hilton Hotels(HLT), IAC/InterActiveCorp.(IACI), ImClone Systems(IMCL), Liz Claiborne(LIZ), Marathon Oil(MRO), Masco Corp.(MAS), MetLife Inc.(MET), Nymex Holdings(NMX), Ruth’s Chris(RUTH), Safeco(SAF), Shaw Group(SGR), St. Joe(JOE), Under Armour(UA), Valero Energy(VLO), WebMD Health(WBMD), Whole Foods(WFMI)

Wed. – Administaff(ASF), Alltel Corp.(AT), Applebees(APPB), Boyd Gaming(BYD), CA Inc.(CA), Cigna(CI), Computer Sciences(CSC), Devon Energy(DVN), Dolby Labs(DLB), Dominion Resources(D), Electronic Arts(ERTS), Garmin(GRMN), Given Imaging(GIVN), GlobalSanataFe(GSF), Kraft(KFT), Martha Stewart(MSO), Mastercard(MA), OfficeMax(OMX), Prudential Financial(PRU), Starbucks(SBUX), Time Warner(TWX), Transocean(RIG), Walt Disney(DIS), Wynn Resorts(WYNN)

Thur. – Barnes Group(B), Clorox(CLX), Eastman Kodak(EK), Expedia(EXPE), Intl. Rectifier(IRF), International Paper(IP), Lear(LEA), MGM Mirage(MGM), Newmont Mining(NEM), NYSE Euronext(NYX), Rowan Cos(RDC), Starwood Hotels(HOT), Timberland(TBL)

Fri. – Armor Holdings(AH), Procter & Gamble(PG), Weyerhaeuser(WY)

Other events that have market-moving potential this week include:

Mon. – None of note

Tue. – Keefe, Bruyette & Woods Community Bank Investor Conference, (LSI) Analyst Day

Wed. – Keefe, Bruyette & Woods Community Bank Investor Conference, BOE Policy Meeting

Thur. – CIBC Communication Tech Conference, ThinkEquity Partners ThinkBIG Conference, BOE Policy Meeting, ECB Policy Meeting

Fri. – None of note

Friday, July 27, 2007

Weekly Scoreboard*

Indices

S&P 500 1,458.95 -4.90%

DJIA 13,265.47 -4.22%

NASDAQ 2,562.24 -4.66%

Russell 2000 777.83 -7.0%

Wilshire 5000 14,663.63 -5.14%

Russell 1000 Growth 591.22 -3.79%

Russell 1000 Value 825.97 -4.78%

Morgan Stanley Consumer 707.25 -3.19%

Morgan Stanley Cyclical 1,033.69 -6.87%

Morgan Stanley Technology 637.95 -2.33%

Transports 5,039.17 -5.98%

Utilities 474.79 -7.24%

MSCI Emerging Markets 133.14 -5.80%

NYSE Cumulative A/D Line 68,092 -10.50%

Bloomberg New Highs-Lows Index -1056 -340.0%

Bloomberg Crude Oil % Bulls 35.0 -3.9%

CFTC Oil Large Speculative Longs 252,944 +2.5%

Total Put/Call 1.3 +5.7%

NYSE Arms 1.37 -35.98%

Volatility(VIX) 24.17 +42.60%

ISE Sentiment 132.0 unch.

AAII % Bulls 44.2 +5.8%

AAII % Bears 36.8 +.4%

Futures Spot Prices

Crude Oil 76.96 +1.84%

Reformulated Gasoline 211.25 -2.29%

Natural Gas 6.23 -4.83%

Heating Oil 207.32 -.95%

Gold 673.0 -3.64%

Base Metals 253.66 -5.1%

Copper 354.60 -4.46%

Economy

10-year US Treasury Yield 4.76% -19 basis points

4-Wk MA of Jobless Claims 308,500 -1.3%

Average 30-year Mortgage Rate 6.69% - 4 basis points

Weekly Mortgage Applications 609.0 -3.6%

Weekly Retail Sales +2.80%

Nationwide Gas $3.92/gallon -.08/gallon

US Cooling Demand Next 7 Days 12.0% above normal

ECRI Weekly Leading Economic Index 143.70 -.14%

US Dollar Index 81.0 +.82%

CRB Index 319.61 -1.49%

Best Performing Style

Large-Cap Growth -3.79%

Worst Performing Style

Small-Cap Value -6.64%

Telecom -.67%

Computer Services -1.57%

HMOs -1.67%

Defense -1.96%

Internet -2.30%

Lagging Sectors

Papers -8.65%

Gold -9.0%

Engineering & Construction -9.2%

Homebuilders -9.7%

Coal -10.4%

One-Week High-Volume Gainers

One-Week High-Volume Losers

Stocks Lower into Final Hour as Lingering Credit Worries Offset Positive Economic Data

BOTTOM LINE: The Portfolio is higher into the final hour on gains in my Internet longs, Medical longs and Retail longs. I added slightly to my (GILD), (UA) and (PWR) longs, covered my (IWM)/(QQQQ) hedges and took some profits in my (EEM) short today, thus leaving the Portfolio 100% net long. The overall tone of the market is negative today as the advance/decline line is lower, most sectors are declining and volume is very heavy. My intraday gauge of investor angst is at an elevated level. Money market funds saw inflows of $12.57 billion, reaching another record high of $2.54 trillion. Recent market action makes me more convinced than ever that the secular trend of disinflation is still firmly intact. It is interesting to note the Baltic Dry Index hit another new high yesterday. As well, U.S. U.S. U.S.

Subscribe to:

Posts (Atom)