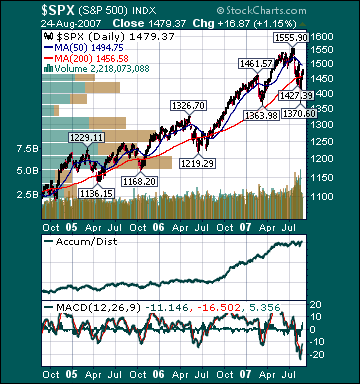

S&P 500 1,479.37 +2.31%*

Click here for What a Week from TheStreet.com.

*5-day % Change

Indices

S&P 500 1,479.37 +2.31%

DJIA 13,378.87 +2.29%

NASDAQ 2,576.69 +2.86%

Russell 2000 798.93 +1.64%

Wilshire 5000 14,855.94 +2.46%

Russell 1000 Growth 591.48 +3.02%

Russell 1000 Value 833.09 +2.05%

Morgan Stanley Consumer 719.15 +1.65%

Morgan Stanley Cyclical 1,031.87 +4.26%

Morgan Stanley Technology 629.74 +3.1%

Transports 4,915.95 +3.1%

Utilities 498.80 +2.34%

MSCI Emerging Markets 129.59 +7.29%

Sentiment/Internals

NYSE Cumulative A/D Line 65,381 +10.1%

Bloomberg New Highs-Lows Index -145 +92.2%

Bloomberg Crude Oil % Bulls n/a

CFTC Oil Large Speculative Longs 206,977 -6.2%

Total Put/Call 1.07 -12.3%

NYSE Arms .62 -7.14%

Volatility(VIX) 20.72 -30.91%

ISE Sentiment 115.0 -11.6%

AAII % Bulls 41.28 -2.2%

AAII % Bears 43.1 -5.4%

Futures Spot Prices

Crude Oil 71.2 -.61%

Reformulated Gasoline 197.85 -2.22%

Natural Gas 5.49 -21.1%

Heating Oil 199.70 -.74%

Gold 678.30 +1.53%

Base Metals 233.95 +4.45%

Copper 336.50 +7.82%

Economy

10-year US Treasury Yield 4.62% -7 basis points

4-Wk MA of Jobless Claims 317,800 +1.5%

Average 30-year Mortgage Rate 6.52% -10 basis points

Weekly Mortgage Applications 641.10 -5.5%

Weekly Retail Sales +2.2%

Nationwide Gas $2.78/gallon -.02/gallon

US Cooling Demand Next 7 Days 25.0% above normal

ECRI Weekly Leading Economic Index 139.80 -1.34%

US Dollar Index 80.69 -.93%

CRB Index 305.64 -.17%

Best Performing Style

Mid-cap Growth +3.8%

Worst Performing Style

Small-cap Value +1.4%

Leading Sectors

Steel +12.3%

Engineering & Construction +11.2%

Airlines +7.8%

Gaming +7.1%

Retail +5.1%

Lagging Sectors

Medical Equipment +1.95%

Alternative Energy +1.8%

Insurance +1.73%

Tobacco +1.30%

Banks -.98%

BOTTOM LINE: The Portfolio is higher into the final hour on gains in my Computer longs, Medical longs, Internet longs and Retail longs. I covered my some of my (EEM) short and all of my (IWM)/(QQQQ) hedges today, thus leaving the Portfolio 100% net long. The overall tone of the market is positive today as the advance/decline line is higher, every sector is rising and volume is below average. My intraday gauge of investor angst is still above average. Bloomberg is reporting that Google's (GOOG) chief economist is saying that the advertisers have not slowed Web spending. This is a positive for the stock and market. I expect Google to outperform the market substantially through year-end. There has been a lot of recession talk of late, mainly by those who know that the more the media talk about it, the more the consumer will retrench. A recession this year, defined by two consecutive quarters of negative growth, is virtually impossible, in my opinion. We would have to see a contraction this quarter. Based on my analysis, that is a very remote possibility. I also believe the likelihood of a recession beginning next year is fairly low. Recessions don't occur often. We never even saw two consecutive quarters of negative growth during the 2000-2002 bubble bursting and 9/11 terrorist attacks. I see few signs that point to a recession now, however, if we did start to get substantially weaker economic data, there is no doubt in my mind that the Fed would act and act vigorously. The Fed has a lot of ammunition to fire, and I strongly disagree with those who think that doesn't matter. We have heard for several years every time we get some weak data that the bulls are in a lose-lose situation. If the Fed cuts, it means the economy is too weak; if they don't, investors will sell because they will be disappointed. In my opinion, we are in a win-win situation. I think stocks rally if an imminent recession begins to be taken out of the equation, and I think we rally if the Fed cuts rates. We saw historic levels of investor angst in many gauges over the last few weeks as investors prepared for the worst. What if the worst doesn't happen? There is a mountain of cash on the sidelines, insiders are buying at levels last seen before we took off in 2003, fear is high, bears are partying likes it's 2000-2002, and the S&P 500 is just 4.8% off its record high. If the major averages continue to trade around current levels or even grind higher over the coming weeks as we get more negative news, investment manager performance anxiety will come back into play in a monstrous way. This could pave the way for an extraordinarily bullish fourth-quarter for stocks. Money market funds are at new record levels and have now seen $127.79 billion in cash inflows over the last two weeks, the most in several years. Asia will likely take today's

Bloomberg:

- German Chancellor Angela Merkel said the recent turmoil in world financial markets underscores the need for greater transparency in hedge funds, a key aim of

- Credit investors are overcompensating for their years of complacency by “shunning deals with innovation and added risk,” S&P analysts said in a report today.

- David Kelly, an economic adviser at Putnam Investments LLC, says worries about a slower housing market and losses on subprime mortgages have been blown out of proportion by Wall Street.

- Crude oil rose after a report showed orders for US-made durable goods rose more than expected last month, easing concern that loan defaults will slow economic growth.

- Sugar is falling 1% on speculation that a global surplus will overwhelm demand next year and that lower energy prices will reduce the value of ethanol made from sugar cane.

- Zbigniew Brzezinski, one of the most influential foreign-policy experts in the Democratic Party, threw his support behind Barack Obama’s presidential candidacy, saying the

-

- Republican presidential candidate Mitt Romney will propose tax breaks to help Americans pay for health insurance and incentives for states to craft their own programs to make sure everyone gets coverage.

NY Times:

- The headquarters of Google Inc.(GOOG) is increasingly popular among US presidential candidates as a fund-raising destination.

- What Credit Crunch?

Financial Times:

- Vulture funds, or seekers of distressed securities, are poised to pick through dead or wounded companies and securities. A net flow of $20 billion into distressed-securities funds in the first half of 2007 was double the entire amount for 2003-2006, citing Hedge Fund Research data.

- Durable Goods Orders for July rose 5.9% versus estimates of 1.0% and an upwardly revised 1.9% gain in June.

- Durable Ex Transports for July rose 3.7% versus estimates of a .6% gain and a downwardly revised 1.2% decline in June.

- New Home Sales for July rose to 870K versus estimates of 820K and an upwardly revised 846K in June.

BOTTOM LINE: Orders for US-made durable goods rose more than forecast in July, suggesting business spending remains healthy, Bloomberg reported. Orders for autos rose 9.8%, the biggest increase since January 2003 versus a .7% decline in the prior month. Non-defense capital goods orders excluding aircraft, a gauge of future business spending, rose 2.2%, versus a .1% decline in June. The gain in ex-transport orders was propelled by demand for machinery, communications gear and primary metals. I expect business spending to remain healthy over the intermediate-term as companies gain confidence in the sustainability of the current expansion and continue to rebuild depleted inventories.

Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes