Indices

S&P 500 1,270.20 +2.06%

DJIA 11,150.22 +1.47%

NASDAQ 2,172.09 +2.39%

Russell 2000 724.67 +5.0%

Wilshire 5000 12,808.89 +2.36%

S&P Equity Long/Short Index 1,129.31 +.08%

S&P Barra Growth 586.68 +1.71%

S&P Barra Value 681.93 +2.41%

Morgan Stanley Consumer 611.41 +1.71%

Morgan Stanley Cyclical 829.04 +2.78%

Morgan Stanley Technology 493.80 +1.53%

Transports 4,928.89 +3.27%

Utilities 413.95 +1.91%

S&P 500 Cum A/D Line 6,874.0 +9.0%

Bloomberg Oil % Bulls 53.0 +32.5%

CFTC Oil Large Speculative Longs 171,371 +6.0%

Put/Call .92 -7.07%

NYSE Arms 1.54 +105.33%

Volatility(VIX) 13.08 -17.68%

ISE Sentiment 107.00 -20.15%

AAII % Bulls 38.60 +12.21%

AAII % Bears 39.77 -4.40%

US Dollar 85.16 -1.98%

CRB 346.39 +3.39%

ECRI Weekly Leading Index 136.0 -.51%

Futures Spot Prices

Crude Oil 73.85 +2.99%

Unleaded Gasoline 222.30 +2.56%

Natural Gas 6.08 -1.29%

Heating Oil 203.85 +.67%

Gold 616.20 +4.97%

Base Metals 217.65 +8.36%

Copper 335.55 +4.01%

10-year US Treasury Yield 5.13% -1.72%

Average 30-year Mortgage Rate 6.78% +1.04%

Leading Sectors

Energy +6.27%

Gaming +5.04%

REITs +4.13%

Biotech +3.01%

I-Banks +2.81%

Lagging Sectors

Retail +.49%

Alternative Energy +.48%

Defense +.15%

Computer Hardware -.25%

Semis -.83%

One-Week High-Volume Gainers

One-Week High-Volume Losers

*5-Day % Change

Friday, June 30, 2006

Stocks Higher into Final Hour as Long-term Rates Fall and Shorts Cover

BOTTOM LINE: The Portfolio is slightly lower into the final hour on losses in my Computer longs and Energy-related shorts. I have not traded today, thus leaving the Portfolio 100% net long. The tone of the market is positive as the advance/decline line is higher, most sectors are higher and volume is below average. It is interesting to note that over the last two days, the ISE Sentiment Index declined 52% to an all-time low of 65.0 this morning. This is a positive, especially considering the magnitude of yesterday's advance. Copper reversed morning gains and looks like it may have put in another top. I expect US stocks to trade modestly higher into the close from current levels on short-covering, bargain hunting and lower long-term rates.

Today's Headlines

Bloomberg:

- Cholesterol-lowering drugs used to prevent heart attacks and stroke may also help fight a pandemic sparked by bird flu, and should be tested, said a physician who has studied immunization for decades.

- Barr Pharmaceuticals(BRL) raised its offer for the Croatian generic-drug maker Pliva d.d. to $2.3 billion in cash, topping a rival bid for eastern Europe’s largest drugmaker.

- Cendant Corp.(CD) agreed to sell Travelport, the travel subsidiary that includes the Orbitz Web site, to the Blackstone Group for $4.3 billion in cash as part of a plan to break the company into four pieces.

- Kirk Kerkorian’s Tracinda asked GM’s CEO Wagoner to explore a three-way partnership with Nissan Motor and Renault SA.

- US Treasuries rallied for a second day on optimism the Fed is close to done raising the benchmark interest rate and has kept inflation contained.

Wall Street Journal:

- DaimlerChrysler’s(DCX) Chrysler Group will announce tomorrow its new V8-powered Dodge Challenger coupe, designed to evoke a 1970s so-called muscle car.

- Standard & Poor’s said it will stop publishing its four-year-old Hedge Fund Index, highlighting the fallout from the collapse of commodity broker Refco Inc., citing court filings.

- Vic Gundotra, who spent 15 years at Microsoft Corp.(MSFT) helping market the company’s software, will leave to join rival Google(GOOG) net year, citing Google spokesman Steve Langdon.

- Gap Inc.(GPS) plans to put higher-priced merchandise in the apparel chain’s Old Navy outlets to test if customers will spend more and help the company boost sluggish sales.

- Iridium Satellite LLC is providing the US National Oceanic and Atmospheric Administration with satellite data links for a new tsunami warning system.

Boston Globe:

- Members of the Massachusetts House unanimously passed a bill that would raise the minimum wage to $8 an hour by October 2008, and rejected a plan to link future increases to the cost of living.

AP:

- Warren Buffett’s pledge of most of his fortune to the Bill and Melinda Gates Foundation has drawn criticism from pro-life abortion opponents. Activists including Thomas Euteneuer, a Roman Catholic priest who is president of Human Life International, criticized Gates and Buffett for their support of Planned Parenthood and international birth-control programs.

NY Times:

- New York City’s on-time high-school graduation rate last year was 58.2%, the highest in two decades, citing Schools Chancellor Joel Klein.

Financial Times:

- UK hedge funds should support disclosure of large short-selling positions, in order to avoid being imposed with more severe regulations, the Assoc. of British Insurers said.

Les Echos:

- Dell Inc.(DELL) will suffer reduced profitability in the next three or four quarters as its seeks growth in emerging markets such as China, Brazil and India, CEO Rollins said.

Beijing Antaike Information Development:

- China produced 68.3 metric tons of gold in the first four months of this year, up 13% form last year, citing the China Gold Assoc.

- China may consumer less copper than forecast this year as soaring prices damp use of the metal by cable and electric wire producers, which favor cheaper aluminum.

- Cholesterol-lowering drugs used to prevent heart attacks and stroke may also help fight a pandemic sparked by bird flu, and should be tested, said a physician who has studied immunization for decades.

- Barr Pharmaceuticals(BRL) raised its offer for the Croatian generic-drug maker Pliva d.d. to $2.3 billion in cash, topping a rival bid for eastern Europe’s largest drugmaker.

- Cendant Corp.(CD) agreed to sell Travelport, the travel subsidiary that includes the Orbitz Web site, to the Blackstone Group for $4.3 billion in cash as part of a plan to break the company into four pieces.

- Kirk Kerkorian’s Tracinda asked GM’s CEO Wagoner to explore a three-way partnership with Nissan Motor and Renault SA.

- US Treasuries rallied for a second day on optimism the Fed is close to done raising the benchmark interest rate and has kept inflation contained.

Wall Street Journal:

- DaimlerChrysler’s(DCX) Chrysler Group will announce tomorrow its new V8-powered Dodge Challenger coupe, designed to evoke a 1970s so-called muscle car.

- Standard & Poor’s said it will stop publishing its four-year-old Hedge Fund Index, highlighting the fallout from the collapse of commodity broker Refco Inc., citing court filings.

- Vic Gundotra, who spent 15 years at Microsoft Corp.(MSFT) helping market the company’s software, will leave to join rival Google(GOOG) net year, citing Google spokesman Steve Langdon.

- Gap Inc.(GPS) plans to put higher-priced merchandise in the apparel chain’s Old Navy outlets to test if customers will spend more and help the company boost sluggish sales.

- Iridium Satellite LLC is providing the US National Oceanic and Atmospheric Administration with satellite data links for a new tsunami warning system.

Boston Globe:

- Members of the Massachusetts House unanimously passed a bill that would raise the minimum wage to $8 an hour by October 2008, and rejected a plan to link future increases to the cost of living.

AP:

- Warren Buffett’s pledge of most of his fortune to the Bill and Melinda Gates Foundation has drawn criticism from pro-life abortion opponents. Activists including Thomas Euteneuer, a Roman Catholic priest who is president of Human Life International, criticized Gates and Buffett for their support of Planned Parenthood and international birth-control programs.

NY Times:

- New York City’s on-time high-school graduation rate last year was 58.2%, the highest in two decades, citing Schools Chancellor Joel Klein.

Financial Times:

- UK hedge funds should support disclosure of large short-selling positions, in order to avoid being imposed with more severe regulations, the Assoc. of British Insurers said.

Les Echos:

- Dell Inc.(DELL) will suffer reduced profitability in the next three or four quarters as its seeks growth in emerging markets such as China, Brazil and India, CEO Rollins said.

Beijing Antaike Information Development:

- China produced 68.3 metric tons of gold in the first four months of this year, up 13% form last year, citing the China Gold Assoc.

- China may consumer less copper than forecast this year as soaring prices damp use of the metal by cable and electric wire producers, which favor cheaper aluminum.

Income Rises More Than Inflation, Spending Decelerates, Confidence Improves, Chicago Manufacturing Slows

- Personal Income for May rose .4% versus estimates of a .2% gain and an upwardly revised .7% increase in April.

- Personal Spending for May rose .4% versus estimates of a .4% increase and an upwardly revised .7% gain in April.

- The PCE core for May rose .2% versus estimates of a .2% increase and a .2% gain in April.

- Final Univ. of Mich. Consumer Sentiment for June rose to 84.9 versus estimates of 82.5 and a prior estimate of 82.4.

- The Chicago Purchasing Manager Index for June fell to 56.5 versus estimates of 59.0 and a reading of 61.5 in May.

- Personal Spending for May rose .4% versus estimates of a .4% increase and an upwardly revised .7% gain in April.

- The PCE core for May rose .2% versus estimates of a .2% increase and a .2% gain in April.

- Final Univ. of Mich. Consumer Sentiment for June rose to 84.9 versus estimates of 82.5 and a prior estimate of 82.4.

- The Chicago Purchasing Manager Index for June fell to 56.5 versus estimates of 59.0 and a reading of 61.5 in May.

BOTTOM LINE: US consumer spending in May rose the least in three months and a measure of inflation watched by the Fed remained steady, Bloomberg said. Disposable income, or the money left over after taxes, rose 4.7% over the last 12 months. The PCE core, the Fed’s favorite inflation gauge, rose 2.1% over the last 12 months. Spending on services, which comprise almost 60% of all spending, gained .3% versus a .1% rise the prior month. Consumer spending rose 5.1% last quarter, the most in over two years. I expect income growth to remain steady around current levels and spending to slow to more average rates over the intermediate-term. I continue to believe inflation fears have peaked for the year.

Americans were more confident in June for the first time in three months as a decline in gas prices left them more to spend on other goods, Bloomberg said. The expectations component of the index rose to 72.0 versus 68.2 the prior month. Americans’ perceptions of their financial health and whether it’s a good time to buy big-ticket items surged to 105.0 versus 96.1 the prior moth, the largest gain this year. The expected inflation component of the index fell. Consumers see inflation decelerating to 3.3% over the next 12 months versus expectations of a 4% rise the prior month. I expect consumer sentiment to rise from irrationally low levels next month.

Growth at businesses in the Chicago area slowed in June, and a measure of prices paid for raw materials gained, Bloomberg reported. The prices paid index rose to 89 versus a reading of 76.9 the prior month. The new orders component of the index fell to 57.2 versus 69.6 the prior month. The employment component of the index decreased to 50.4 this month from 52.8 in May. I continue to believe manufacturing is slowing to average levels.

Thursday, June 29, 2006

Friday Watch

Late-Night Headlines

Bloomberg:

- EMC Corp.(EMC) agreed to buy RSA Security(RSAS) for about $2.1 billion to expand its security software business.

- Atlanta’s $32 million purchase of Martin Luther King Jr.’s papers, made just days before they were to be auctioned by Sotheby’s Holdings, will be a catalyst for getting a new civil rights museum built in the city, Mayor Shirley Franklin said.

- The US House of Representatives passed a resolution condemning the news media for reports last week that exposed a government program that tracks terrorism financing. The resolution, which passed 227-183, condemns the disclosure of classified programs and says they “may endanger the lives of Americans.”

- Japan’s consumer prices rose .6% in May from a year earlier, adding to evidence that deflation in the world’s second-largest economy may be over and supporting the Bank of Japan’s case for raising interest rates from near zero.

- A long-range missile test by North Korea would call into question commitments by the US and other countries to give security guarantees and aid in return for North Korea ending its nuclear program, a US government official said.

Wall Street Journal:

- Goldman Sachs Group(GS) was the top-earning investment bank in Asia excluding Japan in the first half, with estimated revenue exceeding $205 million, citing Dealogic Plc.

AP:

- The family of a man who disappeared from a Royal Caribbean Cruises Ltd.(RCL) ship last year is suing the company in Florida state court for unspecified monetary damages.

Xinhua News Agency:

- China will step up development of technology for monitoring Internet sites accessed within the country, citing the country’s top information gatekeeper.

China Securities Journal:

- China’s economy is growing too quickly and the government will take measures to slow growth, citing Zhu Zhixin, a deputy director with the National Development and Reform Commission.

Late Buy/Sell Recommendations

Business Week:

- Southern Copper(PCU) is benefiting from the mergers of other mining companies and may become a takeover target, citing Carl Birkelbach, CEO of Birkelbach Investment Securities.

- Acusphere Inc.(ACUS), which is developing drugs using microparticle technology, is undervalued at a time when it is expected to produce more favorable results, citing analyst Deborah Knobelman of Piper Jaffray.

- Devon Energy(DVN) may rise 55% on acquisition interest from Exxon Mobil(XOM) and Chevron Corp.(CHV), citing Oppenheimer’s Fadel Gheit.

Night Trading

Asian Indices are +.75% to +2.0% on average.

S&P 500 indicated -.09%.

NASDAQ 100 indicated -.22%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- None of note

Upcoming Splits

- (CLF) 2-for-1

- (LOW) 2-for-1

Economic Releases

8:30 am EST

- Personal Income for May is estimated to rise .2% versus a .5% increase in April.

- Personal Spending for May is estimated to rise .4% versus a .6% gain in April.

- The PCE core for May is estimated to rise .2% versus a .2% gain in April.

9:45 am EST

- The Final Univ. of Mich. Consumer Confidence reading for June is estimated to rise to 82.5 versus a prior estimate of 82.4.

10:00 am EST

- The Chicago Purchasing Index for June is estimated to fall to 59.0 versus a reading of 61.5 in May.

Bloomberg:

- EMC Corp.(EMC) agreed to buy RSA Security(RSAS) for about $2.1 billion to expand its security software business.

- Atlanta’s $32 million purchase of Martin Luther King Jr.’s papers, made just days before they were to be auctioned by Sotheby’s Holdings, will be a catalyst for getting a new civil rights museum built in the city, Mayor Shirley Franklin said.

- The US House of Representatives passed a resolution condemning the news media for reports last week that exposed a government program that tracks terrorism financing. The resolution, which passed 227-183, condemns the disclosure of classified programs and says they “may endanger the lives of Americans.”

- Japan’s consumer prices rose .6% in May from a year earlier, adding to evidence that deflation in the world’s second-largest economy may be over and supporting the Bank of Japan’s case for raising interest rates from near zero.

- A long-range missile test by North Korea would call into question commitments by the US and other countries to give security guarantees and aid in return for North Korea ending its nuclear program, a US government official said.

Wall Street Journal:

- Goldman Sachs Group(GS) was the top-earning investment bank in Asia excluding Japan in the first half, with estimated revenue exceeding $205 million, citing Dealogic Plc.

AP:

- The family of a man who disappeared from a Royal Caribbean Cruises Ltd.(RCL) ship last year is suing the company in Florida state court for unspecified monetary damages.

Xinhua News Agency:

- China will step up development of technology for monitoring Internet sites accessed within the country, citing the country’s top information gatekeeper.

China Securities Journal:

- China’s economy is growing too quickly and the government will take measures to slow growth, citing Zhu Zhixin, a deputy director with the National Development and Reform Commission.

Late Buy/Sell Recommendations

Business Week:

- Southern Copper(PCU) is benefiting from the mergers of other mining companies and may become a takeover target, citing Carl Birkelbach, CEO of Birkelbach Investment Securities.

- Acusphere Inc.(ACUS), which is developing drugs using microparticle technology, is undervalued at a time when it is expected to produce more favorable results, citing analyst Deborah Knobelman of Piper Jaffray.

- Devon Energy(DVN) may rise 55% on acquisition interest from Exxon Mobil(XOM) and Chevron Corp.(CHV), citing Oppenheimer’s Fadel Gheit.

Night Trading

Asian Indices are +.75% to +2.0% on average.

S&P 500 indicated -.09%.

NASDAQ 100 indicated -.22%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- None of note

Upcoming Splits

- (CLF) 2-for-1

- (LOW) 2-for-1

Economic Releases

8:30 am EST

- Personal Income for May is estimated to rise .2% versus a .5% increase in April.

- Personal Spending for May is estimated to rise .4% versus a .6% gain in April.

- The PCE core for May is estimated to rise .2% versus a .2% gain in April.

9:45 am EST

- The Final Univ. of Mich. Consumer Confidence reading for June is estimated to rise to 82.5 versus a prior estimate of 82.4.

10:00 am EST

- The Chicago Purchasing Index for June is estimated to fall to 59.0 versus a reading of 61.5 in May.

BOTTOM LINE: Asian indices are sharply higher, boosted by commodity, automaking and technology stocks in the region. I expect US equities to open modestly lower and to rally into the afternoon, finishing modestly higher. The Portfolio is 100% net long heading into the day.

Stocks Finish Sharply Higher on Bargain-Hunting and Short-Covering

Indices

S&P 500 1,272.87 +2.16%

DJIA 11,190.80 +1.98%

NASDAQ 2,174.38 +2.96%

Russell 2000 714.32 +3.82%

Wilshire 5000 12,808.90 +2.32%

S&P Barra Growth 588.56 +2.11%

S&P Barra Value 682.62 +2.20%

Morgan Stanley Consumer 609.99 +1.68%

Morgan Stanley Cyclical 824.80 +2.83%

Morgan Stanley Technology 496.30 +3.14%

Transports 4,890.23 +3.37%

Utilities 412.85 +1.03%

Put/Call .66 -20.48%

NYSE Arms .44 -43.94%

Volatility(VIX) 13.03 -17.48%

ISE Sentiment 105.00 -27.59%

US Dollar 86.00 -.73%

CRB 342.30 +1.22%

Futures Spot Prices

Crude Oil 73.64 +.15%

Unleaded Gasoline 229.10 -.17%

Natural Gas 6.11 -.33%

Heating Oil 198.76 +2.59%

Gold 600.10 +1.90%

Base Metals 214.04 +4.37%

Copper 333.65 +.47%

10-year US Treasury Yield 5.19% -.94%

Leading Sectors

Gold & Silver +6.97%

Restaurants +4.52%

Networking +4.30%

Lagging Sectors

Foods +1.05%

Utilities +1.03%

Hospitals +.97%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

- None of note

Afternoon/Evening Headlines

Bloomberg:

- Microsoft(MSFT) delayed the release of its new Office word processing, e-mail and spreadsheet program to make improvements to its performance and design.

- Futures traders trimmed bets that the Fed will continue lifting its target rate for overnight loans to 62% from 83% yesterday after policy makers increased the rate a quarter of a point for the 17th straight time.

- Apple Computer(AAPL) announced they were launching an internal probe into the backdating of stock options.

- Palm Inc.(PALM) maker of the Treo e-mail phones, said fourth-quarter profit rose 53% as demand for devices with full keyboards and business features increases.

- US Treasuries climbed as the Fed raised the benchmark interest rate as investors speculated inflation would remain contained.

S&P 500 1,272.87 +2.16%

DJIA 11,190.80 +1.98%

NASDAQ 2,174.38 +2.96%

Russell 2000 714.32 +3.82%

Wilshire 5000 12,808.90 +2.32%

S&P Barra Growth 588.56 +2.11%

S&P Barra Value 682.62 +2.20%

Morgan Stanley Consumer 609.99 +1.68%

Morgan Stanley Cyclical 824.80 +2.83%

Morgan Stanley Technology 496.30 +3.14%

Transports 4,890.23 +3.37%

Utilities 412.85 +1.03%

Put/Call .66 -20.48%

NYSE Arms .44 -43.94%

Volatility(VIX) 13.03 -17.48%

ISE Sentiment 105.00 -27.59%

US Dollar 86.00 -.73%

CRB 342.30 +1.22%

Futures Spot Prices

Crude Oil 73.64 +.15%

Unleaded Gasoline 229.10 -.17%

Natural Gas 6.11 -.33%

Heating Oil 198.76 +2.59%

Gold 600.10 +1.90%

Base Metals 214.04 +4.37%

Copper 333.65 +.47%

10-year US Treasury Yield 5.19% -.94%

Leading Sectors

Gold & Silver +6.97%

Restaurants +4.52%

Networking +4.30%

Lagging Sectors

Foods +1.05%

Utilities +1.03%

Hospitals +.97%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

- None of note

Afternoon/Evening Headlines

Bloomberg:

- Microsoft(MSFT) delayed the release of its new Office word processing, e-mail and spreadsheet program to make improvements to its performance and design.

- Futures traders trimmed bets that the Fed will continue lifting its target rate for overnight loans to 62% from 83% yesterday after policy makers increased the rate a quarter of a point for the 17th straight time.

- Apple Computer(AAPL) announced they were launching an internal probe into the backdating of stock options.

- Palm Inc.(PALM) maker of the Treo e-mail phones, said fourth-quarter profit rose 53% as demand for devices with full keyboards and business features increases.

- US Treasuries climbed as the Fed raised the benchmark interest rate as investors speculated inflation would remain contained.

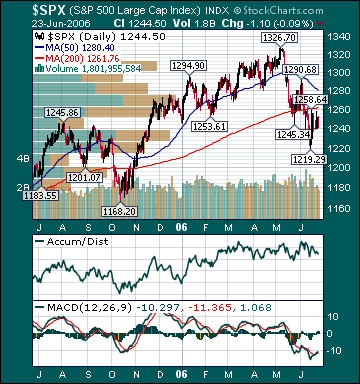

BOTTOM LINE: The Portfolio finished substantially higher today on gains in my Internet longs, Semi longs, Networking longs, Retail longs and Biotech longs. I covered some of my (EEM) shorts and all of my (IWM) and (QQQQ) shorts earlier in the day, thus leaving the Portfolio 100% net long. The tone of the market was very positive today as the advance/decline line finished substantially higher, every sector rose and volume was heavy. Measures of investor anxiety were mostly lower into the close. Overall, today's market performance was very bullish. The ISE Sentiment Index plunged 28% to 105.0, a depressed level, which is a big positive. Moreover, the 10-year yield finished near session lows. I sense many bears are trapped and bulls are underinvested, which should lead to more buying tomorrow as they scramble to stay ahead of benchmarks. The S&P 500 chart looks very similar to the pattern during the bottom last October. Subsequently, the index rose about 14% in less than seven months. Many of the exact same bear arguments were espoused during that October bottom. While I do expect another period of weakness over the coming months as the U.S. economy decelerates to average rates, I continue to believe most stocks have bottomed for the year and the major averages have put in place a meaningful bottom.

Today's Headlines

Bloomberg:

- Intel Corp.(INTC) CEO Paul Otellini, pressured by investors to fix the chipmaker’s flagging fortunes, is scrapping his old boss’s biggest projects.

- Venture Capital firms are betting big on solar and biofuel companies in a green energy frenzy.

- UK house prices rose for a fourth consecutive month in June, suggesting a revival in the $6 trillion property market may continue into the second half.

- Iran’s top nuclear negotiator Ali Larijani dismissed US and European calls to accelerate its decision over whether to accept trade and technology incentives in return for suspending its uranium enrichment program.

- US senators, hearing testimony yesterday that fraud is widespread in the $1.2 trillion hedge-fund industry, said the private investment partnerships may need more scrutiny form federal regulators and law enforcement.

- The US Supreme Court ruled that President Bush lacks authority to try Guantanamo Bay inmates before military tribunals, a blow to the administration’s anti-terrorism strategy that scales back presidential wartime powers.

Wall Street Journal:

- Symantec(SYMC) is in a $1 billion legal dispute with the IRS involving dealings with two related companies.

- Google(GOOG) will start operating in Cairo with a view to that city becoming the company’s hub for the Arabic-speaking Middle East.

- European politicians who criticize the US for allegedly violating the rights of “jihadist terrorists” at Guantanamo Bay in Cuba are more concerned with attacking America than in helping to fight terrorism, said Denis MacShane, British Labour Party Member of the Parliament.

- Pfizer Inc.(PFE) plans to produce a discounted generic version of Zoloft after the antidepressant loses its domestic patent protection tomorrow.

AP:

- Japan wants all its cars to run on ethanol-blended gasoline by 2030 to mitigate crude oil costs.

NY Times:

- RSA Security(RSAS) is close to an agreement to be bought by either data storage company EMC Corp.(EMC) or at least one other company in a transaction that may top $1.8 billion.

LA Times:

- Officials for the ports of LA and Long Beach have introduced an air pollution control plan that could reduce diesel pollution from cargo ships, trains, and trucks by more than half.

Financial Times:

- Many hedge funds have seen gains made earlier this year wiped out in June’s global market declines, citing performance figures obtained from funds and investors.

La Tribune:

- Dell Inc.(DELL) will grow faster than its industry in the long term and profitability will remain higher than that of competitors, CEO Rollins said.

- Intel Corp.(INTC) CEO Paul Otellini, pressured by investors to fix the chipmaker’s flagging fortunes, is scrapping his old boss’s biggest projects.

- Venture Capital firms are betting big on solar and biofuel companies in a green energy frenzy.

- UK house prices rose for a fourth consecutive month in June, suggesting a revival in the $6 trillion property market may continue into the second half.

- Iran’s top nuclear negotiator Ali Larijani dismissed US and European calls to accelerate its decision over whether to accept trade and technology incentives in return for suspending its uranium enrichment program.

- US senators, hearing testimony yesterday that fraud is widespread in the $1.2 trillion hedge-fund industry, said the private investment partnerships may need more scrutiny form federal regulators and law enforcement.

- The US Supreme Court ruled that President Bush lacks authority to try Guantanamo Bay inmates before military tribunals, a blow to the administration’s anti-terrorism strategy that scales back presidential wartime powers.

Wall Street Journal:

- Symantec(SYMC) is in a $1 billion legal dispute with the IRS involving dealings with two related companies.

- Google(GOOG) will start operating in Cairo with a view to that city becoming the company’s hub for the Arabic-speaking Middle East.

- European politicians who criticize the US for allegedly violating the rights of “jihadist terrorists” at Guantanamo Bay in Cuba are more concerned with attacking America than in helping to fight terrorism, said Denis MacShane, British Labour Party Member of the Parliament.

- Pfizer Inc.(PFE) plans to produce a discounted generic version of Zoloft after the antidepressant loses its domestic patent protection tomorrow.

AP:

- Japan wants all its cars to run on ethanol-blended gasoline by 2030 to mitigate crude oil costs.

NY Times:

- RSA Security(RSAS) is close to an agreement to be bought by either data storage company EMC Corp.(EMC) or at least one other company in a transaction that may top $1.8 billion.

LA Times:

- Officials for the ports of LA and Long Beach have introduced an air pollution control plan that could reduce diesel pollution from cargo ships, trains, and trucks by more than half.

Financial Times:

- Many hedge funds have seen gains made earlier this year wiped out in June’s global market declines, citing performance figures obtained from funds and investors.

La Tribune:

- Dell Inc.(DELL) will grow faster than its industry in the long term and profitability will remain higher than that of competitors, CEO Rollins said.

1Q GDP Booms, Job Market Still Healthy

- Final 1Q GDP rose 5.6% versus estimates of a 5.6% gain and a prior estimate of a 5.3% rise.

- Final 1Q GDP Price Index rose 3.1% versus estimates of a 3.3% increase and prior estimates of a 3.3% increase.

- Final 1Q Personal Consumption rose 5.1% versus estimates of 5.2% and prior estimates of a 5.2% increase.

- Initial Jobless Claims for last week rose 313K versus estimates of 310K and 309K the prior week.

- Continuing Claims rose to 2409K versus estimates of 2430K and 2355K prior.

- Final 1Q GDP Price Index rose 3.1% versus estimates of a 3.3% increase and prior estimates of a 3.3% increase.

- Final 1Q Personal Consumption rose 5.1% versus estimates of 5.2% and prior estimates of a 5.2% increase.

- Initial Jobless Claims for last week rose 313K versus estimates of 310K and 309K the prior week.

- Continuing Claims rose to 2409K versus estimates of 2430K and 2355K prior.

BOTTOM LINE: The US economy boomed at an annual rate of 5.6% in the first quarter, propelled by a surge in consumer spending, Bloomberg reported. Business investment rose at the fastest pace in six years. Inventory rebuilding, along with robust profits, should continue to spur corporate spending over the intermediate-term. The core PCE index, the Fed’s favorite inflation gauge, rose 2% for the quarter. I expect second quarter GDP to rise around average levels, consumption to moderate and the core PCE to decelerate.

First-time claims for unemployment benefits in the US rose last week while remaining at a level that suggests strength in the labor market, Bloomberg said. The four-week moving average of claims fell to 305,500 from 311,500 the prior week. The four-week average of total benefit rolls fell to 2.39 million, the lowest in almost 6 years. The unemployment rate among those eligible for benefits, which tracks the US unemployment rate, rose to 1.9% from 1.8% the prior week. I continue to believe the labor market will remain healthy without generating substantial unit labor cost increases over the intermediate-term.

Wednesday, June 28, 2006

Thursday Watch

Late-Night Headlines

Bloomberg:

- BlueScope Steel Ltd., Australia’s largest steelmaker, cut its full-year profit estimate for the third time this year. Its shares fell the most in three months.

- The American public has turned against the Fed’s two-year campaign of interest-rate increases, concerned it may hurt the economy by slowing growth, a Bloomberg/LA Times poll shows.

Financial Times:

- Dell Inc.(DELL) has reorganized its Americas division after several quarters of worse-than-expected results, citing an interview with CEO Rollins.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are +.75% to +1.25% on average.

S&P 500 indicated +.08%.

NASDAQ 100 indicated +.06%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (ACN)/.46

- (AM)/.26

- (CA)/.20

- (STZ)/.32

- (GIS)/.61

- (MON)/1.20

- (PALM)/.23

- (WOR)/.40

Upcoming Splits

- None of note

Economic Releases

8:30 am EST

- Final 1Q GDP is estimated to rise 5.6% versus a prior estimate of a 5.3% gain.

- Final 1Q GDP Price Index is estimated to rise 3.3% versus a prior estimate of a 3.3% gain.

- Final 1Q Personal Consumption is estimated to rise 5.2% versus a prior estimate of a 5.2% gain.

- Initial Jobless Claims for last week are estimated to rise to 310K versus 308K the prior week.

- Continuing Claims are estimated to fall to 2430K versus 2439K prior.

2:15 pm EST

- The FOMC is expected to raise the benchmark Fed Funds rate 25 basis points to 5.25%.

Bloomberg:

- BlueScope Steel Ltd., Australia’s largest steelmaker, cut its full-year profit estimate for the third time this year. Its shares fell the most in three months.

- The American public has turned against the Fed’s two-year campaign of interest-rate increases, concerned it may hurt the economy by slowing growth, a Bloomberg/LA Times poll shows.

Financial Times:

- Dell Inc.(DELL) has reorganized its Americas division after several quarters of worse-than-expected results, citing an interview with CEO Rollins.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are +.75% to +1.25% on average.

S&P 500 indicated +.08%.

NASDAQ 100 indicated +.06%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (ACN)/.46

- (AM)/.26

- (CA)/.20

- (STZ)/.32

- (GIS)/.61

- (MON)/1.20

- (PALM)/.23

- (WOR)/.40

Upcoming Splits

- None of note

Economic Releases

8:30 am EST

- Final 1Q GDP is estimated to rise 5.6% versus a prior estimate of a 5.3% gain.

- Final 1Q GDP Price Index is estimated to rise 3.3% versus a prior estimate of a 3.3% gain.

- Final 1Q Personal Consumption is estimated to rise 5.2% versus a prior estimate of a 5.2% gain.

- Initial Jobless Claims for last week are estimated to rise to 310K versus 308K the prior week.

- Continuing Claims are estimated to fall to 2430K versus 2439K prior.

2:15 pm EST

- The FOMC is expected to raise the benchmark Fed Funds rate 25 basis points to 5.25%.

BOTTOM LINE: Asian indices are higher, boosted by commodity and technology stocks in the region. I expect US equities to open modestly higher and to build on gains into the afternoon, finishing higher. The Portfolio is 75% net long heading into the day.

Stocks Finish at Session Highs ahead of Fed Announcement

Indices

S&P 500 1,246.00 +.55%

DJIA 10,973.56 +.45%

NASDAQ 2,111.84 +.55%

Russell 2000 688.04 +.16%

Wilshire 5000 12,518.20 +.47%

S&P Barra Growth 576.40 +.49%

S&P Barra Value 667.92 +.60%

Morgan Stanley Consumer 599.92 +.10%

Morgan Stanley Cyclical 802.08 +.41%

Morgan Stanley Technology 481.19 +.58%

Transports 4,730.60 +.56%

Utilities 408.63 +.51%

Put/Call .83 -15.31%

NYSE Arms .75 -50.36%

Volatility(VIX) 15.79 -3.72%

ISE Sentiment 140.00 -2.78%

US Dollar 86.67 +.23%

CRB 338.19 +.33%

Futures Spot Prices

Crude Oil 72.34 +.21%

Unleaded Gasoline 220.59 +.34%

Natural Gas 5.88 -3.60%

Heating Oil 194.60 +.44%

Gold 581.20 +.03%

Base Metals 205.08 +1.37%

Copper 315.05 -1.15%

10-year US Treasury Yield 5.24% +.83%

Leading Sectors

Energy +1.82%

Gaming +1.62%

Steel +1.44%

Lagging Sectors

Alternative Energy -.94%

Airlines -.99%

Restaurants -1.15%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

CSFB:

- Rated (FRX) and (BRL) Outperform.

Afternoon/Evening Headlines

Bloomberg:

- A tsunami alert system for nations bordering the Indian Ocean is up and running, 18 months after deadly waves triggered by an earthquake slammed into 12 nations across the region and killed an estimated 220,000 people.

- BP Plc(BP) manipulated the price of propane used to heat homes and businesses in the northeastern US in February 2004 and tried to do the same in April 2003, the Commodity Futures Trading Commission said.

- Walt Disney(DIS) named former Procter & Gamble CEO John E. Pepper as its non-executive chairman, succeeding former US Senator George Mitchell.

- Henry Paulson, confirmed today by the US Senate to become Treasury Secretary, said faster global economic growth will help reduce lopsided global trade and investment flows.

AP:

- Sunni insurgents offered to stop attacks on US-led military forces in Iraq if the Iraqi government and President Bush set a two-year deadline for withdrawing all foreign troops.

Financial Times Deutschland:

- Advanced Micro Devices(AMD) aims to win Dell Inc.(DELL) as a customer for its personal computer chips after agreeing to equip Dell servers, citing AMD strategist Margaret Lewis.

S&P 500 1,246.00 +.55%

DJIA 10,973.56 +.45%

NASDAQ 2,111.84 +.55%

Russell 2000 688.04 +.16%

Wilshire 5000 12,518.20 +.47%

S&P Barra Growth 576.40 +.49%

S&P Barra Value 667.92 +.60%

Morgan Stanley Consumer 599.92 +.10%

Morgan Stanley Cyclical 802.08 +.41%

Morgan Stanley Technology 481.19 +.58%

Transports 4,730.60 +.56%

Utilities 408.63 +.51%

Put/Call .83 -15.31%

NYSE Arms .75 -50.36%

Volatility(VIX) 15.79 -3.72%

ISE Sentiment 140.00 -2.78%

US Dollar 86.67 +.23%

CRB 338.19 +.33%

Futures Spot Prices

Crude Oil 72.34 +.21%

Unleaded Gasoline 220.59 +.34%

Natural Gas 5.88 -3.60%

Heating Oil 194.60 +.44%

Gold 581.20 +.03%

Base Metals 205.08 +1.37%

Copper 315.05 -1.15%

10-year US Treasury Yield 5.24% +.83%

Leading Sectors

Energy +1.82%

Gaming +1.62%

Steel +1.44%

Lagging Sectors

Alternative Energy -.94%

Airlines -.99%

Restaurants -1.15%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

CSFB:

- Rated (FRX) and (BRL) Outperform.

Afternoon/Evening Headlines

Bloomberg:

- A tsunami alert system for nations bordering the Indian Ocean is up and running, 18 months after deadly waves triggered by an earthquake slammed into 12 nations across the region and killed an estimated 220,000 people.

- BP Plc(BP) manipulated the price of propane used to heat homes and businesses in the northeastern US in February 2004 and tried to do the same in April 2003, the Commodity Futures Trading Commission said.

- Walt Disney(DIS) named former Procter & Gamble CEO John E. Pepper as its non-executive chairman, succeeding former US Senator George Mitchell.

- Henry Paulson, confirmed today by the US Senate to become Treasury Secretary, said faster global economic growth will help reduce lopsided global trade and investment flows.

AP:

- Sunni insurgents offered to stop attacks on US-led military forces in Iraq if the Iraqi government and President Bush set a two-year deadline for withdrawing all foreign troops.

Financial Times Deutschland:

- Advanced Micro Devices(AMD) aims to win Dell Inc.(DELL) as a customer for its personal computer chips after agreeing to equip Dell servers, citing AMD strategist Margaret Lewis.

BOTTOM LINE: The Portfolio finished slightly higher today on gains in my Internet longs, Retail longs and Biotech longs. I covered some of my (EEM), (IWM) and (QQQQ) shorts earlier in the day, thus leaving the Portfolio 75% net long. The tone of the market was modestly positive today as the advance/decline line finished slightly higher, sector performance was mixed and volume was below average. Measures of investor anxiety were lower into the close. Overall, today's market performance was mildly bullish. A number of market leading stocks posted outsized gains. As well, bears were unable to capitalize on yesterday's weakness. The 4-basis-point rise in the 10-year yield likely capped an otherwise more vigorous rally. I suspect long-term rates may fall on tomorrow's Fed rate hike. Natural gas is trading at new cycle lows, falling another 4%. I continue to expect stocks to finish the last two days strongly.

Today's Headlines

Bloomberg:

- Senate Majority Leader Bill Frist said he expects an “overwhelming majority” of senators to vote tomorrow for Henry Paulson to be the next US Treasury secretary.

- DaimlerChrysler AG plans to sell the two-seat Smart mini-car in the US, betting a fuel-efficient vehicle that fits on a pool table will help end eight years of losses at is Smart division.

- Russian President Putin told his security services to find and kill those responsible for the deaths of four Russian diplomats in Iraq.

- Pessimism about US stocks rose to the highest level since October 2002 last week, according to Investors Intelligence, a very bullish development.

- The US government needs to step in and regulate the $1.2 trillion hedge-fund industry or states will “join forces” and oversee the private investment pools, the attorney general of Connecticut told senators.

- US Dept. of Energy Secretary Samuel Bodman announced today that the DOE has approved two loan requests totaling 750,000 barrels of crude oil from the Strategic Petroleum Reserve to two Louisiana refineries.

Wall Street Journal:

- US money managers are gaining enthusiasm for large-capitalization stocks and losing interest in small-cap shares.

- Mitsubishi UFJ Financial Group, the world’s biggest lender by assets, is in talks with the US Fed about obtaining “financial holding company” status, a move that would allow the Japanese bank to expand into underwriting, insurance and investment banking in the US.

- A small group of hedge fund managers is heading a campaign to deter Congress and the SEC from tightening regulations over the business.

- HJ Heinz(HNZ) is trying to rebuild relations with McDonald’s 33 years after being cut off for not supplying enough ketchup during a tomato shortage.

- Two Detroit-area auto dealers are offering modified versions of the Hummer H2 and H3 they say can get 25 miles per gallon in highway traffic compared with the usual 19 to 20.

- United Parcel Service(UPS) and the US Postal Service reached an agreement on a deal that will put mail on UPS planes and may improve the post office’s reliability.

- US securities firms face two civil antitrust lawsuits in connection with the part they allegedly play in “naked short-selling.”

USA Today:

- 33% US adults said they are changing their summer vacation plans because of higher gas prices.

AP:

- Dallas Mavericks owner Mark Cuban and Hall of Fame quarterback Dan Marino have joined a bid to buy the NHL’s Pittsburgh Penguins.

NY Times:

- President Bush’s administration will issue new welfare rules today that will prompt states to move more people from welfare to work, representing the biggest policy change since 1996.

- Iraqi Prime Minister Nuri al-Maliki said the country’s new amnesty plan won’t allow pardons for people who attacked US soldiers “out of respect” for their contributions.

- The US Episcopal Church may lose full membership of the Anglican Communion if it doesn’t renounce same-sex unions and gay bishops, citing the Church of England’s Archbishop of Canterbury.

- Three-time heavyweight boxing champ Muhammad Ali plans to introduce a line of reduced-calorie snacks and beverages aimed at curbing youth obesity.

Washington Post:

- Military commanders said they expect to reach their target of training and equipping more than 325,000 members of the new Iraqi security forces by the end of the year.

Daily Telegraph:

- Global mergers and acquisitions activity may reach a record $3,500 billion this year, citing Thomson Financial.

Wall Street Journal Asia:

- China’s cabinet plans a two-day meeting this year to set new policies for the nation’s financial system.

- Senate Majority Leader Bill Frist said he expects an “overwhelming majority” of senators to vote tomorrow for Henry Paulson to be the next US Treasury secretary.

- DaimlerChrysler AG plans to sell the two-seat Smart mini-car in the US, betting a fuel-efficient vehicle that fits on a pool table will help end eight years of losses at is Smart division.

- Russian President Putin told his security services to find and kill those responsible for the deaths of four Russian diplomats in Iraq.

- Pessimism about US stocks rose to the highest level since October 2002 last week, according to Investors Intelligence, a very bullish development.

- The US government needs to step in and regulate the $1.2 trillion hedge-fund industry or states will “join forces” and oversee the private investment pools, the attorney general of Connecticut told senators.

- US Dept. of Energy Secretary Samuel Bodman announced today that the DOE has approved two loan requests totaling 750,000 barrels of crude oil from the Strategic Petroleum Reserve to two Louisiana refineries.

Wall Street Journal:

- US money managers are gaining enthusiasm for large-capitalization stocks and losing interest in small-cap shares.

- Mitsubishi UFJ Financial Group, the world’s biggest lender by assets, is in talks with the US Fed about obtaining “financial holding company” status, a move that would allow the Japanese bank to expand into underwriting, insurance and investment banking in the US.

- A small group of hedge fund managers is heading a campaign to deter Congress and the SEC from tightening regulations over the business.

- HJ Heinz(HNZ) is trying to rebuild relations with McDonald’s 33 years after being cut off for not supplying enough ketchup during a tomato shortage.

- Two Detroit-area auto dealers are offering modified versions of the Hummer H2 and H3 they say can get 25 miles per gallon in highway traffic compared with the usual 19 to 20.

- United Parcel Service(UPS) and the US Postal Service reached an agreement on a deal that will put mail on UPS planes and may improve the post office’s reliability.

- US securities firms face two civil antitrust lawsuits in connection with the part they allegedly play in “naked short-selling.”

USA Today:

- 33% US adults said they are changing their summer vacation plans because of higher gas prices.

AP:

- Dallas Mavericks owner Mark Cuban and Hall of Fame quarterback Dan Marino have joined a bid to buy the NHL’s Pittsburgh Penguins.

NY Times:

- President Bush’s administration will issue new welfare rules today that will prompt states to move more people from welfare to work, representing the biggest policy change since 1996.

- Iraqi Prime Minister Nuri al-Maliki said the country’s new amnesty plan won’t allow pardons for people who attacked US soldiers “out of respect” for their contributions.

- The US Episcopal Church may lose full membership of the Anglican Communion if it doesn’t renounce same-sex unions and gay bishops, citing the Church of England’s Archbishop of Canterbury.

- Three-time heavyweight boxing champ Muhammad Ali plans to introduce a line of reduced-calorie snacks and beverages aimed at curbing youth obesity.

Washington Post:

- Military commanders said they expect to reach their target of training and equipping more than 325,000 members of the new Iraqi security forces by the end of the year.

Daily Telegraph:

- Global mergers and acquisitions activity may reach a record $3,500 billion this year, citing Thomson Financial.

Wall Street Journal Asia:

- China’s cabinet plans a two-day meeting this year to set new policies for the nation’s financial system.

Tuesday, June 27, 2006

Wednesday Watch

Late-Night Headlines

Bloomberg:

- Honda Motor Co. chose Indiana as the home of its sixth North American auto-assembly plant.

- J. Crew Group(JCG), the casual clothing retailer part-owned by Texas Pacific Group, raised $376 million through an IPO today, topping its expected price range and signaling strong demand for new issues.

- Bank of China Ltd. drew $84.6 billion of bids for the nation’s biggest public offering, 52 times the stock on offer, underlining demand for new equity after the lifting of a yearlong ban on share sales.

Financial Times:

- High oil prices and the risk of volatility in commodity markets now rank ahead of fraud and the growth of hedge funds as the main concern for the stability of banks and financial regulators, citing a survey by the Center for the Study of Financial Innovation. Trading in derivatives linked to commodities has been one of the largest areas for growth for investment banks.

Xinhua news:

- Chinese government policies meant to curb excessive expansion in investment and credit must be implemented to ensure the economy maintains “stable, fast growth,” citing the head of the nation’s top planning body.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are -1.50% to -.75% on average.

S&P 500 indicated -.04%.

NASDAQ 100 indicated -.16%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (COMS)/.04

- (ARRO)/.33

- (BMET)/.45

- (CAG)/.29

- (EMMS)/-.05

- (MLHR)/.37

- (MKC)/.30

- (MU)/.10

- (PAYX)/.32

- (RHAT)/.09

Upcoming Splits

- (ANDE) 2-for-1

Economic Releases

10:30 am EST

- Bloomberg consensus estimates call for a 1,400,000 barrel crude oil drawdown. Gasoline supplies are expected to rise by 450,000 barrels. Distillate supplies are estimated to rise by 1,450,000 barrels. Finally, refinery utilization is expected to rise 0.30%.

Bloomberg:

- Honda Motor Co. chose Indiana as the home of its sixth North American auto-assembly plant.

- J. Crew Group(JCG), the casual clothing retailer part-owned by Texas Pacific Group, raised $376 million through an IPO today, topping its expected price range and signaling strong demand for new issues.

- Bank of China Ltd. drew $84.6 billion of bids for the nation’s biggest public offering, 52 times the stock on offer, underlining demand for new equity after the lifting of a yearlong ban on share sales.

Financial Times:

- High oil prices and the risk of volatility in commodity markets now rank ahead of fraud and the growth of hedge funds as the main concern for the stability of banks and financial regulators, citing a survey by the Center for the Study of Financial Innovation. Trading in derivatives linked to commodities has been one of the largest areas for growth for investment banks.

Xinhua news:

- Chinese government policies meant to curb excessive expansion in investment and credit must be implemented to ensure the economy maintains “stable, fast growth,” citing the head of the nation’s top planning body.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are -1.50% to -.75% on average.

S&P 500 indicated -.04%.

NASDAQ 100 indicated -.16%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (COMS)/.04

- (ARRO)/.33

- (BMET)/.45

- (CAG)/.29

- (EMMS)/-.05

- (MLHR)/.37

- (MKC)/.30

- (MU)/.10

- (PAYX)/.32

- (RHAT)/.09

Upcoming Splits

- (ANDE) 2-for-1

Economic Releases

10:30 am EST

- Bloomberg consensus estimates call for a 1,400,000 barrel crude oil drawdown. Gasoline supplies are expected to rise by 450,000 barrels. Distillate supplies are estimated to rise by 1,450,000 barrels. Finally, refinery utilization is expected to rise 0.30%.

BOTTOM LINE: Asian indices are lower, weighed down by commodity and technology stocks in the region. I expect US equities to open lower and to rally into the afternoon, finishing mixed. The Portfolio is 50% net long heading into the day.

***Alert***

I am unable to post the Tuesday Close due to a scheduling conflict. I will post the Wednesday Watch later this evening.

Stocks Lower into Final Hour on Rate Hike Worries

BOTTOM LINE: The Portfolio is lower into the final hour on losses in my Retail longs, Networking longs and Semi longs. I added to my (EEM), (IWM) and (QQQQ) shorts, thus leaving the Portfolio 50% net long. The tone of the market is negative as the advance/decline line is substantially lower, almost every sector is lower and volume is below average. The Johnson Redbook same-store sales index rose 3.3% year over year last week vs. a 3.2% rise the prior week. The long-term average is again of around 2.6%. I continue to see little evidence that a significant decline in consumer spending is on the horizon. I do, however, still expect to see retail sales decelerate back to average levels by next month. I expect US stocks to trade mixed into the close from current levels as short-covering and bargain hunting offset Fed worries.

Today's Headlines

Bloomberg:

- Barr Pharmaceuticals(BRL) agreed to buy Pliva d.d., eastern Europe’s biggest drugmaker, for $2.2 billion in cash, topping a bid from Iceland’s Actavis Group hf.

- The Hamas and Fatah movements, which share control of the Palestinian Authority, today agreed to back a document that implicitly recognizes Israel’s right to exist.

- Intel Corp.(INTC) agreed to sell a unit that builds chips for devices such as the BlackBerry to Marvell Technology Group.(MRVL) for $600 million as the company slashes costs and seeks to regain market share in its bigger businesses.

- Copper is falling 4% on mounting concern that the world’s central banks will continue to boost interest rates to combat inflation, slowing the economy and demand for metals.

- Henry Paulson, President Bush’s nominee for US Treasury Secretary, said “low” tax rates and fixing the Social Security and Medicare programs are key to a stronger economy.

Wall Street Journal:

- General Electric’s(GE) NBC Universal today plans to announce it will offer YouTube Inc. promotional video clips for some of its shows including “The Office” and “Saturday Night Live.”

- The US House of Representatives this week will probably cancel a 25-year restriction on oil and gas exploration along portions of the US coast.

- Google(GOOG) will introduce a test version of its GBuy online-payment service as early as this week to challenge EBay’s(EBAY) PayPal online-payment service.

- Time Warner’s(TWX) Warner Bros. will distribute movies and television shows over the Internet under an agreement to use Guba’s search engine and video-sharing network.

- US investors have been playing it safe, opting for multi-cap or all-cap mutual funds rather than large-cap or small-cap funds.

- Sony’s(SNE) personal music player is still struggling to compete with Apple Computer’s(AAPL) iPod, citing Sony president Ryoji Chubachi.

- A Coca-Cola bottler and MasterCard Intl. plan to site 1,000 vending machines in the Philadelphia area which will be able to accept credit and debit cards.

Washington Post:

- President Bush asked US Homeland Security Secretary Michael Chertoff to overhaul the nation’s Emergency Alert System because of weaknesses revealed after the Sept. 11, 2001, terrorist attacks and Hurricane Katrina in 2005.

Miami Herald:

- “Full-house” generators have become an important feature for high-priced South Florida homes after six major hurricanes in two years.

NY Times:

- Univision Communications(UVN) may accept a bid worth about $36.25 a share, or $11 billion, from a group led by billionaire Haim Saban.

USA Today:

- Real estate in more than 30 major metro areas, including Washington, Atlantic City, New York, Las Vegas, Phoenix, Sacramento and San Diego, more than doubled since 2000. Home prices will rise another 5% this year, according to the paper.

Handelsblatt:

- Kohlberg Kravis Roberts raised $15.5 billion for the biggest ever private equity fund.

Xinhua News:

- China’s government may fine media organizations as much as $12,501 for unauthorized reporting of emergencies under a draft law legislators started debating yesterday.

- Barr Pharmaceuticals(BRL) agreed to buy Pliva d.d., eastern Europe’s biggest drugmaker, for $2.2 billion in cash, topping a bid from Iceland’s Actavis Group hf.

- The Hamas and Fatah movements, which share control of the Palestinian Authority, today agreed to back a document that implicitly recognizes Israel’s right to exist.

- Intel Corp.(INTC) agreed to sell a unit that builds chips for devices such as the BlackBerry to Marvell Technology Group.(MRVL) for $600 million as the company slashes costs and seeks to regain market share in its bigger businesses.

- Copper is falling 4% on mounting concern that the world’s central banks will continue to boost interest rates to combat inflation, slowing the economy and demand for metals.

- Henry Paulson, President Bush’s nominee for US Treasury Secretary, said “low” tax rates and fixing the Social Security and Medicare programs are key to a stronger economy.

Wall Street Journal:

- General Electric’s(GE) NBC Universal today plans to announce it will offer YouTube Inc. promotional video clips for some of its shows including “The Office” and “Saturday Night Live.”

- The US House of Representatives this week will probably cancel a 25-year restriction on oil and gas exploration along portions of the US coast.

- Google(GOOG) will introduce a test version of its GBuy online-payment service as early as this week to challenge EBay’s(EBAY) PayPal online-payment service.

- Time Warner’s(TWX) Warner Bros. will distribute movies and television shows over the Internet under an agreement to use Guba’s search engine and video-sharing network.

- US investors have been playing it safe, opting for multi-cap or all-cap mutual funds rather than large-cap or small-cap funds.

- Sony’s(SNE) personal music player is still struggling to compete with Apple Computer’s(AAPL) iPod, citing Sony president Ryoji Chubachi.

- A Coca-Cola bottler and MasterCard Intl. plan to site 1,000 vending machines in the Philadelphia area which will be able to accept credit and debit cards.

Washington Post:

- President Bush asked US Homeland Security Secretary Michael Chertoff to overhaul the nation’s Emergency Alert System because of weaknesses revealed after the Sept. 11, 2001, terrorist attacks and Hurricane Katrina in 2005.

Miami Herald:

- “Full-house” generators have become an important feature for high-priced South Florida homes after six major hurricanes in two years.

NY Times:

- Univision Communications(UVN) may accept a bid worth about $36.25 a share, or $11 billion, from a group led by billionaire Haim Saban.

USA Today:

- Real estate in more than 30 major metro areas, including Washington, Atlantic City, New York, Las Vegas, Phoenix, Sacramento and San Diego, more than doubled since 2000. Home prices will rise another 5% this year, according to the paper.

Handelsblatt:

- Kohlberg Kravis Roberts raised $15.5 billion for the biggest ever private equity fund.

Xinhua News:

- China’s government may fine media organizations as much as $12,501 for unauthorized reporting of emergencies under a draft law legislators started debating yesterday.

Existing Home Sales Fall Slightly, Consumer Confidence Rises

- Existing Home Sales for May fell to 6.67M versus estimates of 6.6M and 6.75M in April.

- Consumer Confidence for June rose to 105.7 versus estimates of 103.8 and 104.7 in May.

- Consumer Confidence for June rose to 105.7 versus estimates of 103.8 and 104.7 in May.

BOTTOM LINE: Sales of previously owned homes in the US fell in May to the lowest since January as higher mortgage rates sapped demand, Bloomberg said. The supply of homes for sale is now up to May 1997 levels. The median price of an existing home rose 6% in May from a year earlier to $230,000. Sales fell 4.2% in the Northeast and 3.8% in the Midwest. They rose .4% in the South and rose .7% in the West. This is more evidence of a “soft-landing” in housing.

Confidence among US consumers rose more than forecast in June as Americans’ outlook for the job market improved, Bloomberg said. The expectations component of the index rose to 87.6 from 85.1 the prior month. The employment component of the index rose to 15.6%, the highest since August. 3% of consumers said they plan to buy a home, up from 2.9% the prior month. I continue to expect consumer confidence to make new cycle highs over the intermediate-term as stocks rise, energy prices fall, irrational pessimism lifts further, Iraq improves, the job market remains healthy, long-term rates remain low by historic standards and inflation decelerates.

Monday, June 26, 2006

Tuesday Watch

Late-Night Headlines

Bloomberg:

- General Motors(GM) persuaded about 35,000 US union workers to retire, a move aimed at helping return the company’s financial health.

- Merrill Lynch(MER), Morgan Stanley(MS) and Lehman Brothers(LEH), three of the world’s biggest securities firms, sued Theflyonthewall.com Web site, claiming it “pirated” their equity research.

- Take-Two(TTWO) said it received requests from the NY District Attorney for documents related to statements about earnings and hidden sex scenes in its “Grand Theft Auto” video game.

- Seven present and former pro football players sued the NFL and the NFL Players Assoc., saying the organizations recommended unfit financial advisers and caused them to lose $20 million.

- South Korea’s government said it will take “measures” against North Korea in the event the country tests a long-range missile, as President Bush told North Korea to refrain from such a “provocative” act.

- Japan will start receiving its first shipments from the $13 billion Sakhalin-1 oil and natural gas project this year, helping the world’s second-largest economy ease dependence on imports from the Middle East.

Financial Times:

- A US proposal to tighten restrictions on exports of technology products to China is expected to draw criticism from Beijing and protests from US industry groups.

Security Times:

- China should raise interest rates further to curb lending, citing Chen Dongqi, deputy director of the Academy of Macroeconomic Research, a government-affiliated body.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are +.25% to +1.0% on average.

S&P 500 indicated +.05%.

NASDAQ 100 indicated +.10%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (FLS)/.49

- (FRE)/1.21

- (FUL)/.69

- (NKE)/1.40

Upcoming Splits

- None of note

Economic Releases

10:00 am EST

- Existing Home Sales for May are estimated to fall to 6.6M versus 6.76M in April.

- Consumer Confidence for June is estimated to rise to 103.8 versus a reading of 103.2 in May.

Bloomberg:

- General Motors(GM) persuaded about 35,000 US union workers to retire, a move aimed at helping return the company’s financial health.

- Merrill Lynch(MER), Morgan Stanley(MS) and Lehman Brothers(LEH), three of the world’s biggest securities firms, sued Theflyonthewall.com Web site, claiming it “pirated” their equity research.

- Take-Two(TTWO) said it received requests from the NY District Attorney for documents related to statements about earnings and hidden sex scenes in its “Grand Theft Auto” video game.

- Seven present and former pro football players sued the NFL and the NFL Players Assoc., saying the organizations recommended unfit financial advisers and caused them to lose $20 million.

- South Korea’s government said it will take “measures” against North Korea in the event the country tests a long-range missile, as President Bush told North Korea to refrain from such a “provocative” act.

- Japan will start receiving its first shipments from the $13 billion Sakhalin-1 oil and natural gas project this year, helping the world’s second-largest economy ease dependence on imports from the Middle East.

Financial Times:

- A US proposal to tighten restrictions on exports of technology products to China is expected to draw criticism from Beijing and protests from US industry groups.

Security Times:

- China should raise interest rates further to curb lending, citing Chen Dongqi, deputy director of the Academy of Macroeconomic Research, a government-affiliated body.

Late Buy/Sell Recommendations

- None of note

Night Trading

Asian Indices are +.25% to +1.0% on average.

S&P 500 indicated +.05%.

NASDAQ 100 indicated +.10%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (FLS)/.49

- (FRE)/1.21

- (FUL)/.69

- (NKE)/1.40

Upcoming Splits

- None of note

Economic Releases

10:00 am EST

- Existing Home Sales for May are estimated to fall to 6.6M versus 6.76M in April.

- Consumer Confidence for June is estimated to rise to 103.8 versus a reading of 103.2 in May.

BOTTOM LINE: Asian indices are higher, boosted by commodity and technology stocks in the region. I expect US equities to open modestly higher and to maintain gains into the afternoon. The Portfolio is 75% net long heading into the day.

Stocks Finish at Session Highs on Light Volume ahead of Fed Hike

Indices

S&P 500 1,250.56 +.49%

DJIA 11,045.28 +.51%

NASDAQ 2,133.67 +.58%

Russell 2000 698.64 +1.23%

Wilshire 5000 12,580.73 +.54%

S&P Barra Growth 578.82 +.35%

S&P Barra Value 670.0 +.62%

Morgan Stanley Consumer 603.61 +.42%

Morgan Stanley Cyclical 809.61 +.37%

Morgan Stanley Technology 487.04 +.14%

Transports 4,772.36 -.01%

Utilities 407.99 +.45%

Put/Call .74 -25.25%

NYSE Arms .75 +.79%

Volatility(VIX) 15.61 -1.76%

ISE Sentiment 208.00 +55.22%

US Dollar 86.52 -.41%

CRB 337.37 +.70%

Futures Spot Prices

Crude Oil 71.64 -.22%

Unleaded Gasoline 217.88 +2.41%

Natural Gas 5.98 +.34%

Heating Oil 197.50 -.20%

Gold 587.90 +.03%

Base Metals 207.99 +3.55%

Copper 322.15 -.36%

10-year US Treasury Yield 5.23% +.28%

Leading Sectors

Homebuilders +1.80%

Gold & Silver +1.12%

Energy +1.11%

Lagging Sectors

Airlines -.52%

Gaming -.60%

Disk Drives -.64%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

Banc of America:

- Rated (COST) Buy, target $63.

Piper Jaffray:

- Rated (OPTN) Outperform, target $14.

Lehman Brothers:

- Upgraded IT Consulting & Computer Services Sector to Positive.

Afternoon/Evening Headlines

Bloomberg:

- US Treasury 10-year notes fell a ninth consecutive day as the prospect of a 17th straight interest-rate hike by the Fed this week prompted investors to demand higher returns.

- US stocks rose as companies’ plans for $88 billion in takeovers outweighed concern that the Fed will hike rates further.

- Natural gas fell to the lowest closing price in a month in NY as moderate temperatures limited demand for the power-plant fuel.

S&P 500 1,250.56 +.49%

DJIA 11,045.28 +.51%

NASDAQ 2,133.67 +.58%

Russell 2000 698.64 +1.23%

Wilshire 5000 12,580.73 +.54%

S&P Barra Growth 578.82 +.35%

S&P Barra Value 670.0 +.62%

Morgan Stanley Consumer 603.61 +.42%

Morgan Stanley Cyclical 809.61 +.37%

Morgan Stanley Technology 487.04 +.14%

Transports 4,772.36 -.01%

Utilities 407.99 +.45%

Put/Call .74 -25.25%

NYSE Arms .75 +.79%

Volatility(VIX) 15.61 -1.76%

ISE Sentiment 208.00 +55.22%

US Dollar 86.52 -.41%

CRB 337.37 +.70%

Futures Spot Prices

Crude Oil 71.64 -.22%

Unleaded Gasoline 217.88 +2.41%

Natural Gas 5.98 +.34%

Heating Oil 197.50 -.20%

Gold 587.90 +.03%

Base Metals 207.99 +3.55%

Copper 322.15 -.36%

10-year US Treasury Yield 5.23% +.28%

Leading Sectors

Homebuilders +1.80%

Gold & Silver +1.12%

Energy +1.11%

Lagging Sectors

Airlines -.52%

Gaming -.60%

Disk Drives -.64%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Economic Calendar

Timely Economic Charts

GuruFocus.com

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

Banc of America:

- Rated (COST) Buy, target $63.

Piper Jaffray:

- Rated (OPTN) Outperform, target $14.

Lehman Brothers:

- Upgraded IT Consulting & Computer Services Sector to Positive.

Afternoon/Evening Headlines

Bloomberg:

- US Treasury 10-year notes fell a ninth consecutive day as the prospect of a 17th straight interest-rate hike by the Fed this week prompted investors to demand higher returns.

- US stocks rose as companies’ plans for $88 billion in takeovers outweighed concern that the Fed will hike rates further.

- Natural gas fell to the lowest closing price in a month in NY as moderate temperatures limited demand for the power-plant fuel.

BOTTOM LINE: The Portfolio finished higher today on gains in my Semi longs, Retail longs and Biotech longs. I did not trade in the final hour, thus leaving the Portfolio 75% net long. The tone of the market was positive today as the advance/decline line finished higher, most sectors rose and volume was very light. Measures of investor anxiety were mostly lower into the close. Overall, today's market performance was mildly bullish. A substantial amount of market uncertainty revolves around housing and inflation. We had one very positive data point on housing today and we get another one tomorrow. Personal incomes and spending are released Friday, which are related to the housing slowdown. At this point, most expect the Fed to raise 25 basis points and make hawkish statements in their ensuing policy statement. While I am very certain that a 25 basis-point hike is in the offing, I am not as certain of the tone of the policy statement. I wouldn't be surprised to see more dovish statements than most expect. Finally, the PCE Core, the Fed's favorite inflation gauge, is released on Friday. Bottom line, the market hates uncertainty and some very key releases are on tap this week. The lifting of this uncertainty, combined with depressed investor sentiment and substantial losses in many stocks this quarter will likely lead to short profit-taking and long bargain-hunting on Thursday and Friday. Thus, I expect stocks to finish the week on a positive note.

Stocks Modestly Higher into Final Hour, Led by Homebuilders

BOTTOM LINE: The Portfolio is slightly higher into the final hour on gains in my Retail longs, Internet longs and Semi longs. I have not traded today, thus leaving the Portfolio 75% net long. The tone of the market is slightly positive as the advance/decline line is modestly higher, sector performance is mostly positive and volume is light. The latest data from the NYSE show short interest as a percentage of total share outstanding is 2.4%. This is back to an all-time record high and corresponds with other data showing excessive levels of pessimism. I expect US stocks to trade mixed-to-higher into the close from current levels on short-covering and bargain hunting ahead of a number of important releases.

Today's Headlines

Bloomberg:

- The world is winning the war on drugs, according to a United Nations report that said opium production might soon be eradicated in Asia’s notorious “Golden Triangle” and coca cultivation in the Andean region of South American has decreased 25% since 2000.

- Shares of Inco Ltd.(N) and Falconbridge Ltd. rose after reports that Phelps Dodge(PD) will acquire the Canadian nickel miners for $40 billion in cash and stock.

- The US Supreme Court agreed to consider a bid by environmentalists and 12 states to force the Environmental Protection Agency to regulate car and truck emissions that may contribute to possible global warming.

- Shares of Zimmer Holdings(ZMH) and Biomet(BMET) fell after the two markers of artificial joints disclosed the US Dept. of Justice is investigating the $7 billion-a-year orthopedics industry.

Wall Street Journal:

- A report detailing the US Army’s recovery of at least 500 weapons of mass destruction in Iraq starting in 2003 should have been disclosed to the public earlier, Senator Rick Santorum and Representative Peter Hoekstra said. The National Group Intelligence Center agreed to declassify six “key points” of a report on the chemical weapons recovery in Iraq, information requested for nine weeks before getting a response.