Click here for the Weekly Wrap by Briefing.com.

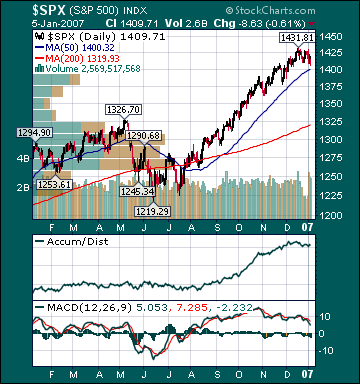

BOTTOM LINE: Overall, last week's market performance was mildly bearish. The advance/decline line fell, sector performance was mixed and volume was heavy on the week. Measures of investor anxiety were mixed. The AAII percentage of Bulls rose to 49.14% last week from 46.0% the prior week. This reading is slightly above average levels. The AAII percentage of Bears fell to 29.31% this week from 36.0% the prior week. This reading is now at average levels. The 10-week moving average of the percentage of Bears is currently 37.1%, an above-average level. The 10-week moving average of the percentage of Bears peaked at 43.0% at the major bear market low during 2002. Moreover, the 50-week moving average of the percentage of Bears is 37.0%, a very high level seen during only two other periods in U.S. history.

I continue to believe that steadfastly high bearish sentiment in many quarters is mind-boggling, considering the S&P 500's 16.4% rise in less than six months, one of the best August/September/October runs in U.S. history, the fact that the Dow made another all-time high last week and that we are in the early stages of what is historically a very strong period for U.S. stocks after a midterm election. Despite recent gains, the forward P/E on the S&P 500 is a very reasonable 16.0 due to the historic run of double-digit profit growth increases, which are poised to continue when fourth quarter earnings come in over the next few weeks. Bears still remain stunningly complacent, in my opinion. As I have said many times over the last few months, they see every pullback as a major top and every move higher as just another shorting/selling opportunity.

As well, there are many other indicators registering high levels of investor skepticism regarding recent stock market gains. The 50-day moving average of the ISE Sentiment Index just crossed above the 200-day moving average for the first time since November 2005. The ISE Sentiment Index plunged to depressed levels again several times last week. Nasdaq and NYSE short interests are very close to record highs. Moreover, public short interest continues to soar to records, and U.S. stock mutual funds have seen outflows for most of the last year, according to AMG Data Services. Finally, investment blogger bullish sentiment is hovering just above record lows. There is still a high wall of worry for stocks to climb substantially from current levels as the general public remains very skeptical of this bull market.

I continue to believe this is a direct result of the strong belief by the herd that the U.S. is in a long-term trading range or secular bear environment. There is still overwhelming evidence that investment sentiment by the public regarding U.S. stocks has never been this poor in history, with the Dow registering all-time highs almost weekly. I still expect the herd to finally embrace the current bull market this year, which should result in another meaningful move higher in the major averages as the S&P 500 breaks out to an all-time high to join the Dow and Russell 2000. Only in a "negativity bubble" could Wall Street strategists' consensus predictions of a 7% gain for the S&P 500 this year be characterized as "very bullish" by the many bearish pundits. I continue to believe the coming bullish shift in long-term sentiment with respect to U.S. stocks will result in the "mother of all short-covering rallies."

The average 30-year mortgage rate was unch. at 6.18%, which is 62 basis points below July highs. I still believe housing is in the process of stabilizing at relatively high levels. The Fed’s Minehan said this week that recent data suggest a “bottoming” in real estate. A belief shared by former Fed Chairman Alan Greenspan, current Fed Chairman Ben Bernanke and several current Fed members. Mortgage applications rose another 3.6% this week and continue to trend higher with the decline in mortgage rates and healthy job market. The Mortgage Bankers Association said last month that the US housing market will “fully regain its footing” by the middle of 2007. Moreover, the California Building Industry Association on Friday gave an upbeat forecast for housing this year, saying production would be near last year’s brisk levels.

As well, housing inventories have been trending lower and homebuilding equities have been moving higher. The Housing Index(HGX) has risen 21.5% from July lows. The Case-Schiller housing futures have improved substantially and are now projecting a 2.1% decline in the average home price by May, up from projections of a 5.2% decline a couple of months ago. Considering the median house has appreciated over 50% during the last few years with record high US home ownership, this would be considered a “soft landing.” The overall negative effects of housing on the US economy and the potential for significant price drops are still being exaggerated by the many bears in hopes of dissuading buyers from stepping up, in my opinion. Housing and home equity extractions have been slowing substantially for well over a year and have been mostly offset by many other very positive aspects of the US economy.

Home values are more important than stock prices to the average American, but the median home has barely declined in value after a historic run-up, while the S&P 500 has risen 11.7% over the last year and 90.2% since the Oct. 4, 2002 low. Americans’ median net worth is still very close to or at record high levels as a result, a fact that is generally unrecognized or minimized by the record number of stock market participants that feel it is in their financial and/or political interests to paint a bleak picture of America. Moreover, energy prices are down significantly, consumer spending remains relatively healthy, unemployment is low by historic standards, interest rates are very low, inflation is below average rates, stocks are surging and wages are rising. The economy has created 840,000 jobs in the last five months. Challenger, Gray & Christmas reported this week that December job cuts plunged 49.3% from year-ago levels. As well, the Monster Employment Index is just off record highs. Moreover, the unemployment rate is a historically low 4.5%, down from 5.1% in September 2005, notwithstanding fewer real estate-related jobs and significant auto production cutbacks. Consumer spending is around long-term average levels and looks poised to remain healthy over the intermediate-term.

The Consumer Price Index for November rose 2.0% year-over-year, down from a 4.7% increase in September of 2005. This is substantially below the long-term average of around 3%. Moreover, the CPI has only been lower during 4 other periods since the mid-1960s. Many other measures of inflation have recently shown substantial deceleration. The Producer Price Index for November rose a historically low .9% year-over-year. Most measures of Americans’ income growth are now more than twice the rate of inflation. Americans’ Average Hourly Earnings rose 4.2% in December, substantially above the 3.2% 20-year average. The recent plunge in many commodities should eventually result in the complete debunking of the problematic inflation myth that so many have perpetuated endlessly over the last couple of years.

The benchmark 10-year T-note yield fell 3 basis points on the week on diminishing inflation concerns and lingering economic worries. In my opinion, investors’ continuing fears over an economic “hard landing” are misplaced. The ISM Manufacturing Index improved in December and is now registering expansion. Moreover, the ISM’s semi-annual forecast was released recently and gave an upbeat assessment of expected manufacturing activity this year. The ISM Non-Manufacturing Index, which is a gauge of the vast majority of U.S. economic activity, came in at a healthy 57.1 for December. Manufacturing accounts for roughly 12% of US economic growth, while consumer spending accounts for about 70% of growth.

U.S. GDP growth came in at 1.1% and 0.7% during the first two quarters of 1995. The ISM Manufacturing Index fell below 50, which signals a contraction in activity, during May 1995. It stayed below 50, reaching a low of 45.5, until August 1996. During that period, the S&P 500 soared 31% as the P/E multiple expanded from 16.0 to 17.2. This was well before the stock market bubble began to inflate. As well, manufacturing was more important to overall US economic growth at that time. Stocks can and will rise as P/E multiples expand, even with more average economic and earnings growth. The S&P 500's P/E has contracted for three straight years. A recent Morgan Stanley report concluded that the S&P 500's P/E has only contracted for four consecutive years twice since 1905. The report says that each point of multiple expansion is equivalent to a 6.6% gain in the S&P 500. As I have said many times before, P/E multiple expansion is the bears' worst nightmare.

Weekly retail sales rose an average 3.2% for the week. Spending is poised to remain strong on lower energy prices, very low long-term interest rates, a rising stock market, healthy job market, decelerating inflation and more optimism. The current conditions component of the December Univ. of Mich. Consumer Confidence Index, which gauges whether or not consumers feel it is a good time to buy big-ticket items, rose to its highest level since March. As well, the Conference Board’s Consumer Confidence reading for December came in at the second highest this cycle.

The CRB Commodities Index, the main source of inflation fears, has declined 13.3% over the last 12 months and is down 20.3% from May highs despite a historic flood of capital into commodity funds and numerous potential upside catalysts. Oil has declined $22/bbl from July highs. Last year, oil rose $2.05/bbl. on the first trading day of the year and $7.40/bbl. through the first three weeks of trading as commodity funds, flush with new capital, drove futures prices higher. I suspect, given the average commodity hedge fund fell around double-digits last year as the CRB Index dropped 7.4%, that many energy-related funds saw outflows at year-end. Oil has declined over $5/bbl. in the first four trading days of the new year so far. I continue to believe inflation fears have peaked for this cycle as global economic growth stabilizes around average levels, unit labor costs remain subdued and the mania for commodities continues to reverse course.

The EIA reported this week that gasoline supplies rose substantially more than expectations even as refinery utilization increased only slightly. U.S. gasoline supplies are at high levels for this time of the year. Gasoline futures fell substantially for the week and have plunged 48.6% from September 2005 highs even as some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. The still very elevated level of gas prices, related to crude oil production disruption speculation by investment funds, will further dampen global fuel demand, sending gas prices still lower over the intermediate-term.

The 10-week moving-average of US oil inventories is approaching 8-year highs. Since December 2003, global oil demand is only up 2%, despite booming global growth, while global supplies have increased 6%, according to the Energy Intelligence Group. OPEC said recently that global crude oil supply would exceed demand by 100 million barrels by the second quarter of this year. Moreover, worldwide oil inventories are poised to begin increasing at an accelerated rate over the next year. One of the main reasons I believe OPEC has been slow to actually meet their pledged cuts has been the fear of losing market share to non-OPEC countries. I continue to believe oil is priced at extremely elevated levels on record speculation by investment funds, not fundamentals.

The Amaranth Advisors hedge fund blow-up is a prime example of the extent to which many investment funds have been speculating on ever higher energy prices through futures contracts, thus driving the price of the underlying commodity to absurd levels. Amaranth, a multi-strategy hedge fund, lost about $6.5 billion of its $9.5 billion under management in less than two months speculating mostly on higher natural gas prices. I continue to believe a number of other funds will experience similar fates over the coming months after managers “pressed their bets” in hopes of making up for recent poor performance, which will further pressure energy prices as these funds unwind their leveraged long positions to meet rising investor redemptions.

Recently, Cambridge Energy Research, one of the most respected energy research firms in the world, put out a report that drills gaping holes in the belief by most investors of imminent "peak oil" production. Cambridge said that its analysis indicates that the remaining global oil base is actually 3.74 trillion barrels, three times greater than "peak oil" theory proponents say and that the "peak oil" theory is based on faulty analysis. I suspect the contango that still exists in energy futures, which encourages hoarding, will begin to reverse over the coming months as more investors come to the realization that the "peak oil" theory is hugely flawed, global storage fills, and Chinese/US demand slows.

A major top in oil is already in place as global crude oil storage capacity utilization is running around 98%. Recent OPEC production cuts are likely resulting in a complete technical breakdown in crude. Demand destruction is already pervasive globally and will only intensify over the coming years as many more alternative energy projects come to the fore. Moreover, many Americans feel as though they are helping fund terrorism or hurting the environment every time they fill up their gas tanks. I do not believe we will ever again see the demand for gas-guzzling vehicles that we saw in recent years, even if gas prices plunge further from current levels, as I expect. OPEC production cuts, with oil still at very high levels and weakening global growth, only further deepens resentment towards the cartel and will result in even greater long-term demand destruction. Finally, as the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should continue heading meaningfully lower over the intermediate-term, notwithstanding OPEC production cuts. Oil has already begun another significant downturn. I suspect crude will eventually fall to levels that most investors deemed unimaginable just a few months ago during the next significant global economic downturn.

Natural gas inventories fell less than expectations this week. Prices for the commodity declined again as record investment fund speculation continues to subside with supplies now 15.3% above the 5-year average and at all-time high levels for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have collapsed 60.7% since December 2005 highs. Notwithstanding this decline, natural gas anywhere near current prices is ridiculous with inventories poised to hit new record highs this year. The long-term average price of natural gas is $4.63 with inventories at much lower levels than currently.

Gold fell substantially on the week as the US dollar rose, inflation concerns subsided further and investment fund speculation for all commodities waned. Gold, natural gas, oil and copper all look both fundamentally and technically weak. The US dollar gained on stronger US economic data and short-covering. I continue to believe there is very little chance of another Fed rate hike anytime soon. An eventual cut is likely this year as inflation continues to decelerate substantially. A Fed rate cut should actually boost the dollar as currency speculators anticipate faster US economic growth. Moreover, last month’s net long-term TIC flows report showed foreign investors’ demand for US securities remains very strong.

Technology stocks outperformed for the week as “growth” companies substantially outpaced “value”. Energy-related stocks underperformed significantly as the fundamentals continue to weaken for the over-owned group and a couple of high-profile companies gave negative forecasts. S&P 500 profit growth for the third quarter came in around 20% versus a long-term historical average of 7%, according to Thomson Financial. This marks the 17th straight quarter of double-digit profit growth, the best streak since recording keeping began in 1936. Moreover, another double-digit gain is likely for the fourth quarter. Just a few months ago many investors expected profit growth to fall to the low single digits last year. Despite a 90.2% total return(which is equivalent to a 16.3% average annual return) for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 16.0. The 20-year average p/e for the S&P 500 is 23.0.

Current stock prices are still providing longer-term investors very attractive opportunities, in my opinion. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. A CSFB report late last year confirmed this view. The report concluded that on a price-to-cash flow basis growth stocks are cheaper than value stocks for the first time since at least 1977. The entire decline in the S&P 500’s p/e, since the bubble burst in 2000, is attributable to growth stock multiple contraction. I still expect the most overvalued economically sensitive and emerging market stocks to continue underperforming over the intermediate-term as the manias for those shares subside as global growth slows to more average rates. I continue to believe a chain reaction of events has begun that will result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels, notwithstanding recent gains. One of the characteristics of the current “negativity bubble” is that most potential positives are undermined, downplayed or completely ignored, while almost every potential negative is exaggerated, trumpeted and promptly priced in to stock prices. Furthermore, this “irrational pessimism” by investors is resulting in a dramatic decrease in the supply of stock as companies buy back shares, IPOs are pulled and secondary stock offerings are canceled. Booming merger and acquisition activity is also greatly constricting the supply of stock. Many commodity funds, which have received a historic flood of capital inflows over the last few years are likely now seeing redemptions as the CRB Index heads into bear market territory. Some of this capital will likely find its way back to US stocks. As well, money market funds are brimming with cash. There is massive bull firepower available on the sidelines for US equities at a time when the supply of stock has contracted.

I continue to believe the many U.S. stock market bears and most bulls raised cash in December in anticipation of a pullback this month. Considering the overwhelming majority of investment funds failed to meet the S&P 500's 15.8% return last year, I suspect most portfolio managers have a very low threshold of pain this year for falling substantially behind their benchmark once again. Rising optimism for a Fed rate cut, a stronger US dollar, lower commodity prices, seasonal strength, decelerating inflation readings, a pick-up in consumer spending, lower long-term rates, increased consumer/investor confidence, short-covering, investment manager performance anxiety, rising demand for US stocks and the realization that economic growth is poised to accelerate back to around average levels in the second half of the year should provide the catalysts for another substantial push higher in the major averages over the intermediate-term as p/e multiples expand substantially. Another strong performance by US equities is likely this year. Finally, the ECRI Weekly Leading Index surged this week and is forecasting a modest acceleration in US economic activity.

*3-day % Change

No comments:

Post a Comment