Bloomberg:

- Google today will start offering customizable e-mail and calendar software to businesses and universities in a bid to lure more corporate customers and develop new sources of revenue.

- EBay(EBAY) chose Google(GOOG) to run advertising on its Web sites outside the US to tap a larger share of global online advertising market.

- Kinder Morgan(KMI) accepted an increased offer of $15 billion from a group led by Richard Kinder, the former Enron executive.

- Iran’s President Ahmadinejad told German Chancellor Merkel that the Nazi Holocaust may be an “excuse” by the nations that won World War II to keep Germans “ashamed.”

- US Bankruptcy filings fell to the lowest level in five years. Full-year 2006 filings will be the fewest since 1986.

- Crude oil fell more than $2/bbl. and natural gas plunged 10% as Tropical Storm Ernesto veered away from oil- and gas-producing areas in the Gulf of Mexico that were damaged by Hurricane Katrina a year ago.

Wall Street Journal:

- Royal Dutch Shell Plc and Chevron(CVX) are set to begin tests to extract oil from the US Rocky Mountains as high oil prices spur unconventional new methods of oil extraction.

- CBS Corp.(CBS) is to install “glueless” posters, projectors, light boxes and flat-paneled television screens in a $3 billion outdoor advertising contract with the London Underground as the industry adapts to new technology and intense competition.

- Foreign companies selling shares in IPOs on US exchanges have raised $5.85 billion so far this year, the highest year-to-date amount since the tech bubble burst in 2000, citing Dealogic Holdings.

- Terex is benefiting from a shortage in the large tires needed for mining trucks, citing the CEO.

- The NYSE’s plans to lift limits on the amount of stock traded electronically at the exchange may sideline trading floor specialists and brokers and hurt profit.

- UN Security Council Resolution 1701 failed to address the kidnapping of the two Israeli soldiers that caused fighting to break out between Israel and Lebanon, the parents of slain hostage Daniel Pearl wrote.

Washington Post:

- Biometric identification cards, containing information such as fingerprints and retinal scans, will be issued to US government employees in October to increase security.

NY Daily News:

- The recently discovered terrorist plot in London has created opportunities for bargain travel.

Star-Ledger:

- New Jersey taxes under the state’s new budget increased 5% over 2005, the most in the US.

L’Orient le Jour:

- 51% of Lebanese want Hezbollah to lay down its arms, citing an opinion poll by Ipsos SA.

Monday, August 28, 2006

Sunday, August 27, 2006

Monday Watch

Weekend Headlines

Bloomberg:

- The average US gasoline pump price fell 15.5 cents in the past two weeks to $2.87/gallaon as inventory of the fuel rose, Trilby Lundberg said, citing her survey of about 7,000 filling stations nationwide.

- Two Fox News journalists were freed in the Gaza Strip today after being kidnapped two weeks ago by a Palestinian group that demanded the release of Muslims held in US prisons.

- A Delta Air Lines Comair commuter plane crashed shortly after takeoff at Blue Grass Airport in Lexington, Kentucky, killing 49 and critically injuring one.

- Florida ordered the mandatory evacuation today of visitors in the Florida Keys as Tropical Storm Ernesto tracked toward the state from the Carribean.

- Energy companies have only evacuated some non-essential staff from platforms in the Gulf of Mexico as projections show Tropical Storm Ernesto moving away from the main offshore oil and gas producing regions.

- Hedge funds and other speculators are wagering more than ever on a continuing rally in US Treasuries.

- Gold’s appeal is fading as a slowing global economy and lower oil prices ease inflation concerns.

- FedEx(FDX) and the union for its pilots reached a tentative contract agreement after almost 30 months of talks.

- The dollar gained against the euro and yen this week as traders said bets against the US currency grew excessive.

- Wal-Mart Stores(WMT) said August same-store sales in the US rose about 2.7%, which bettered last month’s 2.4% gain. The company had forecast an increase of 1-3%.

Barron’s:

- Dell(DELL) plans to spend $150 million to improve its customer service.

NY Times:

- Sybase Inc.(SY) CEO Chen wants the company’s wireless business to have as much annual revenue as its database-software unit in three to five years, or about $500 million.

- US schools this year will have about 55 million students, the most in the nation’s history, amid an influx of immigrants similar to the early 20th century.

Business Week:

- Housing: The Roof Won’t Collapse on the US Economy

Detroit News:

- Ford Motor(F) is considering selling a “significant” stake in its Ford Credit finance unit.

InfoWorld:

- SAP’s CEO sees huge overcapacity being generated in China and an economic downturn there in 2008.

Sueddeutsche Zeitung:

- Electronic Arts(ERTS) is seeking to buy German rivals to boost its market share, citing the company’s Germany CEO.

Berliner Zeitung:

- A planned tax increase will act as a “major brake” on Germany’s economic expansion next year, just as the economy shows signs of recovering, citing Gustav Horn, chief economist at the IMK economic research institute.

Emirates Today:

- Monster.com, the job-listing service operated by Monster Worldwide(MNST), expects to increase 500% the number of listings on its new Gulf portal this year.

Al-Ahram:

- Hezbollah and Israel will swap prisoners within two to three weeks in an arrangement orchestrated by Germany.

Handelsblatt:

- Rio Tinto Group(RTP) CEO Clifford expects commodity prices to drop.

Commercial Times:

- AU Optronics(AUO) expects demand for its liquid-crystal displays to rise in the fourth quarter, citing company chairman KY Lee. Production lines at AU are running at capacity on lower inventories and rising orders for LCDs used in televisions.

Weekend Recommendations

Barron's:

- Had positive comments on (WRNC), (CTX), (TOL), (LEN), (KBH), (HOT), (HLT), (CBS), (ANAD) and (PHM).

Night Trading

Asian indices are -.50% to +.25% on average.

S&P 500 indicated -.02%

NASDAQ 100 indicated -.02%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (CAE)/.80

Upcoming Splits

- None of note

Economic Releases

- None of note

Bloomberg:

- The average US gasoline pump price fell 15.5 cents in the past two weeks to $2.87/gallaon as inventory of the fuel rose, Trilby Lundberg said, citing her survey of about 7,000 filling stations nationwide.

- Two Fox News journalists were freed in the Gaza Strip today after being kidnapped two weeks ago by a Palestinian group that demanded the release of Muslims held in US prisons.

- A Delta Air Lines Comair commuter plane crashed shortly after takeoff at Blue Grass Airport in Lexington, Kentucky, killing 49 and critically injuring one.

- Florida ordered the mandatory evacuation today of visitors in the Florida Keys as Tropical Storm Ernesto tracked toward the state from the Carribean.

- Energy companies have only evacuated some non-essential staff from platforms in the Gulf of Mexico as projections show Tropical Storm Ernesto moving away from the main offshore oil and gas producing regions.

- Hedge funds and other speculators are wagering more than ever on a continuing rally in US Treasuries.

- Gold’s appeal is fading as a slowing global economy and lower oil prices ease inflation concerns.

- FedEx(FDX) and the union for its pilots reached a tentative contract agreement after almost 30 months of talks.

- The dollar gained against the euro and yen this week as traders said bets against the US currency grew excessive.

- Wal-Mart Stores(WMT) said August same-store sales in the US rose about 2.7%, which bettered last month’s 2.4% gain. The company had forecast an increase of 1-3%.

Barron’s:

- Dell(DELL) plans to spend $150 million to improve its customer service.

NY Times:

- Sybase Inc.(SY) CEO Chen wants the company’s wireless business to have as much annual revenue as its database-software unit in three to five years, or about $500 million.

- US schools this year will have about 55 million students, the most in the nation’s history, amid an influx of immigrants similar to the early 20th century.

Business Week:

- Housing: The Roof Won’t Collapse on the US Economy

Detroit News:

- Ford Motor(F) is considering selling a “significant” stake in its Ford Credit finance unit.

InfoWorld:

- SAP’s CEO sees huge overcapacity being generated in China and an economic downturn there in 2008.

Sueddeutsche Zeitung:

- Electronic Arts(ERTS) is seeking to buy German rivals to boost its market share, citing the company’s Germany CEO.

Berliner Zeitung:

- A planned tax increase will act as a “major brake” on Germany’s economic expansion next year, just as the economy shows signs of recovering, citing Gustav Horn, chief economist at the IMK economic research institute.

Emirates Today:

- Monster.com, the job-listing service operated by Monster Worldwide(MNST), expects to increase 500% the number of listings on its new Gulf portal this year.

Al-Ahram:

- Hezbollah and Israel will swap prisoners within two to three weeks in an arrangement orchestrated by Germany.

Handelsblatt:

- Rio Tinto Group(RTP) CEO Clifford expects commodity prices to drop.

Commercial Times:

- AU Optronics(AUO) expects demand for its liquid-crystal displays to rise in the fourth quarter, citing company chairman KY Lee. Production lines at AU are running at capacity on lower inventories and rising orders for LCDs used in televisions.

Weekend Recommendations

Barron's:

- Had positive comments on (WRNC), (CTX), (TOL), (LEN), (KBH), (HOT), (HLT), (CBS), (ANAD) and (PHM).

Night Trading

Asian indices are -.50% to +.25% on average.

S&P 500 indicated -.02%

NASDAQ 100 indicated -.02%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (CAE)/.80

Upcoming Splits

- None of note

Economic Releases

- None of note

BOTTOM LINE: Asian Indices are mostly lower, weighed down by commodity and technology shares in the region. I expect US stocks to open mixed and to rally into the afternoon, finishing modestly higher. The Portfolio is 100% net long heading into the week.

Weekly Outlook

Click here for The Week Ahead by Reuters

There are a number of economic reports of note and a few significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - None of note

Tues. - Consumer Confidence, Minutes of Aug. 8 FOMC Meeting

Wed. - ADP Employment Change, Preliminary 2Q GDP, Preliminary 2Q GDP Price Index, Preliminary Personal Consumption, Preliminary Core PCE

Thur. - Personal Income, Personal Spending, PCE Deflator, PCE Core, Initial Jobless Claims, Help Wanted Index, Chicago Purchasing Manager, Factory Orders

Fri. - Change in Non-farm Payrolls, Unemployment Rate, Avg. Hourly Earnings, Univ. of Mich. Consumer Confidence, Construction Spending, ISM Manufacturing, ISM Prices Paid, Pending Home Sales, Total Vehicle Sales

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - BISYS Group(BSG), Cascade(CAE)

Tues. - ADC Telecom(ADCT), Dycom Industries(DY), FuelCell(FCEL), Micros Systems(MCRS), Novell(NOVL), Semtech(SMTC)

Wed. - JDS Uniphase(JDSU), Tivo Inc.(TIVO), United Natural Foods(UNFI)

Thur. - Brown-Forman(BF/A), Cheesecake Factory(CAKE), Ciena Corp.(CIEN), Del Monte(DLM), Dollar General(DG), H&R Block(HRB), HJ Heinz(HNZ), Joy Global(JOYG), Nvidia Corp.(NVDA), Omnivision Tech(OVTI), Tiffany(TIF), Wind River(DRIV), Zale Corp.(ZLC)

Fri. - Corinthian Colleges(COCO), Vimpelcom(VIP)

Other events that have market-moving potential this week include:

Mon. - None of note

Tue. - Fed’s Fisher speaks

Wed. - Fed’s Fisher speaks

Thur. - Fed’s Bernanke speaks

Fri. - pre-Labor day: Financial & Bond markets early close

There are a number of economic reports of note and a few significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - None of note

Tues. - Consumer Confidence, Minutes of Aug. 8 FOMC Meeting

Wed. - ADP Employment Change, Preliminary 2Q GDP, Preliminary 2Q GDP Price Index, Preliminary Personal Consumption, Preliminary Core PCE

Thur. - Personal Income, Personal Spending, PCE Deflator, PCE Core, Initial Jobless Claims, Help Wanted Index, Chicago Purchasing Manager, Factory Orders

Fri. - Change in Non-farm Payrolls, Unemployment Rate, Avg. Hourly Earnings, Univ. of Mich. Consumer Confidence, Construction Spending, ISM Manufacturing, ISM Prices Paid, Pending Home Sales, Total Vehicle Sales

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - BISYS Group(BSG), Cascade(CAE)

Tues. - ADC Telecom(ADCT), Dycom Industries(DY), FuelCell(FCEL), Micros Systems(MCRS), Novell(NOVL), Semtech(SMTC)

Wed. - JDS Uniphase(JDSU), Tivo Inc.(TIVO), United Natural Foods(UNFI)

Thur. - Brown-Forman(BF/A), Cheesecake Factory(CAKE), Ciena Corp.(CIEN), Del Monte(DLM), Dollar General(DG), H&R Block(HRB), HJ Heinz(HNZ), Joy Global(JOYG), Nvidia Corp.(NVDA), Omnivision Tech(OVTI), Tiffany(TIF), Wind River(DRIV), Zale Corp.(ZLC)

Fri. - Corinthian Colleges(COCO), Vimpelcom(VIP)

Other events that have market-moving potential this week include:

Mon. - None of note

Tue. - Fed’s Fisher speaks

Wed. - Fed’s Fisher speaks

Thur. - Fed’s Bernanke speaks

Fri. - pre-Labor day: Financial & Bond markets early close

BOTTOM LINE: I expect US stocks to finish the week modestly higher on short-covering, lower energy prices and mostly positive economic data. My trading indicators are still giving bullish signals and the Portfolio is 100% net long heading into the week.

Saturday, August 26, 2006

Market Week in Review

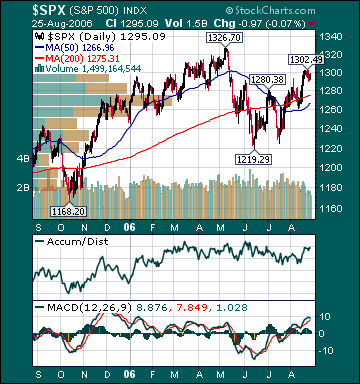

S&P 500 1,295.09 -.55%*

Click here for the Weekly Wrap by Briefing.com.

*5-day % Change

Click here for the Weekly Wrap by Briefing.com.

BOTTOM LINE: Overall, last week's market performance neutral, considering last week’s sharp gains. The advance/decline line fell, sector performance was mixed and volume was light on the week. Measures of investor anxiety were mixed. The AAII % Bulls rose to 39.35% this week from 30.53% the prior week. This reading is now at below-average levels. The AAII % Bears rose to 37.42% from 35.79% the prior week. This reading is still at above-average levels. Moreover, the 10-week moving average of the % Bears is 44.36%. It has been this high during only one other period since record-keeping began in 1987, the significant market bottom during the 1990 recession and Gulf War. It never even reached current levels during one of the greatest stock market collapses in U.S. history from 2000-2003. Many other measures of investor sentiment are still near levels normally associated with meaningful market bottoms. It is quite likely that investor sentiment towards US stocks has never been this poor in history given the positive macro backdrop.

The average 30-year mortgage rate fell 4 basis points to 6.48%, which is 32 basis points below July highs. I still believe housing is in the process of slowing to more healthy sustainable levels. Mortgage rates have likely begun an intermediate-term move lower, which should help stabilize housing over the next few months. The Case-Shiller housing futures are projecting a 5.0% decline in the average home price over the next 9 months. Considering the average house has appreciated over 50% during the last few years, this would be considered a “soft landing.”

The benchmark 10-year T-note yield fell 6 basis points on the week on weaker housing data and diminishing inflation worries. I still believe inflation concerns have peaked for the year as economic growth moderates to around average levels, unit labor costs remain subdued and the mania for commodities continues to reverse course.

The EIA reported this week that gasoline supplies rose more than expectations as refinery utilization increased. Unleaded Gasoline futures fell and are now 34.5% below September 2005 highs even as refinery utilization remains below normal as a result of the hurricanes last year, some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. According to TradeSports.com, the percent chance of a US and/or Israeli strike on Iran this year has fallen to 13.5% from 36% late last year. The elevated level of gas prices related to crude oil production disruption speculation is further dampening fuel demand, which is beginning to send gas prices back to reasonable levels.

US oil inventories are near 7-year highs. Since December 2003, global oil demand is only up .1%, while global supplies have increased 5.3%. Moreover, worldwide inventories are poised to begin increasing at an accelerated rate over the next year. I continue to believe oil is priced at extremely elevated levels on fear and record speculation by investment funds, not fundamentals. Escalating tensions with Iran and a Gulf hurricane will likely lead to a major top in oil over the next 6 weeks as demand destruction further accelerates. As the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should head meaningfully lower over the intermediate-term.

Natural gas inventories rose more than expectations this week. Supplies are now 13.5% above the 5-year average, a high level for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have plunged 54.7% since December 2005 highs. Colorado State recently reduced its forecast from five to three major hurricanes for this season versus seven last year. I expect natural gas to make new cycle lows in December or January.

Gold fell on US dollar strength and diminishing inflation fears. The US dollar rose on short-covering and weaker economic data from Europe and Asia. I continue to believe the Fed is done hiking rates for this cycle.

Energy stocks outperformed for the week on short-covering and hurricane disruption speculation. The Retail sector underperformed substantially as investors continue to price in a collapse in consumer spending. I expect Retail to outperform during the fourth quarter as these fears prove unfounded. S&P 500 profit growth for the second quarter is coming in a strong 13.2% versus a long-term historical average of 7%, according to Reuters. This would mark the 16th straight quarter of double-digit profit growth, the best streak since recording keeping began in 1936. Moreover, another double-digit gain is likely in the third quarter. Despite a 74.5% total return for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 14.9. The 20-year average p/e for the S&P 500 is 24.4. The S&P 500 is up 5.0% and the Russell 2000 Index is up 4.6% year-to-date, notwithstanding the recent correction.

The current pullback is still providing longer-term investors very attractive opportunities in many stocks that have been punished indiscriminately. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. Moreover, the most overvalued economically sensitive and emerging market stocks should continue to underperform over the intermediate-term as the manias for those shares subside. I still believe a chain reaction of events has begun that will eventually result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels. One of the characteristics of the current “negativity bubble” is that most potential positives are undermined or downplayed, while almost every potential negative is exaggerated and promptly priced in to stock prices. Problematic inflation, substantially higher long-term rates, a significant US dollar decline, a “hard-landing” in housing, a plunge in consumer spending and ever higher oil prices appear to be mostly factored into stock prices at this point. I view any one of these as unlikely and the occurrence of all as highly unlikely.

Over the coming months, an end to the Fed rate hikes, lower commodity prices, decelerating inflation readings, lower long-term rates, increased consumer confidence, rising demand for US stocks and the realization that economic growth is only slowing to around average levels should provide the catalysts for another substantial push higher in the major averages through year-end as p/e multiples begin to expand. I still believe the S&P 500 will return a total of around 15% for the year. The ECRI Weekly Leading Index was unchanged this week and is forecasting healthy, but decelerating, US economic activity.

*5-day % Change

Subscribe to:

Posts (Atom)