Style Outperformer:

Sector Outperformers:

- 1) Drugs +.69% 2) Utilities +.17% 3) Telecom +.16%

Stocks Rising on Unusual Volume:

- THRX, ACOR, GSK, S, NFP, LIFE, TMO and NFLX

Stocks With Unusual Call Option Activity:

- 1) VIAB 2) S 3) DUST 4) LIFE 5) DNR

Stocks With Most Positive News Mentions:

- 1) PG 2) UA 3) SHW 4) LIFE 5) S

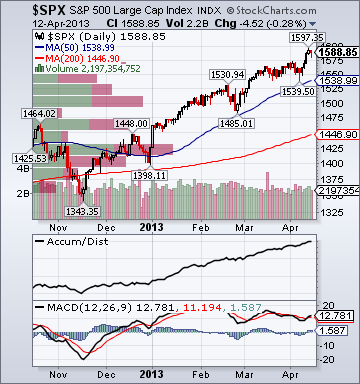

Charts:

Weekend Headlines

Bloomberg:

- EU Affirms Debt-Cut Strategy in Face of ‘Fragile’ Outlook. The European Union will tell its

counterparts in the Group of 20 nations that a shaky economic

recovery requires renewed commitment to budget cuts and other

structural reforms. “The situation remains fragile” in the euro area, the EU

said in a planning document prepared for next week’s G-20

meeting in Washington and obtained by Bloomberg News. The document affirms the EU’s “fiscal consolidation strategy” and calls on other countries to speed up similar efforts. One

of the main threats facing the world economy is “the lack of credible

medium-term fiscal consolidation plans in the U.S. and Japan,” according

to the EU document. It also sees risks stemming from a renewed slowdown

in emerging-market nations, political tensions that could boost oil

prices and the

euro-area’s three-year-old sovereign debt crisis.

- EU Set to Clash on Bank Deal as Germany Sees Treaty Limit. European

Union nations are set to

clash over plans to centralize the handling of failing banks, as Germany

warned that the bloc is running out of road to adopt crisis-fighting

measures under its current treaties. German Finance Minister

Wolfgang Schaeuble told his EU counterparts at a meeting in Dublin April

12-13 that there isn’t enough of a basis in the EU’s current rulebook

for building a common authority and fund for bank failures. Other

nations, including France, Luxembourg, and Denmark, are urging swift

progress on putting in place a resolution system, amid concerns

that treaty changes would cause unacceptable delays.

- Schaeuble Favors ‘Liability Hierarchy’ in European Bank Bailouts. German Finance Minister Wolfgang Schaeuble said he wants to see a “liability hierarchy” where

owners and creditors of banks are first in line to bail them out

before governments bolster equity and the European Stability

Mechanism provides international aid. “It is not so that all banks can in future cover their

capital requirements at the ESM,” Schaeuble told reporters in

Dublin after a two-day meeting of European Union finance

ministers and central bank governors. “Before the state gets

involved in the liability hierarchy, owners and creditors of

banks” will be asked to contribute, and the ESM will help if

“the government itself can’t because its access to financial

markets is restricted,” he said. Independently of the fact that Cyprus was a “unique case,

we will no longer accept the moral hazard problem,” Schaeuble

said. “In the future, it will have to be possible to wind down

troubled banks just like any other company, without risking the

stability of the financial sector as a whole.” To the extent necessary, a troubled bank’s home state has

to ensure the provisioning of capital, Schaeuble said.

- U.K. Faces ‘Sluggish’ Economic Growth on Weak European Demand. Britain’s economy will grow less

than previously forecast this year and further bond purchases by

the Bank of England may do little to stimulate the recovery,

according to the Ernst & Young Item Club. Gross domestic product will rise 0.6 percent, compared with

a January forecast of 0.9 percent, the London-based group said

in a report today. Growth will accelerate to 1.9 percent next

year and 2.5 percent in 2015, in line with previous estimates.

- China Said to Invite Four Flu Experts as Disease Outbreak Widens. Four international flu experts will arrive in China within days to help

authorities respond to the country’s widening bird-flu emergency,

according to two people familiar with the matter. Shanghai’s government said yesterday that the virus killed two more

people, taking the country’s death toll to 13. The city also reported

three fresh infections while the eastern provinces of Jiangsu and

Zhejiang also confirmed new cases, raising the national tally to 60 from

49 on April 13. The cases of the child in Beijing and two men in

Henan widen the geographic spread of H7N9, adding impetus to the

government’s efforts to gauge the magnitude of the infection in poultry

and wild birds.

- China’s Soybean Imports Seen Declining on Bird Flu, Dead Hogs.

An eight-year surge in soybean

imports by China, the biggest buyer, may come to an end this year as

feed consumption drops following a bird-flu outbreak and the discovery

of thousands of dead pigs floating in a river. Imports, which more than tripled from 2004 to 59.2 million

metric tons in the year to Sept. 30, will probably fall to 58

million tons this year, according to the median of a Bloomberg

survey of four crushers and three analysts in China.

- World Bank Says East Asia Should Consider Stimulus Withdrawal.

Asia’s emerging economies should consider reining in monetary stimulus

to curb the risks of asset bubbles and inflation as policy easing in

developed nations spur

capital inflows, the World Bank said. Demand-boosting measures that helped sustain growth “may

now be counterproductive,” the Washington-based lender said in

its East Asia and Pacific Economic Update released today. “As

the global economy recovers, an emerging issue is the risk of

overheating in some of the larger economies,” it said in a

release accompanying the report.

- Japan Getting Calls From U.S. to Europe Not to Drive Down Yen. Japan will be reminded of its

pledge not to drive down the yen when Group of 20 finance chiefs

meet this week for the first time since the world’s third-

largest economy intensified its campaign to defeat deflation. As G-20

finance ministers and central bankers prepare to

convene this week in Washington, the U.S. Treasury is saying it will

press Japan to refrain from competitive devaluation and European

governments are urging it not to become too reliant on

fiscal and monetary stimulus.

- BOJ’s Bet on Easing Will Backfire: Ex-Soros Adviser. The Bank of Japan (8301)’s “huge bet” by boosting quantitative easing

won’t turn the economy around and is instead sending the nation toward

default, said Takeshi Fujimaki, former adviser to billionaire investor

George Soros. “By expanding the monetary base to 270 trillion yen, the BOJ is making a

huge bet which I think it will ultimately lose,” Fujimaki said in an

interview in Tokyo on April 11. “Kuroda’s QE announcement is declaring

double suicide with the government. The BOJ will have to share the

country’s fate and default together.” Fujimaki said he recently bought put options for Japanese government

bonds of various maturities, without elaborating. “Japan’s

finance is sinking into the ocean,” Fujimaki said. “There’s no escape

from a market crash in the future when you have such enormous debt.”

“Things may look rosy for now as stocks rise, but should we see

hyper-inflation, JGBs will see a huge selloff, leading to a stock market

crash,” said Fujimaki, adding that he sold “almost all” of his Japanese

stock holdings some time ago. Kuroda’s predecessor Masaaki

Shirakawa had warned of the dangers of excess liquidity. At his final

meeting as governor he said the costs and risks of monetary policy tend

to be recognized long after steps are taken and that the government and

BOJ need to have discipline. “Shirakawa did more than

enough and he had good reasons to not do any more,” said Fujimaki.

“There will be tremendous side effects from monetary stimulus. QE

doesn’t work and has no exit.”

- N. Korea Attack Would Disrupt U.S. Companies: BGOV. A

North Korean military attack

would pose a risk to sales and investment in South Korea by U.S.

companies, including those in the automotive and semiconductor

industries, according to a Bloomberg Government study. U.S. imports of goods produced in South Korea, including

vehicles and smartphones, may also be disrupted, at least

temporarily, in the event of an attack by the totalitarian

regime led by Kim Jong Un, according to the study by Ken Monahan, a senior global business analyst with BGOV.

- Rebar Drops as China Economic Growth Signals Recovery Faltering.

Steel reinforcement-bar futures in Shanghai fell by the most in two

weeks as China’s economic growth unexpectedly eased in the first

quarter, sparking a slump in commodities. The contract for October delivery on the Shanghai Futures Exchange fell as much as 2.4 percent, the most since April 1, to 3,745 yuan ($605) a metric ton and was at 3,749 yuan at 10:49

a.m. local time.

- Rubber Slumps Most in 8 Months on Yen, Bridgestone Consumption.

Rubber slumped the most in more

than eight months as a rally in Japan’s currency cut the appeal

of the yen-based contracts and after a report that Bridgestone (5108)

Corp. may reduce consumption ignited concerns about demand from

tiremakers. The contract for delivery in September lost as much as

5.4 percent to 261.4 yen a kilogram ($2,655 a metric ton) before trading

at 264 yen on the Tokyo Commodity Exchange at 10:23 a.m.

The drop extended this year’s losses to 13 percent.

- Asian Stocks Drop as China GDP Grows Less Than Estimates.

Asian stocks dropped, with the regional benchmark index retreating from

the highest level in 20 months, after Chinese economic growth and

industrial production expanded less than economists’ estimated. Jiangxi

Copper Co., China’s largest copper producer, plunged 4.5 percent in

Hong Kong. Newcrest Mining Ltd., Australia’s biggest gold producer, sank

8.2 percent, after the bullion tumbled to the lowest price in almost

two years. Nissan Motor Co. (7201), a Japanese carmaker that gets 32

percent of sales from North America, slid 2.7 percent, pacing declines

among exporters after U.S. retail sales unexpectedly fell. The MSCI

Asia Pacific Index (MXAP) fell 0.9 percent to 136.99 as of 11:46 a.m. in

Tokyo, with about three shares falling for each

that rose.

- Fed, BOE Officials Don’t See Signs of Emerging Equity Bubbles.

Policy makers from the Federal Reserve and the Bank of England said

they see few signs of equity price bubbles in the U.S. and the U.K.,

countering criticisms record stimulus is stoking excessive risk-taking. “We

don’t have a lot of experience” with large-scale asset purchases and

“they can entail risks,” Chicago Fed President Charles Evans said during the panel discussion at the

Boston Fed.

- Global Defense Spending Falls as U.S. Cuts Outpace China Growth. Global

defense spending contracted for the first time in 15 years last year as

U.S. and European cuts exceeded rising outlays in China and Russia, the

Stockholm International Peace Research Institute said. In the

first decline since 1998, states spent $1.75 trillion on defense last

year, or 0.5 percent less in real terms than in 2011, the research group

said in a report today. The U.S. and much of Europe have curtailed

military spending as commitments in Afghanistan wind down and

governments cut budgets to reduce debt. The White House last week said

it is seeking about $615 billion in Pentagon spending for the fiscal

year starting in October, about the same as this year, before

mandatory spending cuts.

“Military spending is likely to keep falling for the next

two to three years,” Sam Perlo-Freeman, head of the research

group’s military expenditure project, said in an interview.

- Paulson Loses More Than $300 Million as Gold Declines. Billionaire John Paulson lost more

than $300 million of his personal wealth on his gold bet, as the

precious metal fell to its lowest price in almost two years. Paulson has roughly $9.5 billion invested across his hedge

funds, of which about 85 percent is invested in gold share

classes. Gold dropped 4.1 percent yesterday, shaving about $328

million from his net worth on this bet alone.

Wall Street Journal:

- As America Ages, Shortage of Help Hits Nursing Homes. A labor shortage is worsening in one of the nation's fastest-growing

occupations—taking care of the elderly and disabled—just as baby boomers

head into old age.

Nursing homes and operators of agencies

providing home-care services already are straining to find enough

so-called direct-care workers, who help the elderly or disabled with

such things as eating and bathing. They also face looming retirements in

the current workforce, in which one-fifth of workers are 55 years old

or older.

- Brokers Face Pay Disclosures. Rules Would Require Defectors to Inform Clients of Signing Bonuses, Easy Loans. Securities regulators are widely expected to start forcing

stockbrokers who get big bucks when they defect to another firm to tell

their clients. Signing bonuses, loans that are forgiven over time and other

sweeteners have become bigger as securities firms fight harder to lure

brokers.

Fox News:

- North Korea rejects South Korea's calls for talks. North Korea on Sunday rebuffed a South Korean proposal to resolve

rising tensions through dialogue, dismissing it as a "crafty trick" by

its rival. Tensions have been high on

the Korean Peninsula for weeks, with Pyongyang threatening to attack

Seoul and Washington for conducting joint military drills and for

supporting U.N. sanctions imposed on North Korea for a February nuclear

test. While the threats are largely seen as rhetoric, U.S. and South

Korean officials have said they believe North Korea may test-fire a

mid-range missile designed to reach the U.S. territory of Guam.

CNBC:

- China's Q1 GDP Growth Slows Unexpectedly to 7.7%. China's economic recovery unexpectedly stumbled in the first three

months of 2013 as the annual rate of growth eased back to 7.7 percent

from the 7.9 percent pace set in the final quarter of last year,

official data showed on Monday. The

growth rate, announced by the National Bureau of Statistics, was weaker

than a Reuters poll consensus forecast for an 8.0 percent expansion.

"This number may well explain my there was so much liquidity support in

Q1," Tim Condon, head of Asian economic research at ING in Singapore,

told Reuters. "Industrial production is unexpectedly weak and that's the

source of weakness in GDP. Based on this, the consensus GDP forecasts are going to be headed lower and we'll certainly be looking at ours."

- G20 Mulls Slashing Debt to Less Than 90% of GDP. Financial leaders of the world's 20 biggest economies will consider next

week in Washington a proposal to cut their public debt over the longer

term to well below 90 percent of gross domestic product, a document

prepared for the meeting showed.

- Moody's Zandi Is Top Pick for Fannie Watchdog. Mark Zandi, a well-known economist, is a front-runner to lead the U.S.

housing regulator and oust Edward DeMarco, who critics say hasn't done

enough to aid homeowners, the Wall Street Journal reported.

Business Insider:

Seattle Times:

- Silicon Valley’s lavish perks reportedly under IRS scrutiny. Some experts say tech companies’ free meals and other enticements ought to be taxable.

For the thousands blessed to be working for benevolent behemoths like

Google and Facebook, there could be an end to the free lunch. And the

free shuttle to work. And maybe even the free haircut. As firms pile on

benefits to attract and retain the brightest of the bright, it has

increasingly been part of the job description of Silicon Valley tech

workers that they be pampered nearly to death with perks. But now the

IRS is reportedly examining whether free food — and the other free

perks — provided by tech companies qualifies as a fringe benefit on

which employees should pay additional tax.

Wine Spectator:

-

China Cuts Back on Big-Buck Bordeaux.

A government campaign against lavish spending has led wine drinkers to

spend less. The party's over for Bordeaux first-growths. Chinese

President Xi

Jinping has told the country's free-spending political elite to cut back

on their extravagant lifestyle, leading to a sharp drop in demand for

Bordeaux’s classified growths, with the first-growths taking a

particularly hard hit under the new government’s austerity platform. "Ostentatiousness is politically frowned on in China now," said Simon

Staples from British wine merchant Berry Bros. & Rudd. There's been

a "global slowdown on those very expensive wines."

Reuters:

- Thermo Fisher nears $13 bln Life Tech deal-sources. Thermo Fisher Scientific Inc is nearing a deal to buy genetic testing equipment maker Life Technologies Corp for close to $13 billion,

according to four people familiar with the matter, in what would

be one of the year's biggest corporate takeovers. The acquisition would catapult Thermo Fisher into the hot

field of genetic sequencing, where researchers, drugmakers and

doctors are uncovering the genetic factors underpinning diseases

to better tailor treatments to the patients.

- Italy union warns subsidies for idled factory workers running out. Italy's largest union, the CGIL,

warned on Sunday that state subsidies for idled factory workers

urgently need funding or else the recession gripping the euro

zone's third-biggest economy could worsen. "Unfortunately the

economic crisis has accelerated and worsened during the first few months

of 2013," CGIL chief Susanna Camusso said in an interview on Sunday broadcast by Sky TG24 television. "We have to find those resources not only to protect the

income of those workers but also to avoid a further reduction to

consumer spending that would in turn undermine production."

- Cyprus central bank chief calls for its independence to be respected. Cyprus's central bank governor

said on Sunday he was willing to work with the government to

pull the island out of its economic crisis, provided the bank's

independence was respected. A rift between Governor Panicos Demetriades, appointed last

May by the communist former administration, and the ruling

centre-right government has deepened and pressure grown on him

to resign over his handling of the crisis.

Financial Times:

- Commodities: Tougher times for trading titans. The full scale of the trading houses’ ascent has emerged from a review

by the Financial Times of thousands of pages of documents, from bond

prospectuses to confidential investor presentations and legal filings.

The scale of their operations has long been hard to determine. Eleven of

the 20 biggest houses are either unlisted or have only recently been

required to present filings to exchanges.

- Global economy stuck in a rut.

The global economy is stuck in a rut, unable to sustain a decent

recovery and susceptible to a sudden stall, according to the latest

Brookings Institution-Financial Times tracking index of recovery.

Telegraph:

Welt am Sonntag:

- Germany's

Bundesbank wants more influence on the ECB's bank regulation arm,

citing an interview with Bundesbank Vice President Sabine

Lautenschlaeger.

Online INN:

- Is Asia Heading for a Debt Crisis? In some countries, debt is rising at a disturbing rate. According to data

from Standard & Poor’s, lending from financial institutions to the corporate

and household sector as a percentage of GDP in Hong Kong jumped from 143% in

2005 to an estimated 202 per cent in 2012. In South Korea, the same ratio surged from 132 per cent to 166 per cent over

that same time period; in Singapore, 91 per cent to 117 per cent; and in China

from 112 per cent to 130 per cent. Vietnam’s ratio nearly doubled from 66 per

cent to 113%. The culprits differ from economy to economy. In Vietnam,

state-owned enterprises are to blame. In South Korea, it’s households.

Channel News Asia:

- Singapore Sees 'Bubble-Like' Property Prices on Imbalance. National Development Minister Khaw Boon Wan said a

temporary imbalance in supply and demand has pushed up property prices

to bubble-like level and that the government is pulling out all stops to

deflate the bubble without causing it to suddenly burst.

Fars News Agency:

- Iran's OPEC Governor: Consumers, Producers Satisfied with $100 Price. Both

oil producers and consumers are satisfied with the current oil prices

between 100 to 110 dollars per barrel, Iran's Governor at the

Organization of Petroleum Exporting Countries Mohammad Ali Khatibi said.

"These days those negative factors including slowdown in oil demand

growth and worsening economic outlook in industrial countries especially

the US are prevailing in the market."

Weekend Recommendations

Barron's:

- Bullish commentary on (YHOO) and (NWY).

- Bearish commentary on (PCLN) and (FSLR).

Night Trading

- Asian indices are -1.50% to -.50% on average.

- Asia Ex-Japan Investment Grade CDS Index 115.0 +3.0 basis points.

- Asia Pacific Sovereign CDS Index 91.50 +1.0 basis point.

- NASDAQ 100 futures -.32%.

Morning Preview Links

Earnings of Note

Company/Estimate

Economic Releases

8:30 am EST

- Empire Manufacturing for April is estimated to fall to 7.0 versus 924 in March.

9:00 am EST

- Net Long-Term TIC Flows for February are estimated to rise to $40.0B versus $25.7B in January.

10:00 am EST

- The NAHB Housing Market Index for April is estimated to rise to 45.0 versus 44.0 in March.

Upcoming Splits

Other Potential Market Movers

- The Eurozone industrial production data and the RBA minutes could also impact trading today.

BOTTOM LINE: Asian indices are lower, weighed down by technology and industrial shares in the region. I expect US stocks to open modestly lower and to maintain lossses into the afternoon. The Portfolio is 50% net long heading into the week.

U.S. Week Ahead by Reuters (video).

Wall St. Week Ahead by Reuters.

Stocks to Watch Monday by MarketWatch.

Weekly Economic Calendar by Briefing.com.

BOTTOM LINE: I expect US stocks to finish the week modestly lower on rising global growth fears, Mideast unrest, Asian tensions, bird flu concerns, more Eurozone

debt angst, earnings worries, profit-taking, technical selling and more

shorting. My intermediate-term trading indicators are giving neutral

signals and the Portfolio is 50% net long heading into the week.

S&P 500 1,588.85 +2.29%*

The Weekly Wrap by Briefing.com.

*5-Day Change

Indices

- Russell 2000 942.85 +2.12%

- Value Line Geometric(broad market) 407.99 +2.29%

- Russell 1000 Growth 725.81 +2.51%

- Russell 1000 Value 809.11 +2.13%

- Morgan Stanley Consumer 993.18 +2.98%

- Morgan Stanley Cyclical 1,163.24 +2.72%

- Morgan Stanley Technology 733.41 +2.29%

- Transports 6,143.75 +1.76%

- Bloomberg European Bank/Financial Services 91.02 +2.98%

- MSCI Emerging Markets 42.22 +1.20%

- Lyxor L/S Equity Long Bias 1,138.01 -.27%

- Lyxor L/S Equity Variable Bias 842.12 -.55%

Sentiment/Internals

- NYSE Cumulative A/D Line 181,630 +1.77%

- Bloomberg New Highs-Lows Index 871.0 +977

- Bloomberg Crude Oil % Bulls 38.9 +26.4%

- CFTC Oil Net Speculative Position 223,398 -10.2%

- CFTC Oil Total Open Interest 1,768,185 +2.1%

- Total Put/Call 1.14 +9.62%

- OEX Put/Call 2.82 +90.54%

- ISE Sentiment 56.0 -28.21%

- Volatility(VIX) 12.06 -13.36%

- S&P 500 Implied Correlation 51.59 -7.02%

- G7 Currency Volatility (VXY) 9.24 +.65%

- Smart Money Flow Index 11,729.18 +3.52%

- Money Mkt Mutual Fund Assets $2.623 Trillion -.3%

- AAII % Bulls 19.3 -45.6%

Futures Spot Prices

- Reformulated Gasoline 280.18 -2.48%

- Heating Oil 287.18 -1.85%

- Bloomberg Base Metals Index 197.83 +.87%

- US No. 1 Heavy Melt Scrap Steel 368.0 USD/Ton unch.

- China Iron Ore Spot 141.0 USD/Ton +3.75%

- UBS-Bloomberg Agriculture 1,499.98 +1.5%

Economy

- ECRI Weekly Leading Economic Index Growth Rate 6.2% unch.

- Philly Fed ADS Real-Time Business Conditions Index -.3283 +1.38%

- S&P 500 Blended Forward 12 Months Mean EPS Estimate 115.13 +.22%

- Citi US Economic Surprise Index 7.8 +3.8 points

- Citi Emerging Mkts Economic Surprise Index -37.7 -8.4 points

- Fed Fund Futures imply 52.0% chance of no change, 48.0% chance of 25 basis point cut on 5/1

- US Dollar Index 82.31 -.32%

- Euro/Yen Carry Return Index 134.41 +1.71%

- Yield Curve 149.0 +1 basis point

- 10-Year US Treasury Yield 1.72% +1 basis point

- Federal Reserve's Balance Sheet $3.210 Trillion +.39%

- U.S. Sovereign Debt Credit Default Swap 32.50 -5.39%

- Illinois Municipal Debt Credit Default Swap 124.0 -8.29%

- Western Europe Sovereign Debt Credit Default Swap Index 97.26 -3.83%

- Emerging Markets Sovereign Debt CDS Index 186.95 -6.83%

- Israel Sovereign Debt Credit Default Swap 116.61 -3.15%

- South Korea Sovereign Debt Credit Default Swap 82.0 -6.45%

- China Blended Corporate Spread Index 402.0 -6 basis points

- 10-Year TIPS Spread 2.44% -3 basis points

- 2-Year Swap Spread 14.50 -.5 basis point

- 3-Month EUR/USD Cross-Currency Basis Swap -17.75 -.25 basis point

- N. America Investment Grade Credit Default Swap Index 82.85 -5.95%

- European Financial Sector Credit Default Swap Index 167.55 -4.50%

- Emerging Markets Credit Default Swap Index 222.89 -11.80%

- CMBS AAA Super Senior 10-Year Treasury Spread to Swaps 110.50 -5.5 basis points

- M1 Money Supply $2.511 Trillion +2.16%

- Commercial Paper Outstanding 1,021.70 +1.90%

- 4-Week Moving Average of Jobless Claims 358,000 +3,700

- Continuing Claims Unemployment Rate 2.4% unch.

- Average 30-Year Mortgage Rate 3.43% -11 basis points

- Weekly Mortgage Applications 826.10 +4.48%

- Bloomberg Consumer Comfort -34.0 +.1 point

- Weekly Retail Sales +2.90% -10 basis points

- Nationwide Gas $3.56/gallon -.06/gallon

- Baltic Dry Index 875.0 +1.63%

- China (Export) Containerized Freight Index n/a

- Oil Tanker Rate(Arabian Gulf to U.S. Gulf Coast) 17.50 unch.

- Rail Freight Carloads 231,648 -.83%

Best Performing Style

Worst Performing Style

Leading Sectors

Lagging Sectors

Weekly High-Volume Stock Gainers (9)

- FSLR, LUFK, TSRO, SPWR, NUS, PICO, FSCI, NGVC and FBC

Weekly High-Volume Stock Losers (10)

- IGTE, INFI, TTEK, BRLI, MG, HMA, FTNT, FFIV, SHLM and TITN

Weekly Charts

ETFs

Stocks

*5-Day Change

Today's Market Take:

Broad Market Tone:

- Advance/Decline Line: Lower

- Sector Performance: Most Sectors Declining

- Market Leading Stocks: Performing In Line

Equity Investor Angst:

- ISE Sentiment Index 54.0 -50.0%

- Total Put/Call 1.12 +28.74%

Credit Investor Angst:

- North American Investment Grade CDS Index 81.90 +.32%

- European Financial Sector CDS Index 167.55 +5.4%

- Western Europe Sovereign Debt CDS Index 97.26 +1.5%

- Emerging Market CDS Index 223.32 -.78%

- 2-Year Swap Spread 14.50 +.5 bp

- 3-Month EUR/USD Cross-Currency Basis Swap -17.75 -.5 bp

Economic Gauges:

- 3-Month T-Bill Yield .06% unch.

- Yield Curve 149.0 -7 basis points

- China Import Iron Ore Spot $141.0/Metric Tonne +.07%

- Citi US Economic Surprise Index 7.80 -1.2 points

- 10-Year TIPS Spread 2.44 -3 bps

Overseas Futures:

- Nikkei Futures: Indicating -45 open in Japan

- DAX Futures: Indicating +42 open in Germany

Portfolio:

- Slightly Higher: On gains in my biotech sector longs and emerging markets shorts

- Disclosed Trades: None

- Market Exposure: 50% Net Long