Click here for the Weekly Wrap by Briefing.com.

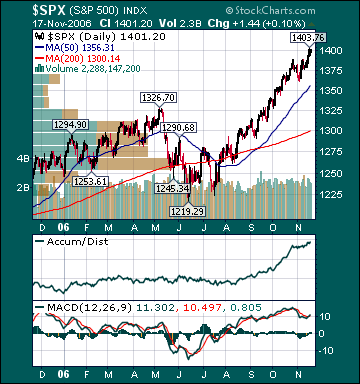

BOTTOM LINE: Overall, last week's market performance was bullish as the Dow Jones Industrial Average hit another all-time high. The advance/decline line rose, most sectors gained and volume was slightly above average on the week. Measures of investor anxiety were mixed. The AAII percentage of bulls fell to 46.56% this week from 50.60% the prior week. This reading is now only slightly above average levels. The AAII percentage of bears rose to 30.53% this week from 26.51% the prior week. This reading is now slightly above average levels. The 10-week moving average of the percentage of bears is currently 34.4%, an above-average level. The 10-week moving-average of the percentage of bears was 43.0% at the major bear market lows during 2002. Moreover, the 50-week moving-average of the percentage of bears is 35.26%, a very high level seen during only two other periods in U.S. history.

I continue to believe steadfastly high bearish sentiment in many quarters is mind-boggling considering the S&P 500's 15.4% rise in just over five months, one of the best August/September/October runs in U.S. history and the fact that the DJIA is at an all-time high. The bears still remain stunningly complacent, in my opinion, notwithstanding recent gains. Every pullback is seen as a major top and every move higher is just another shorting/selling opportunity.

As well, there are many other indicators registering high levels of investor skepticism regarding recent stock market gains. The NYSE Arms reading has been at above-average levels frequently of late. The 50-day moving-average of the ISE Sentiment Index is just off all-time lows and still well below average levels. Nasdaq and NYSE short interest made record highs again recently. Moreover, public short interest continues to soar to record highs and U.S. stock mutual funds have seen outflows for months, according to AMG Data Services. Finally, investment blogger sentiment is still very bearish with bulls recently making a new low. In my opinion, the market's exceptional performance through the seasonally weak months and significant political uncertainty illustrates its underlying strength. There is still a high wall of worry for stocks to climb substantially from current levels as the public remains very skeptical of recent gains.

I continue to believe this is a direct result of the strong belief by the herd that the major U.S. averages are in a long-term trading range or secular bear. There is overwhelming evidence that investment sentiment by the general public regarding U.S. stocks has never been this poor in history, with the DJIA registering all-time highs almost daily. I still expect the herd to finally embrace the current bull market next year, which should result in another meaningful move higher in the major averages as the S&P 500 breaks out to an all-time high to join the DJIA and Russell 2000. I continue to believe the coming bullish shift in long-term sentiment, with respect to U.S. stocks, will result in the "mother of all short-covering rallies."

The average 30-year mortgage rate fell 9 basis points to 6.24%, which is 56 basis points below July highs. I still believe housing is in the process of stabilizing at relatively high levels. Former Fed Chairman Alan Greenspan and several current Fed members reiterated there belief recently that the “worst may well be over” for the housing slowdown. Mortgage applications have begun trending higher with the decline in mortgage rates. As well, Housing inventories have been falling. The Case-Shiller housing futures have improved recently and are now projecting a 4.8% decline in the average home price over the next 7 months. Considering the median house has appreciated over 50% during the last few years with record high US home ownership, this would be considered a “soft landing.” The overall negative effects of housing on the US economy are still being exaggerated by the bears, in my opinion. Housing and home equity extractions have been slowing substantially for well over a year and have been mostly offset by many other very positive aspects of the economy.

Americans’ median net worth is still very close to or at record high levels, energy prices have plunged, consumer spending remains healthy, unemployment is low by historic standards, interest rates are low, stocks are surging and wages are rising, just to name a few. The unemployment rate fell to a historically low 4.4% last month from 4.6% the prior month and 5.1% in September 2005, notwithstanding fewer real estate-related jobs. Consumer spending is still above long-term average levels and looks poised to strengthen into the holiday shopping season.

The Consumer Price Index for October rose 1.3% year-over-year, the smallest increase since June 2002 and down from 4.7% in September of 2005. This is substantially below the long-term average of around 3%. Moreover, the CPI has only been lower during 2 other periods since the mid-1960s. It was lower during late 1986 and early 2002-mid 2002. Many other measures of inflation have recently shown substantial deceleration. The Producer Price Index for October matched the largest decline in US history, falling 1.6% year-over-year. Most measures of Americans’ income growth are now around four times the rate of inflation.

The benchmark 10-year T-note yield was unchanged on the week as a substantial decline in inflation offset better economic data. In my opinion, investors’ continuing fears over an economic “hard landing” are misplaced. The economy has created almost half a million jobs in the last three months. Consumer spending is very important to the health of the US economy. Weekly retail sales rose an above-average 3.4% for the week. Spending is poised to remain strong on plunging energy prices, low long-term interest rates, a rising stock market, healthy job market, decelerating inflation and more optimism. The CRB Commodities Index, the main source of inflation fears, has now declined 2.2% over the last 12 months and is down 16.3% from May highs despite a historic flood of capital into commodity funds and numerous potential upside catalysts. The average commodity hedge fund is down about 14.0% for the year. Oil has declined $20/bbl from July highs. I continue to believe inflation fears have peaked for this cycle as global economic growth stabilizes around average levels, unit labor costs remain subdued and the mania for commodities continues to reverse course.

The EIA reported this week that gasoline supplies fell more than expectations as refinery utilization declined. U.S. gasoline supplies are still at extraordinarily high levels for this time of the year. Unleaded Gasoline futures fell for the week and have plunged 47.2% from September 2005 highs even as some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. Gasoline demand is estimated to rise .8% this year versus a 20-year average of 1.7% demand growth. Moreover, distillate stocks are 11.6% above the five-year average for this time of the year. The still elevated level of gas prices, related to crude oil production disruption speculation by investment funds, will further dampen global fuel demand, sending gas prices still lower over the intermediate-term.

US oil inventories are near 7-year highs. Since December 2003, global oil demand is only up 1.5%, despite booming global growth, while global supplies have increased 5.9%, according to the Energy Intelligence Group. Moreover, worldwide oil inventories are poised to begin increasing at an accelerated rate over the next year. I continue to believe oil is priced at extremely elevated levels on fear and record speculation by investment funds, not fundamentals. The Amaranth Advisors hedge fund blow-up is a prime example of the extent to which many investment funds have been speculating on ever higher energy prices through futures contracts, thus driving the price of the underlying commodity to absurd levels. Amaranth, a multi-strategy hedge fund, lost about $6.5 billion of its $9.5 billion under management in less than two months speculating mostly on higher natural gas prices. I suspect a number of other funds will experience similar fates over the coming months, which will further pressure energy prices as these funds unwind their leveraged long positions to meet investor redemptions.

Oil has clearly broken its uptrend, hitting a 17-month low this week. The commodity continues to trade very poorly despite numerous potential catalysts. Recently, Cambridge Energy Research, one of the most respected energy research firms in the world, put out a report that drills gaping holes in the belief by most investors of imminent "peak oil" production. Cambride said that its analysis indicates that the remaining global oil base is actually 3.74 trillion barrels, three times greater than "peak oil" theory proponents say and that the "peak oil" theory is based on faulty analysis. I suspect the contango that currently exists in energy futures, which encourages hoarding, will begin to reverse over the coming months as more investors come to the realization that the "peak oil" theory is hugely flawed, global storage fills, and Chinese demand slows.

A major top in oil is likely already in place as global crude oil storage capacity utilization is running around 97%. Recent OPEC production cuts will likely result in a complete technical breakdown in crude over the coming weeks. Demand destruction is already pervasive globally. Moreover, many Americans feel as though they are helping fund terrorism or hurting the environment every time they fill up their gas tanks. I do not believe we will ever again see the demand for gas-guzzling vehicles that we saw in recent years, even if gas prices continue to plunge. OPEC production cuts, with oil still at very high levels and weakening global growth, only further deepens resentment towards the cartel and will result in even greater long-term demand destruction. Finally, as the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should continue heading meaningfully lower over the intermediate-term, notwithstanding OPEC production cuts. I still believe oil will test $50/bbl. before year-end. I suspect oil will eventually fall to levels that most investors deemed unimaginable just a few months ago during the next significant global economic downturn.

Natural gas inventories rose slightly less than expectations this week. Prices for the commodity rose again as investment fund speculation remains near record highs despite the fact that supplies are now 7.4% above the 5-year average and at all-time high levels for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have collapsed 48.1% since December 2005 highs.

Gold fell slightly on the week on declining inflation, a stronger US dollar and less investment fund speculation. The US dollar rose on short-covering and better economic data. I continue to believe there is very little chance of another Fed rate hike anytime soon. An eventual cut is more likely next year as inflation continues to decelerate substantially.

Airline stocks outperformed for the week on falling oil prices and merger speculation. Commodity stocks underperformed substantially on a firmer US dollar, rising supplies and decelerating demand. S&P 500 profit growth for the third quarter came in around 20% versus a long-term historical average of 7%, according to Thomson Financial. This marks the 17th straight quarter of double-digit profit growth, the best streak since recording keeping began in 1936. Moreover, another double-digit gain is likely in the fourth quarter. Just a few months ago many investors expected profit growth to fall to the low single digits this year. Despite an 88.6% total return(which is equivalent to a 16.6% average annual return) for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 15.9. The 20-year average p/e for the S&P 500 is 24.4. The S&P 500 is now up 14.1% and the Russell 2000 Index is up 18.3% year-to-date. Historically, if the S&P 500 is up at least 10% going into the final two months of the year, which it was, it continues to climb the last two months 84% of the time.

Current stock prices are still providing longer-term investors very attractive opportunities, in my opinion. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. A recent CSFB report confirmed this view. The report concluded that on a price-to-cash flow basis growth stocks are now cheaper than value stocks for the first time since at least 1977. The entire decline in the S&P 500’s p/e, since the bubble burst in 2000, is attributable to growth stock multiple contraction. I still expect the most overvalued economically sensitive and emerging market stocks to continue underperforming over the intermediate-term as the manias for those shares subside and global growth slows to more average rates. I continue to believe a chain reaction of events has begun that will result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels, notwithstanding recent gains. One of the characteristics of the current “negativity bubble” is that most potential positives are undermined, downplayed or completely ignored, while almost every potential negative is exaggerated, trumpeted and promptly priced in to stock prices. Furthermore, this “irrational pessimism” by investors has resulted in a dramatic decrease in the supply of stock as companies bought back shares, IPOs were pulled and secondary stock offerings canceled. Commodity funds, which have received huge capital infusions this year, will likely see significant outflows at year-end. Some of this capital will likely find its way back to US stocks. I continue to believe there is massive bull firepower available on the sidelines for US equities at a time when the supply of stock has contracted.

An end to the Fed rate hikes, lower commodity prices, seasonal strength, an end to political uncertainty, decelerating inflation readings, a strong holiday shopping season, lower long-term rates, increased consumer/investor confidence, short-covering, investment manager performance anxiety, rising demand for US stocks and the realization that economic growth is only slowing to around average levels should provide the catalysts for another substantial push higher in the major averages through year-end as p/e multiples expand further. I still expect the S&P 500 to return a total of at least 15% for the year. The ECRI Weekly Leading Index rose again this week, very close to cycle highs, and is forecasting a modest acceleration in US economic activity.

*5-day % Change

No comments:

Post a Comment