Market Snapshot

Detailed Market Summary

Market Internals

Economic Commentary

Movers & Shakers

Today in IBD

NYSE OrderTrac

I-Watch Sector Overview

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Option Dragon

Real-time Intraday Chart/Quote

Monday, September 18, 2006

Sunday, September 17, 2006

Monday Watch

Weekend Headlines

Bloomberg:

- Pope Benefict XVI apologized today for offence caused by comments he made in a university lecture this week implicitly linking Islam to violence.

- Henry Paulson, who left Goldman Sachs(GS) in May to become the US Treasury Secretary, said he was surprised to learn the extent to which Iranian front companies had infiltrated the financial system, prompting him to organize an “education” program for banks and governments.

- General Motors(GM), trying to improve its image among environmentalists and consumers looking for better mileage, will build more than 100 hydrogen-fuel vehicles next year.

- National Intelligence Director Negroponte suggested interrogations of suspected terrorists have been curtailed because of legal concerns raised by a US Supreme Court ruling on the treatment of enemy combatants.

- When some of the world’s smartest investors earlier this year said buying sugar was the easiest way to make money in 2006, they would have been better off buying stocks in Jordan where the Amman SE General Index is down 23%. Sugar fell 34% from March 31 to the end of August.

- “The cyclical story in commodities is behind us,” said Jack Ablin, CIO at Harris Private Bank in Chicago, which manages $50 billion and sold its investment in commodities. The CRB Index just had its worst 3-week loss in almost 26 years.

Wall Street Journal:

- Symbol Technologies(SBL) is close to completing an auction of itself, which could result in the sale of the $3.2 billion wireless-equipment company in a matter of days.

- Steven Cohen, who runs the $10 billion hedge-fund firm SAC Capital Advisors LLC, holds stocks longer now and makes bigger bets when he does purchase them.

NY Times:

- Many US farmers have decided to profit from demand for ethanol by planting corn instead of wheat.

- At least nine US states have passed laws extending the age limits for health-insurance coverage parents can provide for their children.

Washington Post:

- The head of FEMA, under the US Dept. of Homeland Security, will get direct access to the president during a crisis and an increased budget as part of an agreement being negotiated by congressional lawmakers.

San Francisco Chronicle:

- Google Inc.(GOOG) executive Chris Sacca complained about the slow pace of negotiating a final agreement to provide free wireless Internet access in San Francisco.

Fortune.com:

- Frank Quattrone is reputed to be developing a new, $5 billion venture and stands to collect $120 million in back pay from CSFB.

AP:

- Saudi Arabia’s religious police, known as the Muttawa, issued a decree restricting the sale of cats and dogs as pets, regarded as a sign of Western influence. The mandate, which doesn’t state whether current pets would be confiscated, hasn’t been enforced yet.

Middle East Economic Digest:

- Royal Dutch Shell’s Oman venture expects bids this month for a contract to boost output from the Qarn Alam oil field, after it re-tendered the project when initial bids came in over budget.

Yonhap:

- A niece of North Korean leader Kim Jong Il committed suicide in Paris because she did not want to return to the communist state, citing North Korean officials.

Yomiuri:

- Japan asked China to cut its steel output capacity earlier this month on concern an oversupply of products will result in a sharp price decline.

Weekend Recommendations

Barron's:

- Made positive comments on (EMR), (CLF) and (IVGN).

- Made negative comments on (OVTI).

Citigroup:

- Reiterated Buy on (SNDK), target $69.

Night Trading

Asian indices are +.25% to +1.0% on average.

S&P 500 indicated +.05%

NASDAQ 100 indicated +.08%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- None of note

Upcoming Splits

- None of note

Economic Releases

8:30 am EST

- The 2Q Current Account Deficit is estimated to widen to -$214.0 billion versus -$208.7 billion in 1Q.

9:00 am EST

- Net Foreign Security Purchases for July are estimated to come in at $70.0 billion versus $75.1 billion in June.

1:00 pm EST

- NAHB Housing Market Index for September fell to 31 versus a reading of 32 in August.

Bloomberg:

- Pope Benefict XVI apologized today for offence caused by comments he made in a university lecture this week implicitly linking Islam to violence.

- Henry Paulson, who left Goldman Sachs(GS) in May to become the US Treasury Secretary, said he was surprised to learn the extent to which Iranian front companies had infiltrated the financial system, prompting him to organize an “education” program for banks and governments.

- General Motors(GM), trying to improve its image among environmentalists and consumers looking for better mileage, will build more than 100 hydrogen-fuel vehicles next year.

- National Intelligence Director Negroponte suggested interrogations of suspected terrorists have been curtailed because of legal concerns raised by a US Supreme Court ruling on the treatment of enemy combatants.

- When some of the world’s smartest investors earlier this year said buying sugar was the easiest way to make money in 2006, they would have been better off buying stocks in Jordan where the Amman SE General Index is down 23%. Sugar fell 34% from March 31 to the end of August.

- “The cyclical story in commodities is behind us,” said Jack Ablin, CIO at Harris Private Bank in Chicago, which manages $50 billion and sold its investment in commodities. The CRB Index just had its worst 3-week loss in almost 26 years.

Wall Street Journal:

- Symbol Technologies(SBL) is close to completing an auction of itself, which could result in the sale of the $3.2 billion wireless-equipment company in a matter of days.

- Steven Cohen, who runs the $10 billion hedge-fund firm SAC Capital Advisors LLC, holds stocks longer now and makes bigger bets when he does purchase them.

NY Times:

- Many US farmers have decided to profit from demand for ethanol by planting corn instead of wheat.

- At least nine US states have passed laws extending the age limits for health-insurance coverage parents can provide for their children.

Washington Post:

- The head of FEMA, under the US Dept. of Homeland Security, will get direct access to the president during a crisis and an increased budget as part of an agreement being negotiated by congressional lawmakers.

San Francisco Chronicle:

- Google Inc.(GOOG) executive Chris Sacca complained about the slow pace of negotiating a final agreement to provide free wireless Internet access in San Francisco.

Fortune.com:

- Frank Quattrone is reputed to be developing a new, $5 billion venture and stands to collect $120 million in back pay from CSFB.

AP:

- Saudi Arabia’s religious police, known as the Muttawa, issued a decree restricting the sale of cats and dogs as pets, regarded as a sign of Western influence. The mandate, which doesn’t state whether current pets would be confiscated, hasn’t been enforced yet.

Middle East Economic Digest:

- Royal Dutch Shell’s Oman venture expects bids this month for a contract to boost output from the Qarn Alam oil field, after it re-tendered the project when initial bids came in over budget.

Yonhap:

- A niece of North Korean leader Kim Jong Il committed suicide in Paris because she did not want to return to the communist state, citing North Korean officials.

Yomiuri:

- Japan asked China to cut its steel output capacity earlier this month on concern an oversupply of products will result in a sharp price decline.

Weekend Recommendations

Barron's:

- Made positive comments on (EMR), (CLF) and (IVGN).

- Made negative comments on (OVTI).

Citigroup:

- Reiterated Buy on (SNDK), target $69.

Night Trading

Asian indices are +.25% to +1.0% on average.

S&P 500 indicated +.05%

NASDAQ 100 indicated +.08%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- None of note

Upcoming Splits

- None of note

Economic Releases

8:30 am EST

- The 2Q Current Account Deficit is estimated to widen to -$214.0 billion versus -$208.7 billion in 1Q.

9:00 am EST

- Net Foreign Security Purchases for July are estimated to come in at $70.0 billion versus $75.1 billion in June.

1:00 pm EST

- NAHB Housing Market Index for September fell to 31 versus a reading of 32 in August.

BOTTOM LINE: Asian Indices are higher, boosted by technology shares in the region. I expect US stocks to open modestly higher and to maintain gains into the afternoon. The Portfolio is 100% net long heading into the week.

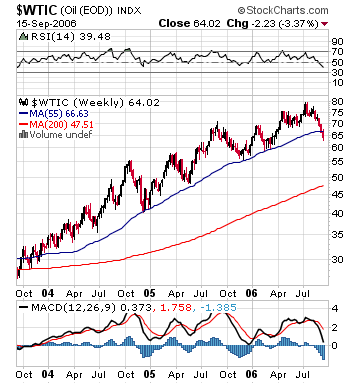

Chart of Interest(Crude Oil)

BOTTOM LINE: Oil broke clearly below its long-term uptrend line at $66.33/bbl. last week. Crude is still in its seasonally strongest period of the year. Historically, mid-October brings seasonal price weakness through February. I expect oil to fall to the low 50s before year-end.

Weekly Outlook

Click here for The Week Ahead by Reuters

There are a few of economic reports of note and several significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - 2Q Current Account Balance, Net Foreign Security Purchases, NAHB Housing Market Index

Tues. - Producer Price Index, Housing Starts, Building Permits

Wed. - FOMC Rate Decision

Thur. - Initial Jobless Claims, Leading Indicators, Philly Fed

Fri. - None of note

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - None of note

Tues. - Autozone(AZO), CBRL Group(CBRL), Chaparral Steel(CHAP), Darden Restaurants(DRI), Factset Research(FDS), Oracle Corp.(ORCL)

Wed. - Carmax(KMX), Cintas Corp.(CTAS), Circuit City(CC), Herman Miller(MLHR), Morgan Stanley(MS), Stage Stores(SSI), Steelcase(SCS)

Thur. - AG Edwards(AGE), Bed Bath & Beyond(BBBY), Biomet(BMET), Carnival Corp.(CCL), ConAgra Corp.(CAG), FedEx Corp.(FDX), Finish Line(FINL), General Mills(GIS), Nike Inc.(NKE), Palm Inc.(PALM), Scholastic Corp.(SCHL)

Fri. - KB Home(KBH)

Other events that have market-moving potential this week include:

Mon. - Bank of America Investment Conference, TGT Mid-month Sales Update

Tue. - CSFB Chemical Conference, UBS Global Paper and Forest Products Conference, Bank of America Investment Conference

Wed. - CSFB Chemical Conference, UBS Global Paper and Forest Products Conference, Bank of America Investment Conference, Goldman Sachs Communacopia Conference

Thur. - Oppenheimer Diabetes Conference, Bank of America Investment Conference

Fri. - None of note

There are a few of economic reports of note and several significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - 2Q Current Account Balance, Net Foreign Security Purchases, NAHB Housing Market Index

Tues. - Producer Price Index, Housing Starts, Building Permits

Wed. - FOMC Rate Decision

Thur. - Initial Jobless Claims, Leading Indicators, Philly Fed

Fri. - None of note

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - None of note

Tues. - Autozone(AZO), CBRL Group(CBRL), Chaparral Steel(CHAP), Darden Restaurants(DRI), Factset Research(FDS), Oracle Corp.(ORCL)

Wed. - Carmax(KMX), Cintas Corp.(CTAS), Circuit City(CC), Herman Miller(MLHR), Morgan Stanley(MS), Stage Stores(SSI), Steelcase(SCS)

Thur. - AG Edwards(AGE), Bed Bath & Beyond(BBBY), Biomet(BMET), Carnival Corp.(CCL), ConAgra Corp.(CAG), FedEx Corp.(FDX), Finish Line(FINL), General Mills(GIS), Nike Inc.(NKE), Palm Inc.(PALM), Scholastic Corp.(SCHL)

Fri. - KB Home(KBH)

Other events that have market-moving potential this week include:

Mon. - Bank of America Investment Conference, TGT Mid-month Sales Update

Tue. - CSFB Chemical Conference, UBS Global Paper and Forest Products Conference, Bank of America Investment Conference

Wed. - CSFB Chemical Conference, UBS Global Paper and Forest Products Conference, Bank of America Investment Conference, Goldman Sachs Communacopia Conference

Thur. - Oppenheimer Diabetes Conference, Bank of America Investment Conference

Fri. - None of note

BOTTOM LINE: I expect US stocks to finish the week modestly higher on short-covering, bargain hunting, decelerating inflation readings, no Fed rate hike, less hawkish Fed policy comments, mostly positive earnings reports and less pessimism. My trading indicators are still giving bullish signals and the Portfolio is 100% net long heading into the week.

Saturday, September 16, 2006

Market Week in Review

S&P 500 1,319.87 +1.61%*

Click here for the Weekly Wrap by Briefing.com.

*5-day % Change

Click here for the Weekly Wrap by Briefing.com.

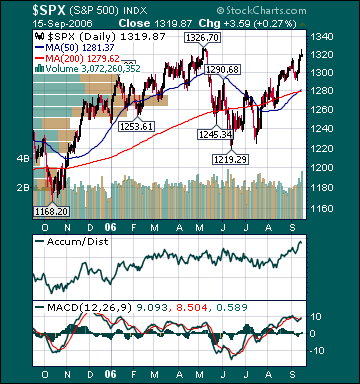

BOTTOM LINE: Overall, last week's market performance was very bullish. The advance/decline line rose, most sectors gained and volume was above average on the week. Measures of investor anxiety were mixed. The AAII percentage of Bulls rose to 47.95% this week from 42.99% the prior week. This reading is now slightly above average levels. The AAII percentage of Bears rose to 38.36% this week from 29.91% the prior week. This reading is now again above average levels. The 10-week moving average of the percent Bears is currently 40.04%. The 10-week moving-average of percent Bears was 43.0% at the major bear market lows during 2002. The only other times it was higher than these levels, since record keeping began in 1987, were the significant market bottom during the 1990 recession/Gulf War and in October 1992. In my opinion, the fact that bullish sentiment is moving up from excessively depressed levels is a positive. The steadfastly high bearish percentage, given recent gains, is still providing a wall of worry for stocks to climb higher. I continue to believe the “irrational pessimism” aimed towards most US stocks has never been this great in history given the positive macro backdrop.

The average 30-year mortgage rate fell another 4 basis points to 6.43%, which is 37 basis points below July highs. I still believe housing is in the process of slowing to more healthy sustainable levels. Mortgage rates have likely begun an intermediate-term move lower, which should help stabilize housing over the next few months. The Case-Shiller housing futures are still projecting a 5% decline in the average home price over the next 9 months. Considering the average house has appreciated over 50% during the last few years, this would be considered a “soft landing.” The overall negative effects of housing on the US economy are currently being exaggerated, in my opinion. Housing has been slowing substantially for 13 months and has been mostly offset by other very positive aspects of the economy.

The benchmark 10-year T-note yield rose 2 basis points on the week on profit-taking and more economic optimism. The CRB Commodities Index, the main source of inflation fears, has now declined 4% over the last 12 months and is down 16.0% from May highs, approaching bear market territory. I believe inflation concerns have peaked for the year as economic growth moderates to around average levels, unit labor costs remain subdued and the mania for commodities continues to reverse course.

The EIA reported this week that gasoline supplies rose less than expectations as refinery utilization fell. Unleaded Gasoline futures dropped substantially again and are now 45.9% below September 2005 highs even as refinery utilization remains below normal as a result of the hurricanes last year, some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. Gasoline demand is estimated to rise .8% this year versus a 20-year average of 1.7% demand growth. According to TradeSports.com, the percent chance of a US and/or Israeli strike on Iran this year has fallen to 10% from 36% late last year. The elevated level of gas prices related to crude oil production disruption speculation is further dampening fuel demand, which is sending gas prices back to more reasonable levels.

US oil inventories have only been higher during one other period over the last 7 years. Since December 2003, global oil demand is only up .1%, while global supplies have increased 5.3%, according to the Energy Intelligence Group. Moreover, worldwide inventories are poised to begin increasing at an accelerated rate over the next year. I continue to believe oil is priced at extremely elevated levels on fear and record speculation by investment funds, not fundamentals. Oil closed the week at $63.33/bbl., breaking clearly below its major uptrend line at $66.33 despite the fact that we are in a seasonally strong period for the commodity. A major top in oil is likely already in place. However, a Gulf hurricane will likely lead to a bounce higher in price over the next month further accelerating demand destruction, resulting in a complete technical breakdown in crude. As the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should head meaningfully lower from current levels over the intermediate-term.

Natural gas inventories rose more than expectations this week, sending prices for the commodity plunging further. Supplies are now 12.4% above the 5-year average, a record high level for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have collapsed 68.2% since December 2005 highs. It is very likely US natural gas storage will become full during October, creating the distinct possibility of a “no-bid” situation for the physical commodity. Colorado State recently reduced its forecast from three to two major hurricanes for this season versus seven last year. The peak of hurricane season was September 10. Natural gas made new cycle lows again this week despite the fact that the commodity is in its seasonally strong period.

Gold fell on the week as the US dollar strengthened and inflation fears continued to diminish. The US dollar rose on more US economic optimism, lower commodity prices and weaker international economic reports. I continue to believe there is almost zero chance of a Fed rate hike at the September 20 meeting and very little chance of another hike this year.

Investment Banking stocks outperformed for the week on more US stock market optimism and strong earnings reports. Commodity stocks underperformed substantially again as the mania for these shares continues to subside in the face of falling prices and declining inflation worries. S&P 500 profit growth for the second quarter came in a strong 16.3% versus a long-term historical average of 7%, according to Thomson Financial. This is the 16th straight quarter of double-digit profit growth, the best streak since recording keeping began in 1936. Moreover, another double-digit gain is likely in the third quarter. Despite a 77.1% total return for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 15.1. The 20-year average p/e for the S&P 500 is 24.4. The S&P 500 is now up 7.2% and the Russell 2000 Index is up 9.2% year-to-date. The DJIA is only 190 points away from its all-time high reached on January 14, 2000. I expect the Dow to breach this level convincingly during the fourth quarter.

Current stock prices are still providing longer-term investors very attractive opportunities in many equities that have been punished indiscriminately. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. A recent CSFB report confirmed this view. The report concluded that on a price-to-cash flow basis growth stocks are now cheaper than value stocks for the first time since at least 1977. Almost the entire decline in the S&P 500’s p/e, since the bubble burst in 2000, is a function of growth stock multiple contraction. The p/e on value stocks is back near high levels. I still expect the most overvalued economically sensitive and emerging market stocks to continue underperforming over the intermediate-term as the manias for those shares subside and global growth slows to more average rates. I believe a chain reaction of events has begun that will result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels. One of the characteristics of the current “negativity bubble” is that most potential positives are undermined, downplayed or completely ignored, while almost every potential negative is exaggerated and promptly priced in to stock prices. This “irrational pessimism” by investors is resulting in a dramatic decrease in the supply of stock as companies buy back shares, IPOs are pulled and secondary stock offerings are canceled.

Over the coming months, an end to the Fed rate hikes, lower commodity prices, seasonal strength, the November election, decelerating inflation readings, lower long-term rates, increased consumer/investor confidence, rising demand for US stocks and the realization that economic growth is only slowing to around average levels should provide the catalysts for another substantial push higher in the major averages through year-end as p/e multiples begin to expand. I expect the S&P 500 to return a total of at least 15% for the year. The ECRI Weekly Leading Index rose again this week and is forecasting healthy US economic activity.

*5-day % Change

Friday, September 15, 2006

Weekly Scoreboard*

Indices

S&P 500 1,319.87 +1.61%

DJIA 11,560.77 +1.48%

NASDAQ 2,235.99 +3.22%

Russell 2000 729.35 +2.94%

Wilshire 5000 13,193.31 +1.66%

S&P Barra Growth 614.22 +1.87%

S&P Barra Value 703.37 +1.36%

Morgan Stanley Consumer 650.81 +1.10%

Morgan Stanley Cyclical 815.78 +1.07%

Morgan Stanley Technology 521.98 +3.84%

Transports 4,403.71 +4.97%

Utilities 425.94 -1.88%

MSCI Emerging Markets 96.82 +.77%

S&P 500 Cum A/D Line 7,447.0 +10%

Bloomberg Oil % Bulls 21.21 -15.2%

CFTC Oil Large Speculative Longs 177,047 -1.0%

Put/Call .81 -19.80%

NYSE Arms 1.16 -1.77%

Volatility(VIX) 11.76 -10.64%

ISE Sentiment 67.0 -46.40%

AAII % Bulls 47.95 +11.54%

AAII % Bears 38.36 +28.25%

US Dollar 85.97 +.03%

CRB 306.32 -4.39%

ECRI Weekly Leading Index 136.60 +.66%

Futures Spot Prices

Crude Oil 63.35 -4.25%

Unleaded Gasoline 157.45 -2.42%

Natural Gas 5.01 -11.48%

Heating Oil 171.08 -7.30%

Gold 584.10 -2.27%

Base Metals 222.74 -6.15%

Copper 333.0 -2.75%

10-year US Treasury Yield 4.79% +.63%

Average 30-year Mortgage Rate 6.47% +.42%

Leading Sectors

I-Banks +7.39%

Airlines +6.68%

Retail +6.14%

Homebuilders +5.79%

Semis +5.69%

Lagging Sectors

Utilities -1.88%

Coal -2.81%

Energy -4.05%

Oil Service -4.69%

Gold & Silver -10.25%

One-Week High-Volume Gainers

One-Week High-Volume Losers

*5-Day % Change

S&P 500 1,319.87 +1.61%

DJIA 11,560.77 +1.48%

NASDAQ 2,235.99 +3.22%

Russell 2000 729.35 +2.94%

Wilshire 5000 13,193.31 +1.66%

S&P Barra Growth 614.22 +1.87%

S&P Barra Value 703.37 +1.36%

Morgan Stanley Consumer 650.81 +1.10%

Morgan Stanley Cyclical 815.78 +1.07%

Morgan Stanley Technology 521.98 +3.84%

Transports 4,403.71 +4.97%

Utilities 425.94 -1.88%

MSCI Emerging Markets 96.82 +.77%

S&P 500 Cum A/D Line 7,447.0 +10%

Bloomberg Oil % Bulls 21.21 -15.2%

CFTC Oil Large Speculative Longs 177,047 -1.0%

Put/Call .81 -19.80%

NYSE Arms 1.16 -1.77%

Volatility(VIX) 11.76 -10.64%

ISE Sentiment 67.0 -46.40%

AAII % Bulls 47.95 +11.54%

AAII % Bears 38.36 +28.25%

US Dollar 85.97 +.03%

CRB 306.32 -4.39%

ECRI Weekly Leading Index 136.60 +.66%

Futures Spot Prices

Crude Oil 63.35 -4.25%

Unleaded Gasoline 157.45 -2.42%

Natural Gas 5.01 -11.48%

Heating Oil 171.08 -7.30%

Gold 584.10 -2.27%

Base Metals 222.74 -6.15%

Copper 333.0 -2.75%

10-year US Treasury Yield 4.79% +.63%

Average 30-year Mortgage Rate 6.47% +.42%

Leading Sectors

I-Banks +7.39%

Airlines +6.68%

Retail +6.14%

Homebuilders +5.79%

Semis +5.69%

Lagging Sectors

Utilities -1.88%

Coal -2.81%

Energy -4.05%

Oil Service -4.69%

Gold & Silver -10.25%

One-Week High-Volume Gainers

One-Week High-Volume Losers

*5-Day % Change

Subscribe to:

Posts (Atom)