There are some economic reports of note and several significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - None of note

Tues. - Wholesale Inventories

Wed. - Sept. 20 FOMC Minutes

Thur. - Trade Balance, Initial Jobless Claims, Fed’s Beige Book

Fri. - Import Price Index, Advance Retail Sales, Univ. of Mich. Consumer Confidence, Business Inventories

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - Cheesecake Factory(CAKE)

Tues. - Alcoa(AA), Chattem(CHTT), Genentech(DNA)

Wed. - Gannett Co.(GCI), Lam Research(LRCX), M&T Bank(MTB), Monsanto(MON), Progressive Corp.(PGR), Ruby Tuesday(RI)

Thur. - Apollo Group(APOL), Fastenal Group(FAST), Genzyme Corp.(GENZ), Harley-Davidson(HDI), MGIC Investment(MTG), Polaris Industries(PII), Winnebago Industries(WGO)

Fri. - General Electric(GE), JB Hunt Transportation(JBHT), Regions Financial(RF)

Other events that have market-moving potential this week include:

Mon. - None of note

Tue. - (SPLS) Analyst and Investor Conference, (CVS) Sept. Sales release, (CIEND) Analyst Day

Wed. - Fed’s Bies speaking, Fed’s Lacker speaking

Thur. - (WEN) Analyst Meeting, Fed’s Beige Book, Fed’s Moskow speaking

Fri. - None of note

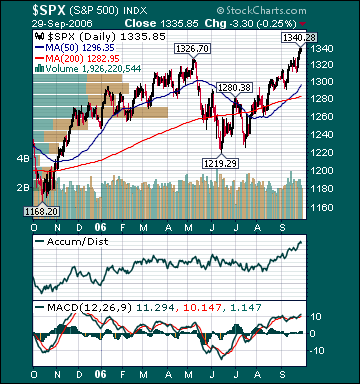

BOTTOM LINE: I expect US stocks to finish the week modestly higher on lower energy prices, short-covering, investment manager performance anxiety, bargain hunting, mostly positive economic reports and less pessimism. My trading indicators are still giving bullish signals and the Portfolio is 100% net long heading into the week.