There are a few economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - Leading Indicators

Tues. - Richmond Fed Manufacturing Index

Wed. - MBA Mortgage Applications, EIA Inventory Data

Thur. - Initial Jobless Claims, Existing Home Sales

Fri. - Durable Goods Orders, New Home Sales

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - American Express(AXP), CSX Corp.(CSX), Eaton Corp.(ETN), Pfizer Inc.(PFE), Texas Instruments(TXN)

Tues. - Adtran Inc.(ADTN), Advanced Micro Devices(AMD), AK Steel(AKS), Avaya Inc.(AV), Bank of America(BAC), Brinker Intl.(EAT), Burlington Northern(BNI), Centex Corp.(CTX), Coach Inc.(COH), DR Horton(DHI), EMC Corp.(EMC), Integrated Device Technology, Johnson & Johnson(JNJ), Microchip Tech(MCHP), QLogic Corp.(QLGC), Seagate Technologies(STX), UAL Corp.(UAUA), United Technologies(UTX), Wachovia Corp.(WB), Yahoo!(YHOO)

Wed. - Abbott Labs(ABT), Allegheny Technologies(ATI), AmerisourceBergen(ABC), Check Point Software(CHKP), ConocoPhillips(COP), Corning Inc.(GLW), eBay Inc.(EBAY), Ethan Allen(ETH), F5 Networks(FFIV), First Data(FDC), General Dynamics(GD), Hershey(HSY), Hutchinson Tech(HTCH), McDonald’s Corp.(MCD), NetFlix(NFLX), Novellus Systems(NVLS), Parametric Tech(PMTC), Qualcomm Inc.(QCOM), Ryland Group(RYL), Symantec Corp.(SYMC), Tidewater(TDW), Trident Microsystems(TRID), Varian Medical(VAR)

Thur. - Agere Systems(AGR), Altera Corp.(ALTR), Amgen Inc.(AMGN), AT&T(T), Baxter Intl(BAX), Beazer Homes(BZH), Bebe Stores(BEBE), Becton Dickinson(BDX), BJ Services(BJS), Bristol-Myers(BMY), Callaway Golf(ELY), Cardinal Health(CAH), Dow Jones(DJ), Federated Investors(FII), Ford Motor(F), Franklin Resources(BEN), ImClone Systems(IMCL), Intl. Rectifier(IRF), Kimberly-Clark(KMB), Lear Corp.(LEA), Legg Mason(LM), Lockheed Martin(LMT), Massey Energy(MEE), Maxim Integrated(MXIM), MBIA Inc.(MBI), McKesson Corp.(MCK), Microsoft Corp.(MSFT), Northrop Grumman(NOC), Peabody Energy(BTU), Quest Diagnostics(DGX), St Jude Medical(STJ), Stryker Corp.(SYK), Sybase Inc.(SY), Union Pacific(UNP), Western Digital(WDC), Zoll Medical(ZOLL)

Fri. - Avid Tech(AVID), Caterpillar Inc.(CAT), CDW Corp.(CDWC), Dolby Labs(DLB), Fortune Brands(FO), Halliburton(HAL), Honeywell Intl(HON), Southern Copper(PCU), T Rowe Price Group(TROW)

Other events that have market-moving potential this week include:

Mon. - AG Edwards Retailing Conference, (TGT) Sales Update, (PFE) Analyst Meeting, Fed’s Yellen speaking

Tue. - AG Edwards Retailing Conference, State of the Union Address, (KMI) Analyst Meeting, (XTO) Analyst Conference

Wed. - None of note

Thur. - Bank of America Out of the Box REIT Summit

Fri. - None of note

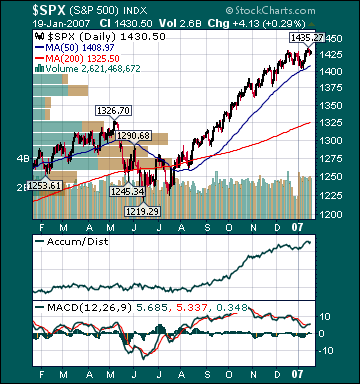

BOTTOM LINE: I expect US stocks to finish the week mixed as mostly positive economic data, buyout speculation, stable long-term rates, mostly positive earnings reports and constructive Fed comments offsets profit-taking and shorting. My trading indicators are giving mostly bullish signals and the Portfolio is 75% net long heading into the week.