Bloomberg:

- Crude oil is falling .78/bbl. to $59.27/bbl., breaking down through its recent uptrend line, on speculation US fuel demand will ease with the end of the northern hemisphere winter.

- It will take more than a shakeout in the US mortgage market and a two-week stumble in global equity prices to derail Wall Street’s earnings streak.

- A US bankruptcy judge ordered hedge funds to disclose details of their holdings in Northwest Airlines, a ruling that may quell the enthusiasm of investor groups to band together and exert influence over bankrupt companies.

- Venezuelan President Hugo Chavez, visiting Bolivia, said Socialism is the solution for the region’s problems.

- China will keep buying US Treasuries after a new state investment agency begins operations to help the nation manage its $1.07 trillion foreign-exchange reserves, central bank Vice Governor Wu Ziaoling said.

- China’s inflation rate probably accelerated to a two-year high in February, increasing the chances that the central bank will raise interest rates.

- President Bush is right not to succumb to pressure to set a date for the withdrawal of US troops from Iraq as it would trigger a surge in violence, former US Secretary of State James Baker said. “You will increase the risk of greater instability and perhaps even a regional war. The minute you put a deadline in there your enemies will react accordingly,” Baker said.

- The world’s best-performing currency against the dollar in the past month may lose its 3.1% gain as Japanese pensioners pursue higher returns at the start of the country’s fiscal year.

- Actor and former Republican Senator Fred Thompson said today he is considering a run for president in the 2008 election.

- Federal Reserve Governor Randall Kroszner said a worldwide glut of savings and a commitment by global central banks to curb inflation may help to keep longer-term interest rates at relatively low levels.

- French President Jacques Chirac’s decision to rule out a third term ends a four-decade political career and leaves Interior Minister Nicolas Sarkozy as the sole candidate from his Union for a Popular Movement.

- Japan’s economy expanded at a faster-than-expected 5.5% pace in the fourth quarter, buoyed by an increase in capital spending.

- Andrew Harrington, a commodity analyst at Australia & New Zealand Banking Group sees copper prices falling on slowing demand from China.

Wall Street Journal:

- Google Inc.(GOOG) began selling and serving television commercials last year to subscribers of a cable television company in Concord, California. Google sells the ads through an auction system, and they then appear during normal commercial breaks for Wave Broadband unit Astound Broadband’s 25,000 viewers.

Barron’s:

- Sam Zell, a Chicago billionaire and real-estate investor, bid $13 billion for publisher Tribune Co.(TRB), topping other offers.

NY Times:

- Google(GOOG) offers workers another perquisite besides free gourmet food, on-site car washes and oil changes – free shuttle buses to and from outlying areas to its Silicon Valley headquarters. Other technology companies such as Yahoo!(YHOO) and eBay(EBAY) have begun offering similar programs, which help attract and keep workers.

- More married couples are choosing to sleep in separate bedrooms instead of just separate beds, which often reflects busier lifestyles and different sleep schedules, citing a homebuilder survey.

NY Post:

- Starbucks Corp.(SBUX) may start its own record label and sign former Beatle Paul McCartney as its first artist.

San Francisco Chronicle:

- The California Nurses Assoc. will join the AFL-CIO labor union to push for health-care reform.

- BP Plc’s(BP) $500 million agreement with the Univ. of California at Berkeley for energy research plans to produce enough bio-fuel to cause a decline in carbon emissions linked to vehicles.

San Jose Mercury News:

- Peet’s Coffee & Tea(PEET) plans to increase its number of stores by 22% this year, primarily in Northern California.

Washington Post:

- Democratic presidential hopeful Hillary Clinton will for the first time back a deadline for withdrawing US troops from Iraq in a vote on a resolution expected in the Senate next week. The measure’s key provision would call on President Bush to begin redeploying US forces from Iraq within four months.

CNNMoney.com:

- Top funds stand by sub-prime bet.

AP:

- Mexico’s president said threats from drug traffickers against his government would not deter a military crackdown against them and that the US must do more to fight drugs domestically.

Business Week:

- Crumbling roads, jammed airports and power blackouts could hobble India’s growth.

Financial Times:

- UK house prices rose by an annualized 7.6% in February.

- Releasing movies simultaneously in cinemas, to DVD rental chains and on the Internet could increase studios revenue up to 165, citing research to be published in the Journal of Marketing.

Sunday Telegraph:

- BG Group Plc may become the first major Western energy company to invest in Iraq. Iraq has the largest petroleum reserves after Saudi Arabia and much of it is considered simple to extract.

Die Welt:

- German renewable energy companies may employ twice as many people or 500,000 by 2020 because of new European Union targets to cut greenhouse gases.

21st Century Business Herald:

- More than fifty percent of wine and imported liquor in Shanghai is fake and doesn’t come from original sources.

JoongAng Ilbo:

- North Korea will disable its 5-megawatt Yongbyon nuclear reactor within one year, citing the North’s chief nuclear negotiator.

Iran Daily:

- Iran’s Interior Ministry may sign contracts worth $20 billion with China for urban development projects in the Islamic Republic.

Tehran Times:

- Iran is ready to pay Russia extra money so that it finishes the Islamic Republic’s first nuclear power plant, citing Mohammed Saaedi, deputy head of the Atomic Energy Organization of Iran.

Weekend Recommendations

Barron's:

- Made positive comments on (MDT), (SNPS), (MOT)/(BA) bonds and (CEG).

Citigroup:

- Reiterated Buy on (SNPS), target $34.

- Upgraded (RDN) to Buy, target raised to $69.

- Upgraded (MTG) to Buy, target $71.

Night Trading

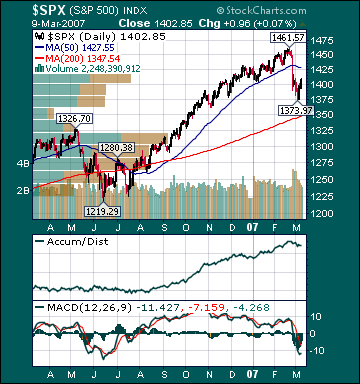

Asian indices are +.75% to +1.0% on average.

S&P 500 indicated +.07%.

NASDAQ 100 indicated +10%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Conference Calendar

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (JAS)/.98

- (TSAI)/.40

- (HTZ)/.10

Upcoming Splits

- (GES) 2-for-1

- (WCN) 3-for-2

Economic Releases

2:00 pm EST

- Monthly Budget Statement for February is estimated to widen to -$121.0B versus -$119.2B in January.

BOTTOM LINE: Asian Indices are higher, boosted by technology shares in the region. I expect US stocks to open modestly higher and to maintain gains into the afternoon. The Portfolio is 75% net long heading into the week.