Weekend Headlines

Bloomberg:

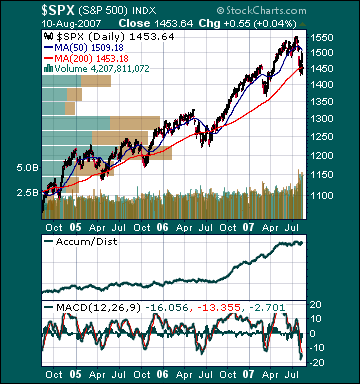

- US stocks gained for the first time in four weeks on speculation the government will take steps to avert a lending crisis, helping the market overcome increasing home-loan and hedge fund losses.

- The “solidity” of BNP Paribas SA, Frances’s biggest bank, isn’t affected by the subprime crisis rippling through financial markets, Alain Papiasse, head of the bank’s asset management and services division, said in an interview published today in Le Parisien.

- Gold is going nowhere. Dollar-prcied bullion, a traditional haven for investors in times of turmoil, is lagging behind US Treasuries.

- Countrywide Financial Corp.(CFC) CEO Mozilo said the US Federal Reserve’s decision to pump more than $38 billion into the banking system may bolster confidence and help restart stalled credit markets.

- Treasuries posted their first weekly decline since early July after the Federal Reserve added $62 billion to the banking system to help avert a crisis of confidence in global credit markets.

- Hedge fund manager DE Shaw increased to 5.3% its stake in mortgage insurer Radian Group(RDN), according to a regulatory filing Friday.

- The yen’s seven-week rally is about to end.

- Pakistani and Afghan tribal leaders took a “positive” first step in the fight against terrorism by agreeing at their peace council to boost cooperation along the border, Pakistan’s President Pervez Musharraf said.

- The speculative grade bond credit default swap index fell 20.5% last week, on renewed optimism, after central banks boosted global liquidity.

Wall Street Journal:

- Northwest Airlines Corp.(NWA) is considering becoming a passive investor with one of four parties that may bid for Midwest Airlines.

- Crude-oil futures are feeling the tremors emanating from the credit markets and are weakening on fears that they could be the next casualty of the risk exodus.

- S&P 500 Looks On Cheap Side Amid Turmoil.

NY Times:

- The sharp stock market decline that began in late July is more likely to be a minor downturn in a continuing bull market than the beginning of a major bear market. That, at least, is the conclusion of an extensive analysis of corporate insiders’ trading behavior.

- Fund managers, who make what they consider conservative investments based on computerized calculations, are being blindsided by “model misbehavior,” Gretchen Morgenson wrote.

- A 75% drop in the overseas-based communications collected by

- Novell Inc.(NOVL) owns the copyrights covering the Unix operating system, not SCO Group Inc., which may jeopardize that company’s lawsuits against Novell and International Business Machines(IBM).

- Democratic presidential candidates are detailing positions that might keep US troops in

- Cases of the sexually transmitted disease syphilis have risen among women in NYC as bisexual relationships increase, citing the Department of Health and Mental Hygiene.

- Cage-free egg demand is rising faster than production as corporations including Google Inc.(GOOG) add them to their cafeteria menu and Whole Foods Market(WFMI) sell them exclusively.

Barron’s:

- Shares of Bear Stearns(BSC), the second-largest underwriter of mortgage bonds, may sell at double their current price should the company consider merging with or being acquired by a larger company.

- Scott Barbee, managing director of the Aegis Value Fund, won the No. 1 spot in the 12th annual Barron’s/Value Line list of the top 100 US mutual-fund managers.

MarketWatch.com:

- Big liquidation triggers hedge-fund turmoil. Some compare upheaval to LTCM collapse; market neutral funds are hit hard.

- Google, Cisco don’t collateralize loans. Commentary: Ignore analysts, look to debt-free tech sector for safe haven.

AP:

- Gas prices drop nearly 11 cents in last 2 weeks.

CBS News.com:

- Credit Crisis? Not Really. National Review Online: Sub-Prime Mortgage Market Woes Are Greatly Exaggerated.

LA Times:

- Conditions at

- NBC Universal may buy Oxygen Media, the closely held owner of the Oxygen cable television network, for as much as $3 billion.

Forbes.com:

- Consumer Spending Will Not Collapse in Face of Housing Correction.

Oil & Gas Journal:

- US oil drilling activity hit a 21-year high last week, according to Baker Hughes.

Financial Times:

- The much-heralded financial rocket scientists responsible for the explosion in complex mathematical trading strategies are bracing themselves for fresh pain after what one team of analysts called “the perfect storm” last week.

- Wall street is braced this week for the most anticipated technology IPO in years as VMware, a fast-growing software company, prepares to float 10% of its shares on the stock market.

- General Motors(GM) may allow buyers of its Chevy Volt electric car to rent the vehicle’s battery as a way of pricing the vehicle at a comparable level to a traditional, petrol-driven family saloon.

- Central banks are expected to continue intervening in the money markets on Monday in an effort to unblock the financial system after last week’s turmoil.

Daily Telegraph:

- Hedge fund panic was behind global stock markets collapse.

AFP:

-

Sunday Times:

- Nasdaq Stock Market(NDAQ) may sell part of its stake in London Stock Exchange Group Plc to fund a higher offer for Swedish exchange operator OMX AB.

- Bank of

Weekend Recommendations

Barron's:

- Made positive comments on (BSC), (GLW) and (ZRAN).

- Made negative comments on (CMG).

Citigroup:

- We are upgrading (AVT) and (ARW) to Buy from Hold. We see

- Reiterated Buy on (INTU), target $35.

- While we cannot hope to predict the outcomes of the current credit market volatility, we emphasize that semiconductor fundamentals are strong. Consistent with the view from out strategist and economist, we expect technology to be a leader from this current market weakness, and we expect semiconductors to play a vital role in this. We continue to favor (INTC), (MU), (TXN), (SPSN) and (IDTI).

Night Trading

Asian indices are -.25% to +.75% on average.

S&P 500 futures +.75%.

NASDAQ 100 futures +.67%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Pre-market Stock Quote/Chart

Before the Bell CNBC Video(bottom right)

Global Commentary

WSJ Intl Markets Performance

Commodity Movers

Top 25 Stories

Top 20 Business Stories

Today in IBD

In Play

Bond Ticker

Economic Preview/Calendar

Daily Stock Events

Macro Calls

Upgrades/Downgrades

Rasmussen Business/Economy Polling

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (BX)/.34

- (BOBE)/.36

- (CNK)/.09

- (DV)/.25

- (DTE)/.47

- (NTES)/.29

- (SYY)/.46

Upcoming Splits

- (SHEN) 3-for-1

Economic Releases

8:30 am EST

- Advance Retail Sales for July are estimated to rise .2% versus a -.9% decline in June.

- Retail Sales Less Autos for July are estimated to rise .4% versus a -.4% decline in June.

10:00 am EST

- Business Inventories for June are estimated to rise .4% versus a .5% increase in May.

Other Potential Market Movers

- The Keefe Bruyette & Woods Bank Conference could also impact trading today.