Market Snapshot

Detailed Market Summary

Quick Summary

Economic Commentary

Movers & Shakers

Today in IBD

NYSE OrderTrac

I-Watch Sector Overview

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Option Dragon

Real-time Intraday Chart/Quote

Monday, December 04, 2006

Sunday, December 03, 2006

Monday Watch

Weekend Headlines

Bloomberg:

- Federal Reserve Vice Chairman Donald Kohn said that inflation is beginning to recede even as risks remain “tilted to the upside.”

- Saudi Arabian Oil Minister Ali Al-Naimi said crude inventories are too high. Global oil inventories stand at 2.3 billion barrels, Naimi said, which is 100 million barrels more than a year earlier.

- European stocks had their biggest weekly decline since July as the dollar fell against the euro and the pound.

- Pfizer Inc.’s(PFE) shares will likely drop after the world’s biggest drugmaker unexpectedly ended development of its most important drug

- The SEC postponed a vote on hedge-fund regulations scheduled for tomorrow to give agency staff more time to revise legal language.

- Tiger Woods plans to design a golf course in Dubai, United Arab Emirates, the first by his Tiger Woods Design company set up last month.

- US investors who are congratulating themselves for putting money into stocks in Europe and Asia may soon find the best times are over. US investors have poured $106.1 billion this year into mutual funds that invest in stocks outside the US, up 40% from the same period in 2005, according to a report last week from Banc of America. They have pulled $1.4 billion out of domestic stock funds, versus inflows of $18.7 billion a year earlier.

- Jinchuan Group Co. has completed construction of a copper smelter capable of producing 200,000 metric tons a year of the metal, doubling output capacity, used in wires and pipes.

- Russia’s oil production rose in November as ExxonMobil Corp.’s(XOM) project on Sakhalin Island increased output.

Wall Street Journal:

- Eli Lilly(LLY) CEO Sidney Taurel said government price-controls in the US would stifle research. Taurel said Euoprean companies 30 years ago were the most innovative. Since then, more drug research has shifted to the US. The CEO said drugmakers’ profits are compensation for long-term investments and that drugmakers are posting growth of 5% to 6%, less than the double-digit increases at the end of the last decade. He said they currently spend about 10 times as much on research and development as on marketing.

Time Magazine:

- President Bush may announce a new plan in coming weeks to link the level of American troops in Iraq with the performance of the Iraqi government in quelling violence.

NY Times:

- The crime rate in Venezuela has soared even as oil wealth has been used to try and cut poverty, and President Hugo Chavez has mostly ignored the violence. Homicides are up 67% since 1999, citing figures from the Criminal Investigation Police. Chavez’s government has pushed aside police officers who don’t agree with the president’s “socialist revolution” principles, citing crime analysts.

- Walt Disney(DIS) plans to produce brief cartoons again, after making few in the last half-century, beginning with a film showing character Goofy trying to figure out home-theater installation.

Philadelphia Inquirer:

- Verizon Communications(VZ) will challenge Comcast Corp.(CMCSA) in the Philadelphia-area market with a telephone, internet and television package it’s expected to start selling this week.

Washington Post:

- The American Civil Liberties Union(ACLU) urged the US government to end a program that screens and creates risk profiles for every airline traveler entering or leaving the US.

Detroit Free Press:

- DaimlerChrysler AG(DCX) will offer dealer incentives of as much as $7,000 per car to help clear out 2006 model-year vehicles beginning Dec. 5.

Financial Times:

- Goldman Sachs(GS) has developed a product that replicates the performance of thousands of hedge funds at a fraction of the cost to investors, citing Edgar Senior, Goldman’s executive director for fund derivative structuring. The Absolute Return Tracker index will replicate the aggregate position of the hedge fund industry. Goldman will charge a flat 1 percent annual fee, compared with between 4% and 7% charged for investments through funds of funds, and will allow trading on a daily basis.

- Hewlett-Packard(HPQ) will supply Amazon.com(AMZN) with high-speed digital printers for the online retailer’s books-on-demand service.

Sunday Times:

- First Data Corp.(FDC) may take over the credit card operation of Allied Irish Banks Plc, Ireland’s biggest lender my market value

Business Times:

- Western Digital(WDC) of the US may spend $150 million to more than double production at its Malaysian plant that makes hard-disk drives.

Weekend Recommendations

Barron's:

- Made positive comments on (RL), (DUK), (IBM), (CCRT) and (DTV).

Night Trading

Asian indices are -.25% to +.50% on average.

S&P 500 indicated -.15%

NASDAQ 100 indicated -.11%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Conference Calendar

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (CMTL)/.33

- (PLL)/.24

- (RVI)/.05

Upcoming Splits

- (AMED) 4-for-3

- (FMD) 3-for-2

Economic Releases

10:00 am EST

- Pending Home Sales for October are estimated to fall .5% versus a 1.1% decline in September.

Bloomberg:

- Federal Reserve Vice Chairman Donald Kohn said that inflation is beginning to recede even as risks remain “tilted to the upside.”

- Saudi Arabian Oil Minister Ali Al-Naimi said crude inventories are too high. Global oil inventories stand at 2.3 billion barrels, Naimi said, which is 100 million barrels more than a year earlier.

- European stocks had their biggest weekly decline since July as the dollar fell against the euro and the pound.

- Pfizer Inc.’s(PFE) shares will likely drop after the world’s biggest drugmaker unexpectedly ended development of its most important drug

- The SEC postponed a vote on hedge-fund regulations scheduled for tomorrow to give agency staff more time to revise legal language.

- Tiger Woods plans to design a golf course in Dubai, United Arab Emirates, the first by his Tiger Woods Design company set up last month.

- US investors who are congratulating themselves for putting money into stocks in Europe and Asia may soon find the best times are over. US investors have poured $106.1 billion this year into mutual funds that invest in stocks outside the US, up 40% from the same period in 2005, according to a report last week from Banc of America. They have pulled $1.4 billion out of domestic stock funds, versus inflows of $18.7 billion a year earlier.

- Jinchuan Group Co. has completed construction of a copper smelter capable of producing 200,000 metric tons a year of the metal, doubling output capacity, used in wires and pipes.

- Russia’s oil production rose in November as ExxonMobil Corp.’s(XOM) project on Sakhalin Island increased output.

Wall Street Journal:

- Eli Lilly(LLY) CEO Sidney Taurel said government price-controls in the US would stifle research. Taurel said Euoprean companies 30 years ago were the most innovative. Since then, more drug research has shifted to the US. The CEO said drugmakers’ profits are compensation for long-term investments and that drugmakers are posting growth of 5% to 6%, less than the double-digit increases at the end of the last decade. He said they currently spend about 10 times as much on research and development as on marketing.

Time Magazine:

- President Bush may announce a new plan in coming weeks to link the level of American troops in Iraq with the performance of the Iraqi government in quelling violence.

NY Times:

- The crime rate in Venezuela has soared even as oil wealth has been used to try and cut poverty, and President Hugo Chavez has mostly ignored the violence. Homicides are up 67% since 1999, citing figures from the Criminal Investigation Police. Chavez’s government has pushed aside police officers who don’t agree with the president’s “socialist revolution” principles, citing crime analysts.

- Walt Disney(DIS) plans to produce brief cartoons again, after making few in the last half-century, beginning with a film showing character Goofy trying to figure out home-theater installation.

Philadelphia Inquirer:

- Verizon Communications(VZ) will challenge Comcast Corp.(CMCSA) in the Philadelphia-area market with a telephone, internet and television package it’s expected to start selling this week.

Washington Post:

- The American Civil Liberties Union(ACLU) urged the US government to end a program that screens and creates risk profiles for every airline traveler entering or leaving the US.

Detroit Free Press:

- DaimlerChrysler AG(DCX) will offer dealer incentives of as much as $7,000 per car to help clear out 2006 model-year vehicles beginning Dec. 5.

Financial Times:

- Goldman Sachs(GS) has developed a product that replicates the performance of thousands of hedge funds at a fraction of the cost to investors, citing Edgar Senior, Goldman’s executive director for fund derivative structuring. The Absolute Return Tracker index will replicate the aggregate position of the hedge fund industry. Goldman will charge a flat 1 percent annual fee, compared with between 4% and 7% charged for investments through funds of funds, and will allow trading on a daily basis.

- Hewlett-Packard(HPQ) will supply Amazon.com(AMZN) with high-speed digital printers for the online retailer’s books-on-demand service.

Sunday Times:

- First Data Corp.(FDC) may take over the credit card operation of Allied Irish Banks Plc, Ireland’s biggest lender my market value

Business Times:

- Western Digital(WDC) of the US may spend $150 million to more than double production at its Malaysian plant that makes hard-disk drives.

Weekend Recommendations

Barron's:

- Made positive comments on (RL), (DUK), (IBM), (CCRT) and (DTV).

Night Trading

Asian indices are -.25% to +.50% on average.

S&P 500 indicated -.15%

NASDAQ 100 indicated -.11%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Before the Bell CNBC Video(bottom right)

Global Commentary

Asian Indices

European Indices

Top 20 Business Stories

In Play

Bond Ticker

Conference Calendar

Daily Stock Events

Macro Calls

Rasmussen Consumer/Investor Daily Indices

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (CMTL)/.33

- (PLL)/.24

- (RVI)/.05

Upcoming Splits

- (AMED) 4-for-3

- (FMD) 3-for-2

Economic Releases

10:00 am EST

- Pending Home Sales for October are estimated to fall .5% versus a 1.1% decline in September.

BOTTOM LINE: Asian Indices are mixed as losses in automaker shares are offsetting gains in technology stocks in the region. I expect US stocks to open modestly lower and to rally into the afternoon, finishing modestly higher. The Portfolio is 100% net long heading into the week.

Weekly Outlook

Click here for The Week Ahead by Reuters

There are a few economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - Pending Home Sales

Tues. - Challenger Job Cuts, Final 3Q Non-farm Productivity, Final 3Q Unit Labor Costs, Factory Orders, ISM Non-Manufacturing

Wed. - ADP Employment Change

Thur. - Initial Jobless Claims, Consumer Credit

Fri. - Change in Non-farm Payrolls, Unemployment Rate, Average Hourly Earnings, Univ. of Mich. Consumer Confidence

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - Pall Corp.(PLL)

Tues. - Activision Inc.(ATVI), Kroger(KO), Novell(NOVL), Photronics(PLAB), Sanderson Farms(SAFM), Toll Brothers(TOL), Witness Systems(WITS)

Wed. - John Wiley(JW/A), Korn/Ferry(KFY), OSI Restaurant Partners(OSI), Quanex Corp.(NX), Veritas DGC(VTS)

Thur. - Atwood Oceanics(ATW), Central Garden(CENT), Credence Systems(CMOS), Esterline Technologies(ESL), Jacuzzi Brands(JJZ), Jos. A. Bank Clothiers(JOSB), National Semi(NSM), Pathmark Stores(PTMK), Toro Co.(TTC), UTi Worldwide(UTIW), VeriFone Holdings(PAY)

Fri. - None of note

Other events that have market-moving potential this week include:

Mon. - Bank of America Credit Conference, UBS Global Media Conference, CSFB Media & Telecom Week, Bear Stearns Real Estate Conference

Tue. - Wachovia Real Estate Conference, Bank of America Credit Conference, Bear Stearns Real Estate Conference, CSFB Aerospace & Defense Conference, Citigroup Chemical Conference, Lehman Global Tech Conference, CSFB Media & Telecom Week, UBS Global Media Conference

Wed. - BMO Nesbitt Burns Healthcare Conference, Lehman Brothers Global Tech Conference, Citigroup Chemical Conference, CSFB Aerospace & Defense Conference, UBS Global Media Conference, CSB Media & Telecom Week, Piper Jaffray Online Ad & Search Symposium

Thur. - Lehman Global Tech Conference, UBS Global Media Conference, CSFB Aerospace & Defense Conference, CSFB Media & Telecom Week, Citigroup Global Paper & Forest Products Conference, BMO Nesbitt Burns Healthcare Conference, Cowen Internet Conference

Fri. - None of note

There are a few economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - Pending Home Sales

Tues. - Challenger Job Cuts, Final 3Q Non-farm Productivity, Final 3Q Unit Labor Costs, Factory Orders, ISM Non-Manufacturing

Wed. - ADP Employment Change

Thur. - Initial Jobless Claims, Consumer Credit

Fri. - Change in Non-farm Payrolls, Unemployment Rate, Average Hourly Earnings, Univ. of Mich. Consumer Confidence

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - Pall Corp.(PLL)

Tues. - Activision Inc.(ATVI), Kroger(KO), Novell(NOVL), Photronics(PLAB), Sanderson Farms(SAFM), Toll Brothers(TOL), Witness Systems(WITS)

Wed. - John Wiley(JW/A), Korn/Ferry(KFY), OSI Restaurant Partners(OSI), Quanex Corp.(NX), Veritas DGC(VTS)

Thur. - Atwood Oceanics(ATW), Central Garden(CENT), Credence Systems(CMOS), Esterline Technologies(ESL), Jacuzzi Brands(JJZ), Jos. A. Bank Clothiers(JOSB), National Semi(NSM), Pathmark Stores(PTMK), Toro Co.(TTC), UTi Worldwide(UTIW), VeriFone Holdings(PAY)

Fri. - None of note

Other events that have market-moving potential this week include:

Mon. - Bank of America Credit Conference, UBS Global Media Conference, CSFB Media & Telecom Week, Bear Stearns Real Estate Conference

Tue. - Wachovia Real Estate Conference, Bank of America Credit Conference, Bear Stearns Real Estate Conference, CSFB Aerospace & Defense Conference, Citigroup Chemical Conference, Lehman Global Tech Conference, CSFB Media & Telecom Week, UBS Global Media Conference

Wed. - BMO Nesbitt Burns Healthcare Conference, Lehman Brothers Global Tech Conference, Citigroup Chemical Conference, CSFB Aerospace & Defense Conference, UBS Global Media Conference, CSB Media & Telecom Week, Piper Jaffray Online Ad & Search Symposium

Thur. - Lehman Global Tech Conference, UBS Global Media Conference, CSFB Aerospace & Defense Conference, CSFB Media & Telecom Week, Citigroup Global Paper & Forest Products Conference, BMO Nesbitt Burns Healthcare Conference, Cowen Internet Conference

Fri. - None of note

BOTTOM LINE: I expect US stocks to finish the week modestly higher on better economic data, a stronger US dollar, lower energy prices, seasonal strength, strong corporate profits, bargain-hunting, investment manager performance anxiety and short-covering. My trading indicators are still giving bullish signals and the Portfolio is 100% net long heading into the week.

Saturday, December 02, 2006

Market Week in Review

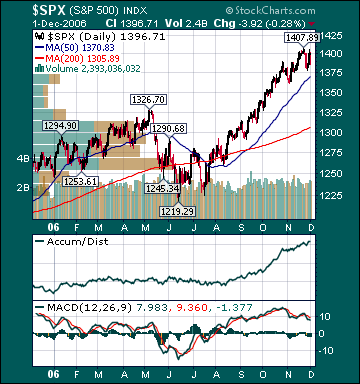

S&P 500 1,396.71 -.30%

Click here for the Weekly Wrap by Briefing.com.

*5-day % Change

Click here for the Weekly Wrap by Briefing.com.

BOTTOM LINE: Overall, last week's market performance was just mildly bearish. The advance/decline line fell, sector performance was mixed and volume was above average on the week. Measures of investor anxiety were mixed. The AAII % Bulls fell to 40.22% this week from 41.94% the prior week. This reading is still below average levels. The AAII % Bears surged again to 47.49% this week from 41.94% the prior week. This reading is now at elevated levels and the highest since July 20 of this year, the week the market began its recent bull run. The 10-week moving average of the % Bears is currently 36.1%, an above-average level. The 10-week moving average of the % Bears was 43.0% at the major bear market lows during 2002. Moreover, the 50-week moving-average of the % Bears is 36.23%, a very high level seen during only two other periods in U.S. history.

I continue to believe steadfastly high bearish sentiment in many quarters is mind-boggling, considering the S&P 500's 15.2% rise in just over five months, one of the best August/September/October runs in U.S. history and the fact that the Dow made another all-time high just ten trading days ago. Despite recent gains, the forward P/E on the S&P 500 is a very reasonable 15.8 due to the historic run of double-digit profit growth increases, which are poised to continue this quarter. Bears still remain stunningly complacent, in my opinion. As I have said many times over the last few months, the bears see every pullback as a major top and every move higher as just another shorting/selling opportunity.

As well, there are many other indicators registering high levels of investor skepticism regarding recent stock market gains. The 50-day moving average of the ISE Sentiment Index is still below its 200-day moving average. NYSE short interest is just .7% off record highs and up 21% since January. Absolute return investment strategies, which directly benefit from a stagnant or declining US stock market, continue to receive massive capital inflows. Moreover, public short interest continues to soar to record highs, and U.S. stock mutual funds have seen outflows for most of the year, according to AMG Data Services. Finally, investment blogger sentiment is still very bearish, with bulls recently making another new low. There is still a high wall of worry for stocks to climb substantially from current levels as the public and many professional investors remain very skeptical of this bull market.

I continue to believe this is a direct result of the belief by the herd that the U.S. is in a long-term trading range or secular bear environment. I strongly disagree with this view. There is overwhelming evidence that investment sentiment by the general public regarding U.S. stocks has never been this poor in history, with the Dow registering all-time highs almost weekly. I still expect the herd to finally embrace the current bull market next year, which should result in another significant move higher in the major averages as the S&P 500 breaks out to an all-time high to join the DJIA and Russell 2000. I continue to believe the coming bullish shift in long-term sentiment with regard to U.S. stocks will result in the "mother of all short-covering rallies."

The average 30-year mortgage rate fell 4 basis points to 6.14%, which is 66 basis points below July highs. I still believe housing is in the process of stabilizing at relatively high levels. Former Fed Chairman Alan Greenspan, current Fed Chairman Ben Bernanke and several current Fed members reiterated there belief recently that the “worst may well be over” for the housing slowdown. Mortgage applications have been trending higher with the decline in mortgage rates. As well, housing inventories have been trending lower and homebuilding equities have been moving higher. The Housing Index(HGX) has risen 22.1% from July lows. The Case-Shiller housing futures have improved recently and are now projecting a 3.4% decline in the average home price over the next 6 months. Considering the median house has appreciated over 50% during the last few years with record high US home ownership, this would be considered a “soft landing.” The overall negative effects of housing on the US economy and the potential for significant price drops are still being exaggerated by the bears in hopes of dissuading buyers from stepping in, in my opinion. Housing and home equity extractions have been slowing substantially for well over a year and have been mostly offset by many other very positive aspects of the economy.

Home values are more important than stock prices to the average American, but the median home has barely declined in value after a record run-up, while the S&P 500 has risen 12.5% over the last year and 88.2% since the Oct. 4, 2002 low. Americans’ median net worth is still very close to or at record high levels, a fact that is generally unrecognized or minimized by the record number of market participants that feel it is in their financial and/or political interests to paint a bleak picture of America. Moreover, energy prices are down, consumer spending remains healthy, unemployment is low by historic standards, interest rates are very low, stocks are surging and wages are rising. The economy has created almost half a million jobs in the last three months. The unemployment rate fell to a historically low 4.4% last month from 4.6% the prior month and 5.1% in September 2005, notwithstanding fewer real estate-related jobs and significant auto production cutbacks. Consumer spending is still above long-term average levels and looks poised to strengthen into year-end.

The Consumer Price Index for October rose 1.3% year-over-year, the smallest increase since June 2002 and down from 4.7% in September of 2005. This is substantially below the long-term average of around 3%. Moreover, the CPI has only been lower during 2 other periods since the mid-1960s. It was lower during late 1986 and early 2002-mid 2002. Many other measures of inflation have recently shown substantial deceleration. The Producer Price Index for October matched the largest decline in US history, falling 1.6% year-over-year. Most measures of Americans’ income growth are now around four times the rate of inflation.

The benchmark 10-year T-note yield fell 12 basis points on the week on diminishing inflation worries and rising growth concerns. In my opinion, investors’ continuing fears over an economic “hard landing” are still misplaced, notwithstanding recent weak manufacturing data. Manufacturing accounts for roughly 12% of US economic growth, while consumer spending accounts for about 70% of growth. U.S. GDP growth came in at 1.1% and 0.7% during the first two quarters of 1995. The ISM Manufacturing Index fell below 50 during May 1995. It stayed below 50, reaching a low of 45.5, until August 1996. During that period, the S&P 500 soared 31% as the P/E multiple expanded from 16.0 to 17.2. This was well before the stock market bubble began to inflate. As well, manufacturing was more important to US growth at that time. Stocks can and will rise as P/E multiples expand, even with more average economic and earnings growth. As I have said many times before, P/E multiple expansion is the US stock market bears' worst nightmare.

Weekly retail sales rose an above-average 3.2% for the week. Spending is poised to remain strong on lower energy prices, very low long-term interest rates, a rising stock market, healthy job market, decelerating inflation and more optimism. The CRB Commodities Index, the main source of inflation fears, has only risen .1% over the last 12 months and is down 12.1% from May highs despite a historic flood of capital into commodity funds and numerous potential upside catalysts. Oil has declined $15/bbl from July highs. The average commodity hedge fund is down substantially for the year. I continue to believe inflation fears have peaked for this cycle as global economic growth stabilizes around average levels, unit labor costs remain subdued and the mania for commodities continues to reverse course.

The EIA reported this week that gasoline supplies fell more than expectations even as refinery utilization rose. U.S. gasoline supplies are still at very high levels for this time of the year. Unleaded Gasoline futures rose for the week, but have plunged 42.1% from September 2005 highs even as some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. Gasoline demand is estimated to rise .8% this year versus a 20-year average of 1.7% demand growth. The still very elevated level of gas prices, related to crude oil production disruption speculation by investment funds, will further dampen global fuel demand, sending gas prices still lower over the intermediate-term.

US oil inventories are now approaching 8-year highs. Since December 2003, global oil demand is only up .7%, despite booming global growth, while global supplies have increased 6.3%, according to the Energy Intelligence Group. OPEC said this week that crude oil supply would exceed demand by 100 million barrels by the second quarter of next year. Moreover, worldwide oil inventories are poised to begin increasing at an accelerated rate over the next year. I continue to believe oil is priced at extremely elevated levels on fear and record speculation by investment funds, not fundamentals.

The Amaranth Advisors hedge fund blow-up is a prime example of the extent to which many investment funds have been speculating on ever higher energy prices through futures contracts, thus driving the price of the underlying commodity to absurd levels. Amaranth, a multi-strategy hedge fund, lost about $6.5 billion of its $9.5 billion under management in less than two months speculating mostly on higher natural gas prices. I continue to believe a number of other funds will experience similar fates over the coming months after managers “press their bets” in hopes of making up for poor performance, which will further pressure energy prices as these funds unwind their leveraged long positions to meet investor redemptions.

Oil has clearly broken its uptrend, notwithstanding this week’s bounce. Recently, Cambridge Energy Research, one of the most respected energy research firms in the world, put out a report that drills gaping holes in the belief by most investors of imminent "peak oil" production. Cambridge said that its analysis indicates that the remaining global oil base is actually 3.74 trillion barrels, three times greater than "peak oil" theory proponents say and that the "peak oil" theory is based on faulty analysis. I suspect the contango that currently exists in energy futures, which encourages hoarding, will begin to reverse over the coming months as more investors come to the realization that the "peak oil" theory is hugely flawed, global storage fills, and Chinese/US demand slows.

A major top in oil is likely already in place as global crude oil storage capacity utilization is running around 97%. Recent OPEC production cuts will likely result in a complete technical breakdown in crude. Demand destruction is already pervasive globally and will only intensify over the coming years as alternative energy projects come to the fore. Moreover, many Americans feel as though they are helping fund terrorism or hurting the environment every time they fill up their gas tanks. I do not believe we will ever again see the demand for gas-guzzling vehicles that we saw in recent years, even if gas prices plunge from current levels as I expect. OPEC production cuts, with oil still at very high levels and weakening global growth, only further deepens resentment towards the cartel and will result in even greater long-term demand destruction. Finally, as the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should continue heading meaningfully lower over the intermediate-term, notwithstanding OPEC production cuts. Oil will likely begin another significant downturn before year-end. I suspect crude will eventually fall to levels that most investors deemed unimaginable just a few months ago during the next significant global economic downturn.

Natural gas inventories fell more than expectations this week. Prices for the commodity rose as investment fund speculation remains near record highs despite the fact that supplies are now 7.2% above the 5-year average and at all-time high levels for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have collapsed 46.8% since December 2005 highs.

Gold rose only slightly on the week despite a weaker US dollar and rise in energy prices. The US dollar fell on weaker economic data and speculation that the European Central Bank will hike interest rates soon. I continue to believe there is very little chance of another Fed rate hike anytime soon. An eventual cut is likely next year as inflation continues to decelerate substantially. A Fed rate cut should actually boost the dollar as currency speculators anticipate faster US growth.

Energy stocks outperformed for the week on rising prices for the underlying commodities, increasing investment fund speculation and a weaker dollar. Airline stocks underperformed as oil prices rose and growth concerns intensified. S&P 500 profit growth for the third quarter came in around 20% versus a long-term historical average of 7%, according to Thomson Financial. This marks the 17th straight quarter of double-digit profit growth, the best streak since recording keeping began in 1936. Moreover, another double-digit gain is likely in the fourth quarter. Just a few months ago many investors expected profit growth to fall to the low single digits this year. Despite an 88.2% total return(which is equivalent to a 16.4% average annual return) for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 15.8. The 20-year average p/e for the S&P 500 is 24.4. The S&P 500 is now up 13.9% and the Russell 2000 Index is up 17.3% year-to-date. Historically, if the S&P 500 is up at least 10% going into the final two months of the year, which it was, it continues to climb the last two months 84% of the time.

Current stock prices are still providing longer-term investors very attractive opportunities, in my opinion. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. A CSFB report earlier this year confirmed this view. The report concluded that on a price-to-cash flow basis growth stocks are cheaper than value stocks for the first time since at least 1977. The entire decline in the S&P 500’s p/e, since the bubble burst in 2000, is attributable to growth stock multiple contraction. I still expect the most overvalued economically sensitive and emerging market stocks to continue underperforming over the intermediate-term as the manias for those shares subside and global growth slows to more average rates. I continue to believe a chain reaction of events has begun that will result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels, notwithstanding recent gains. One of the characteristics of the current “negativity bubble” is that most potential positives are undermined, downplayed or completely ignored, while almost every potential negative is exaggerated, trumpeted and promptly priced in to stock prices. Furthermore, this “irrational pessimism” by investors has resulted in a dramatic decrease in the supply of stock this year as companies bought back shares, IPOs were pulled and secondary stock offerings canceled. Booming merger and acquisition activity is also greatly constricting the supply of stock. Many commodity funds, which have received huge capital infusions this year, will likely see significant outflows at year-end. Some of this capital will likely find its way back to US stocks. As well, money market funds are brimming with cash. I continue to believe there is massive bull firepower available on the sidelines for US equities at a time when the supply of stock has contracted.

An end to the Fed rate hikes, lower commodity prices, seasonal strength, decelerating inflation readings, a strong holiday shopping season, lower long-term rates, increased consumer/investor confidence, short-covering, investment manager performance anxiety, rising demand for US stocks and the realization that economic growth is only slowing to around average levels should provide the catalysts for another substantial push higher in the major averages over the intermediate-term as p/e multiples expand further. I still expect the S&P 500 to return a total of at least 15% for the year. Another strong performance by US equities next year is likely. Finally, the ECRI Weekly Leading Index fell slightly this week and is forecasting a modest deceleration in US economic activity.

*5-day % Change

Friday, December 01, 2006

Weekly Scoreboard*

Indices

S&P 500 1,396.71 -.30%

DJIA 12,194.13 -.70%

NASDAQ 2,413.21 -1.91%

Russell 2000 781.17 -1.40%

Wilshire 5000 14,034.62 -.33%

S&P Barra Growth 649.14 -.27%

S&P Barra Value 745.29 -.33%

Morgan Stanley Consumer 671.94 -.56%

Morgan Stanley Cyclical 877.46 -1.52%

Morgan Stanley Technology 567.48 -2.75%

Transports 4,707.17 -2.85%

Utilities 457.66 +1.57%

MSCI Emerging Markets 109.35 +.31%

S&P 500 Cum A/D Line 8,567 -2.0%

Bloomberg Crude Oil % Bulls 73.0 +52.0%

CFTC Oil Large Speculative Longs 169,872 +3.0%

Put/Call .89 -9.90%

NYSE Arms 1.31 -3.29%

Volatility(VIX) 11.66 +12.67%

ISE Sentiment 121.0 +17.92%

AAII % Bulls 40.22 -4.1%

AAII % Bears 47.5 +13.2%

US Dollar 82.48 -1.4%

CRB 321.23 +3.97%

ECRI Weekly Leading Index 137.10 -.36%

Futures Spot Prices

Crude Oil 63.70 +7.0%

Unleaded Gasoline 168.50 +6.57%

Natural Gas 8.40 +3.38%

Heating Oil 185.62 +7.14%

Gold 651.0 +.65%

Base Metals 244.10 +.44%

Copper 317.50 -1.01%

10-year US Treasury Yield 4.43% -2.6%

Average 30-year Mortgage Rate 6.14 -.65%

Leading Sectors

Energy +5.27%

Gold & Silver +4.23%

Homebuilders +2.40%

HMOs +1.97%

Hospitals +1.49%

Lagging Sectors

Semis -3.67%

Oil Tankers -3.67%

Disk Drives -4.0%

I-Banks -5.13%

Airlines -6.8%

One-Week High-Volume Gainers

One-Week High-Volume Losers

*5-Day % Change

S&P 500 1,396.71 -.30%

DJIA 12,194.13 -.70%

NASDAQ 2,413.21 -1.91%

Russell 2000 781.17 -1.40%

Wilshire 5000 14,034.62 -.33%

S&P Barra Growth 649.14 -.27%

S&P Barra Value 745.29 -.33%

Morgan Stanley Consumer 671.94 -.56%

Morgan Stanley Cyclical 877.46 -1.52%

Morgan Stanley Technology 567.48 -2.75%

Transports 4,707.17 -2.85%

Utilities 457.66 +1.57%

MSCI Emerging Markets 109.35 +.31%

S&P 500 Cum A/D Line 8,567 -2.0%

Bloomberg Crude Oil % Bulls 73.0 +52.0%

CFTC Oil Large Speculative Longs 169,872 +3.0%

Put/Call .89 -9.90%

NYSE Arms 1.31 -3.29%

Volatility(VIX) 11.66 +12.67%

ISE Sentiment 121.0 +17.92%

AAII % Bulls 40.22 -4.1%

AAII % Bears 47.5 +13.2%

US Dollar 82.48 -1.4%

CRB 321.23 +3.97%

ECRI Weekly Leading Index 137.10 -.36%

Futures Spot Prices

Crude Oil 63.70 +7.0%

Unleaded Gasoline 168.50 +6.57%

Natural Gas 8.40 +3.38%

Heating Oil 185.62 +7.14%

Gold 651.0 +.65%

Base Metals 244.10 +.44%

Copper 317.50 -1.01%

10-year US Treasury Yield 4.43% -2.6%

Average 30-year Mortgage Rate 6.14 -.65%

Leading Sectors

Energy +5.27%

Gold & Silver +4.23%

Homebuilders +2.40%

HMOs +1.97%

Hospitals +1.49%

Lagging Sectors

Semis -3.67%

Oil Tankers -3.67%

Disk Drives -4.0%

I-Banks -5.13%

Airlines -6.8%

One-Week High-Volume Gainers

One-Week High-Volume Losers

*5-Day % Change

Subscribe to:

Posts (Atom)