Click here for Stocks in Focus for Monday by MarketWatch

There are a number of economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - NAHB Housing Market Index

Tues. - Housing Starts, Building Permits, weekly retail sales

Wed. - weekly MBA Mortgage Applications, FOMC Rate Decision

Thur. - Initial Jobless Claims, Continuing Claims, Leading Indicators

Fri. - Existing Home Sales

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - None of note

Tues. - Adobe Systems(ADBE), Chaparral Steel(CHAP), Cintas Corp.(CTAS), Commercial Metals(CMC), Darden Restaurants(DRI), Factset Research(FDS), Oracle Corp.(ORCL), Shuffle Master(SHFL), Sonic Corp.(SONC)

Wed. - Charming Shoppes(CHRS), FedEx(FDX), Morgan Stanley(MS), Ross Stores(ROST)

Thur. - Barnes & Noble(BKS), Borders Group(BGP), ConAgra Foods(CAG), General Mills(GIS), Georgia Gulf(GGC), Herman Miller(MLHR), KB Home(KBH), Nike Inc.(NKE), Palm Inc.(PALM), Williams-Sonoma(WSM)

Fri. - Apollo Group(APOL), Family Dollar(FDO), Freddie Mac(FRE)

Other events that have market-moving potential this week include:

Mon. - Lehman Brothers Global Healthcare Conference, the Bank of Japan Policy Meeting

Tue. - Lehman Brothers Global Healthcare Conference, AG Edwards Energy Conference, (CAKE) analyst day

Wed. - Lehman Brothers Global Healthcare Conference, JPMorgan Insurance Conference, JPMorgan Aviation & Transport Conference, AG Edwards Energy Conference, Merrill Lynch Retailing Leaders Conference, BB&T Manufacturing & Materials Conference, JPMorgan Gaming/Lodging/Restaurant Conference

Thur. - BB&T Manufacturing & Materials Conference, JPMorgan Aviation & Transport Conference, Merrill Lynch Retailing Leaders Conference, JPMorgan Gaming/Lodging/Restaurant Conference, (ADP) analyst meeting

Fri. - (BEAV) analyst meeting, the Fed’s Plosser speaking

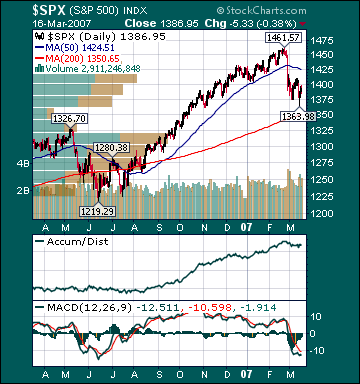

BOTTOM LINE: I expect US stocks to finish the week modestly higher on buyout speculation, constructive FOMC comments, mostly positive earnings reports, short-covering and bargain-hunting. My trading indicators are giving mixed signals and the Portfolio is 75% net long heading into the week.