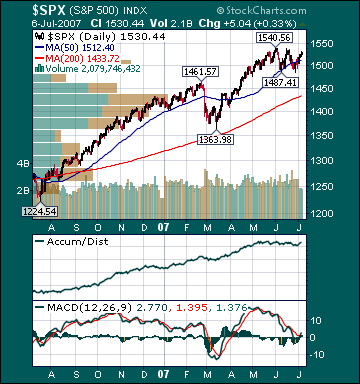

S&P 500 1,530.44 +1.64%*

*5-day % Change

Indices

S&P 500 1,530.44 +1.64%

DJIA 13,611.68 +1.41%

NASDAQ 2,666.51 +2.23%

Russell 2000 852.31 +1.58%

Wilshire 5000 15,456.07 +1.77%

Russell 1000 Growth 609.19 +2.14%

Russell 1000 Value 871.56 +1.45%

Morgan Stanley Consumer 735.70 +.73%

Morgan Stanley Cyclical 1,100.52 +2.50%

Morgan Stanley Technology 637.22 +1.87%

Transports 5,231.29 +1.91%

Utilities 505.16 +1.80%

MSCI Emerging Markets 137.60 +4.89%

Sentiment/Internals

NYSE Cumulative A/D Line 77,548 +4.35%

Bloomberg New Highs-Lows Index +561 +289.6%

Bloomberg Crude Oil % Bulls 44.0 -9.3%

CFTC Oil Large Speculative Longs 197,493 -1.63%

Total Put/Call .86 unch.

NYSE Arms .62 -50.79%

Volatility(VIX) 14.72 -5.28%

ISE Sentiment 140.0 -17.6%

AAII % Bulls 43.8 +12.3%

AAII % Bears 32.88 -8.1%

Futures Spot Prices

Crude Oil 72.81 +4.57%

Reformulated Gasoline 230.96 +4.39%

Natural Gas 6.44 -3.17%

Heating Oil 209.51 +3.26%

Gold 654.80 +.55%

Base Metals 257.77 +2.66%

Copper 359.45 +4.84%

Economy

10-year US Treasury Yield 5.18% +15 basis points

4-Wk MA of Jobless Claims 318,500 +.5%

Average 30-year Mortgage Rate 6.63% -4 basis points

Weekly Mortgage Applications 619.40 +.13%

Weekly Retail Sales +1.6%

Nationwide Gas $2.95/gallon -.02/gallon

US Cooling Demand Next 7 Days 15.0% above normal

ECRI Weekly Leading Economic Index 143.0 +.14%

US Dollar Index 81.46 -1.05%

CRB Index 320.86 +2.59%

Leading Sectors

Alternative Energy +4.77%

Airlines +4.15%

Wireless +4.15%

Oil Service +4.03%

REITs +3.32%

Lagging Sectors

Insurance +.44%

Drugs +.43%

Banks +.40%

Foods +.06%

Biotech -.09%

|

BOTTOM LINE: The Portfolio is higher into the final hour on gains in my Retail longs, I-Banking longs, Semi longs and Medical longs. I have not traded today, thus leaving the Portfolio 100% net long. The tone of the market is positive today as the advance/decline line is higher, most sectors are gaining and volume is below average. Just like last year before oil peaked on July 14 and then proceeded to plunge $28 per barrel in six months, it is just assumed by many that oil will continue heading higher forever. I am already hearing the $100 per barrel oil calls that came last year around this time. The fundamentals for oil are even worse this year, in my opinion. Core inflation is already decelerating meaningfully. I suspect a significant decline in energy prices that begins over the next couple of months will help bring headline inflation readings down even further before year-end, which should also help bring long-term interest rates back down. Significantly lower energy prices, lower long-term rates, higher stock prices, wages continuing to substantially outpace inflation, low unemployment and stabilizing home sales should help boost consumer spending back to above-average rates this fall. Retail stocks have held up very well despite the many perceived headwinds of late. I suspect retailers will begin to outperform the market again this quarter as investors anticipate these catalysts. I remain long Under Armour(UA) and Tractor Supply (TSCO). For the first time in a long time, domestic fund inflows substantially exceeded non-domestic fund inflows this week.

Here is a summary of AMG Data Services fund flows for the week ended July 3:

Bloomberg:

- Goldman Sachs Group(GS) said law-enforcement authorities don’t consider letters making threats against the company to be credible.

- North Korea may shut its Yongbyon nuclear power plant as soon as it gets one-10th to 50,000 tons of heavy fuel oil promised in an international agreement, rather than wait for the full amount, its official news agency said.

- Federal Reserve Bank of San Francisco President Janet Yellen said the central bank’s stance of keeping interest rates unchanged is most likely to achieve faster growth and slower inflation.

- Citadel Investment Group LLC almost doubled its stake in Myriad Genetics(MYGN) to 5.5%.

- John Lonski, chief economist at Moody’s Investors Service(MCO) sees

- Share sales by wind, solar and biofuels companies attracted 8% more investment in the first six months of 2007 than a year earlier, led by energy-efficiency and service industries, New Energy Finance said.

- Investing in renewable energy could save the world $180 billion a year in fuel costs by 2030 while reducing emissions of carbon dioxide, the main gas blamed for global warming, according to a recent report by Greenpeace and the European Renewable Energy Council.

- Coffee futures fell for a fourth straight session in

- Stainless-steel output rose 15% to 7.58 million metric tons in the first quarter from a year ago, driven by increases in

- Natural gas in NY is falling another 3% after a government report today showed supplies are heading towards a new all-time record by October.

Wall Street Journal:

-

- The US Congress needs to respond to Iran’s growing involvement in training and organizing extremists fighting US forces in Iraq, Senator Joseph Lieberman wrote.

- The new US Regulation NMS, which requires brokers to send orders instantly to the market showing the best prices, will help larger securities firms at the expense of smaller ones.

- The White House’s Office of Management and Budget will advise President Bush to veto a bill that would allow members of OPEC to be sued under

- The

- Chicago Mercantile Exchange(CME) will increase its offer for CBOT Holdings Inc.(BOT) in an attempt to get shareholders to approve its bid for the parent of the Chicago Board of Trade.

NY Times:

- In 2005, about the time when hedge funds started sprouting like weeds, investors, money managers and the media started to question whether there might be a hedge fund bubble. With hedge funds lining up to go public, the questioning has turned up a notch.

Financial Times:

- The Bank of England’s decision to raise interest rates to 5.75% and perhaps beyond could severely hurt the

Financial Times Deutschland:

- Hewlett-Packard(HPQ) may acquire more software companies, citing an interview with Hans Ulrich Holdenried, who heads the company’s German unit.

- Steel production in

The Business:

- Dow Jones’ board is confident that the Bancroft family, which controls the majority of voting shares, will approve an agreement for Rupert Murdoch’s News Corp.(NWS/A) to buy the company.

- The Change in Non-farm Payrolls for June was 132K versus estimates of 125K and an upwardly revised 190K in May.

- The Unemployment Rate for June came in at 4.5% versus estimates of 4.5% and 4.5% in May.

- Average Hourly Earnings for June rose .3% versus estimates of a .3% gain and an upwardly revised .4% gain in May.

BOTTOM LINE: Employers in the

Furthermore, most measures of Americans’ income growth are almost twice the rate of inflation. Average Hourly Earnings rose 3.9% year-over-year in June, substantially above the 3.2% 20-year average. The 11-month moving-average of Americans’ Average Hourly Earnings is currently 4.04%. 1998 was the only year during the 90s expansion that it exceeded current levels. This high level of earnings growth comes as the CPI for May rose 2.7% year-over-year, down from a 4.7% increase in September 2005 and well below the 20-year average of 3.1%. Long-term interest rates remain very low by historic standards despite the recent up-tick related to stronger economic growth.

Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote