Click here for the Weekly Wrap by Briefing.com.

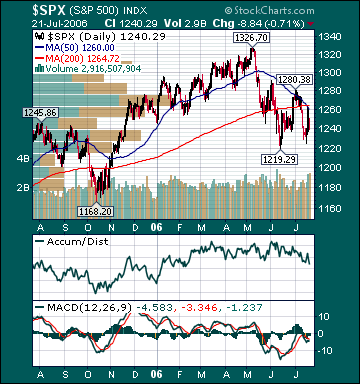

BOTTOM LINE: Overall, last week's market performance was neutral. The advance/decline line fell slightly, sector performance was mixed and volume was above average on the week. Measures of investor anxiety were higher. The AAII % Bulls plunged to 23.85% this week from 36.50% the prior week. This reading is now at depressed levels. The AAII % Bears soared to 57.80% from 39.42% the prior week. This reading is now at elevated levels. Moreover, the 10-week moving average of the % Bears is 43.01%, the highest since the bear market bottom in October 2002. The % Bears has only been this high during two other periods in history since the survey began in 1987. During the 1990 recession and Gulf War the % Bears reached 67.0% and during the 2002-03 recession and tail end of one of the greatest stock market collapses in U.S. history the % Bears reached 57.89%. Many other measures of investor sentiment are also at levels associated with meaningful market bottoms.

The average 30-year mortgage rate fell to 6.80%, which is 159 basis points above all-time lows set in June 2003. I still believe housing is in the process of slowing to more healthy sustainable levels. Mortgage rates should begin an intermediate-term move lower next week.

The benchmark 10-year T-note yield fell 4 basis points on the week as economic data were mixed, commodity prices declined and the Fed made dovish comments. I still believe inflation concerns have peaked for the year as investors continue to anticipate slower economic growth, unit labor costs remain subdued and the mania for commodities continues to reverse course. The fact that commodities fell sharply on the week despite a report of soaring growth in China, rising Middle East tensions, dovish Fed commentary and a weaker US dollar is telling.

The EIA reported this week that gasoline supplies rose more than expectations as refinery utilization increased. Unleaded Gasoline futures rose slightly, but are still 21.0% below September 2005 highs even as refinery utilization remains below normal as a result of the hurricanes last year, some Gulf of Mexico oil production remains shut-in and fears over future production disruptions persist. According to TradeSports.com, the percent chance of a US and/or Israeli strike on Iran this year has fallen to 20.8% from 36% late last year. I continue to believe the elevated level of gas prices related to crude oil production disruption speculation will further dampen fuel demand over the coming months, sending gas prices back to reasonable levels.

US oil inventories are at 7-year highs. Since December 2003, global oil demand is down 1.19%, while global supplies have increased 5.19%. Moreover, worldwide inventories are poised to begin increasing at an accelerated rate over the next year. I continue to believe oil is priced at extremely elevated levels on fear and record speculation by investment funds, not fundamentals. Escalating violence in the Middle East and the onslaught of hurricane season will likely lead to a major top in oil over the next few months as demand destruction further accelerates. As the fear premium in oil dissipates back to more reasonable levels, global growth slows and supplies continue to rise, crude oil should head meaningfully lower over the intermediate-term.

Natural gas inventories rose slightly less than expectations this week. Supplies are now 25.5% above the 5-year average, near an all-time record high for this time of year, even as some daily Gulf of Mexico production remains shut-in. Natural gas prices have plunged 61.08% since December 2005 highs. At this time last year, 5 tropical storms and 3 hurricanes had already threatened Gulf of Mexico production. There is still little evidence of a pick-up in industrial demand for the commodity despite the collapse in price. Natural gas has likely made an intermediate-term bottom before moving to new cycle lows in November or December.

Gold fell on the week despite a lower US dollar, rising Middle East tensions and dovish Fed commentary. The US Dollar fell slightly on dovish Fed commentary.

Commodity and cyclical stocks underperformed for the week on continuing worries over slower global growth. Despite a 65.9% total return for the S&P 500 since the October 2002 bottom, its forward p/e has contracted relentlessly and now stands at a very reasonable 14.4. The average US stock, as measured by the Value Line Geometric Index(VGY), is down 3.8% this year. The Russell 2000 Index is still up .44% year-to-date, notwithstanding the recent correction. In my opinion, the current pullback is still providing longer-term investors very attractive opportunities in many stocks that have been punished indiscriminately. In my entire investment career, I have never seen the best “growth” companies in the world priced as cheaply as they are now relative to the broad market. By contrast, “value” stocks are quite expensive in many cases. Moreover, the most overvalued economically sensitive and emerging market stocks should continue to underperform over the intermediate-term as the manias for those shares subside. I continue to believe a chain reaction of events has begun that will eventually result in a substantial increase in demand for US stocks.

In my opinion, the market is still factoring in way too much bad news at current levels. Problematic inflation, substantially higher long-term rates, a significant US dollar decline, a “hard-landing” in housing, a plunge in consumer spending and ever higher oil prices appear to be mostly factored into stock prices at this point. I view any one of these as unlikely and the occurrence of all as highly unlikely.

Over the coming months, an end to the Fed rate hikes, lower commodity prices, decelerating inflation readings, lower long-term rates, increased consumer confidence, rising demand for US stocks and the realization that economic growth is only slowing to around average levels should provide the catalysts for another substantial push higher in the major averages through year-end as p/e multiples begin to expand. I still believe the S&P 500 will return a total of around 15% for the year. The ECRI Weekly Leading Index was unchanged this week and is forecasting healthy, but decelerating, US economic activity.

*5-day % Change