Style Outperformer:

Sector Outperformers:

- 1) Gold & Silver +2.72% 2) Utilities +.38% 3) Drugs +.12%

Stocks Rising on Unusual Volume:

Stocks With Unusual Call Option Activity:

- 1) MJN 2) GPRE 3) CDE 4) UCO 5) NLNK

Stocks With Most Positive News Mentions:

- 1) DE 2) AEM 3) NAV 4) ASH 5) MKC

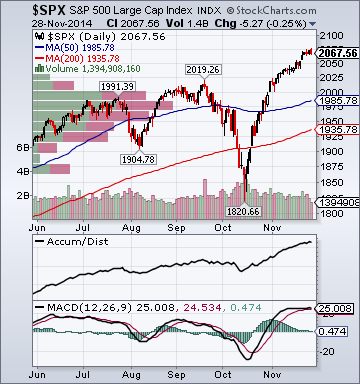

Charts:

Weekend Headlines

Bloomberg:

- Russia’s New Aid Convoy to Rebels Riles Ukraine as Crisis Mounts.

Russia is sending a convoy of more than 100 vehicles with what it

says is humanitarian assistance to rebel-held territory in Ukraine,

drawing accusations from the authorities in Kiev that it’s aiding

separatists. The dispatch marks the eighth such mission since August by

Russia, which says it’s acting to mitigate the humanitarian suffering

caused by the unrest. Ukraine has called the convoys an invasion and

blamed Russia for the toll on civilians. The repeated sight of trucks covered with white tarpaulins

crossing from Russia underscores Ukraine’s loss of control over

parts of the border amid its bloodiest conflict since the Second

World War.

- Russian Warships Enter English Channel Amid Tension Over Ukraine. Russian

warships entered the English Channel amid simmering tensions with the

U.S. and Europe over the conflict in Ukraine. The squadron will conduct

exercises in the area, according to a spokeswoman for Russia’s

Northern Fleet. At least four vessels led by the anti-submarine ship

Severomorsk plan drills in the expanse of water separating England from

continental Europe, the state-run news service RIA Novosti said

yesterday, citing a statement by the Russian Navy. NATO said the foray

isn’t “alarming, it’s normal maritime traffic.” Russia is embroiled in

its most serious confrontation with the U.S. and its European allies

since the collapse of the Soviet Union in 1991.

- ETF Tumbles on Crude’s Plunge as Ukraine Crisis Weighs.

The biggest exchange-traded fund for

Russian equities plunged to a five-year low amid concern a deepening oil

rout will push the world’s largest energy exporter, already beset by

international sanctions, further toward a recession. The Market Vectors Russia ETF (RSX) sank 5.5 percent on Nov. 28 to $19.56, the lowest since April 2009, extending November’s

tumble to 11 percent. The ruble, the worst performing emerging-market currency in 2014, fell for the first time below 50 versus

the dollar, completing a 13 percent slide for the month.

- ECB’s Lautenschlaeger Rebuffs QE as German Opposition Grows. European

Central Bank Executive

Board member Sabine Lautenschlaeger said quantitative easing

isn’t the right policy choice for the euro area currently,

hardening a split among officials over the right response to slowing

inflation. “A consideration of the costs and benefits, and the

opportunities and risks, of a broad purchase program of government bonds

does not give a positive outcome,” Lautenschlaeger, a former

Bundesbank vice president, said at an event in Berlin today. “There are

very few shared competencies in fiscal policy. As long as this is the

case, the ECB’s purchase of government securities is inevitably linked

to a

serious incentive problem.”

- Japan Dairies Losing as Abe’s Weak Yen Boosts Corn Costs. Japan’s dairies and cake lovers just can’t seem to catch a break. A weakening yen is making it more expensive for farmers to import the U.S. corn their cows eat at a time when record crops

have reduced livestock-feeding costs around the world. And while

Japanese milk demand is increasing and prices of some dairy

products are at record highs, domestic production is the lowest

in three decades even as rising output everywhere else creates a

global surplus.

- Xi Says China Will Keep Pushing to Alter Asia Security Landscape.

China will continue its efforts to rewrite Asia’s security architecture

to increase its influence, President Xi Jinping said in a foreign

policy speech over the weekend, according to Xinhua, the state-run news

agency. “We should be fully mindful of the complexity of the evolving international architecture, and we should also

recognize that the growing trend toward a multi-polar world will

not change,” Xi said, according to Xinhua.

- Hong Kong Protesters Clash With Police for Street Control. Hong

Kong police used batons, pepper spray and water hoses in battles with

pro-democracy protesters for control of streets near the government’s

headquarters, as

student leaders pledged to fight on for free elections. Student leaders called this morning for people to head to

the Admiralty district as demonstrators, some with makeshift

shields and head gear, clashed with police along Lung Wo Road

and other junctions near the main protest site in the city.

Traffic was flowing on the roadway as of 9:30 a.m. local time.

- Global Bond Yields Decline to 18-Month Low on Inflation Outlook. A gauge of government bond yields

around the world fell to an 18-month low as tumbling oil prices

push down inflation expectations and economic growth falters. The

average yield among securities in the Bank of America Merrill Lynch

World Sovereign Bond Index dropped to 1.59 percent at the end of last

week, the lowest level since May 2013. Australian 10-year yields dropped

below 3 percent for the first

time in two years.

- Chinese Stocks in Hong Kong Fall Most in Two Weeks on PMI Data.

Chinese stocks trading in Hong Kong fell, sending the benchmark index

to its biggest loss in two weeks, as a drop in the nation’s

manufacturing gauge increased concern economic growth is slowing. Jiangxi

Copper Co., the largest Chinese producer of the metal, plunged 4

percent, while PetroChina Co., the biggest oil company, declined 2.7

percent. Ping An Insurance (Group) Co., China’s second-biggest

insurer, gained 2.2 percent after it said it will raise HK$36.8 billion

($4.75 billion) in a Hong Kong share sale. Airlines rallied in Shanghai

as oil prices extended losses, while lenders climbed after the

government said it will start an insurance system for bank deposits. Hong Kong’s Hang Seng China Enterprises Index (HSCEI) slipped 1.2

percent to 11,003.28 at 10:51 a.m.

- Asia Stocks Fall With U.S. Futures on China, Holiday Data.

Asian stocks fell with U.S. index

futures as a Chinese manufacturing gauge dropped, American holiday

spending slowed and oil tumbled to a five-year low. Malaysia’s ringgit

headed for the biggest two-day retreat since 1998 and precious metals

slumped. The MSCI Asia Pacific Index (MXAP) fell 0.7 percent by 11:42 a.m. in Tokyo, with Standard & Poor’s 500 Index futures dropping 0.4 percent. West

Texas Intermediate crude lost 2.1 percent to $64.74 a barrel, sending

Australian energy stocks toward the biggest three-day loss since the

global financial crisis. Gold

sank as Swiss voters rejected a measure to force the central

bank to hold bullion. The Bloomberg-JPMorgan Asia Dollar Index

fell to a four-year low as the ringgit weakened 1.2 percent.

- Ringgit Set for Biggest Two-Day Drop Since 1998 on Oil Decline.

Malaysia’s ringgit headed for its biggest two-day decline since the

1997-98 Asian financial crisis and led losses in emerging markets on

concern a protracted slide in crude will erode the net oil-exporting

nation’s revenue. The currency weakened 1.3 percent to 3.4250 per dollar as

of 10:38 a.m. in Kuala Lumpur, according to data compiled by

Bloomberg. The ringgit has dropped 2.3 percent in two days, the

sharpest decline since June 1998.

- Commodities Retreat to Five-Year Low as Oil Tumbles With Gold. Commodities fell to the lowest level

in more than five years as oil sank on prospects for a glut,

gold fell after Swiss voters rejected a move to force the

central bank to buy more bullion and data from China confirmed a slowdown in the world’s top user of fuels and metals. The

Bloomberg Commodity Index (BCOM) of 22 raw materials lost as much as

1.3 percent to 111.4738, the lowest level since May 2009, and traded at

111.4777 at 11:03 a.m. in Singapore. West

Texas Intermediate crude fell below $65 a barrel for the first

time since July 2009, while gold, silver and copper declined.

- Miners ‘Covering Their Eyes’ on China’s Commodity Cliff. After

spending $1 trillion since 2002 on projects to feed China’s commodity

boom, the world’s mining companies have a lot riding on their biggest

customer. While commodities may be trading at five-year lows, the heads

of three top miners BHP Billiton Ltd. (BHP), Vale SA (VALE3) and Rio

Tinto Group (RIO) last week all backed China, the world’s second-biggest

economy, to keep buying increasing amounts of their products deep into

the next decade. Not everyone agrees. “The commodity guys are just

too optimistic,” Tao Dong, chief regional economist for Asia excluding

Japan at Credit Suisse Group AG in Hong Kong, said in an interview,

without referring to particular companies.

- BHP(BHP) Sees No Slowdown in Iron-Ore Supply Increase as Prices Slump. BHP

Billiton Ltd. (BHP), the world’s biggest mining company, signaled there

will be no slowdown in the drive by global iron-ore producers to boost

production even as prices slump. “Even the iron-ore price where it is today can induce more volume,” Jimmy

Wilson, BHP’s president of iron ore, said in an interview broadcast

today by Australia’s Nine Network. “If that volume doesn’t come from our

business, it’s going to come from

other businesses around the world and other countries around the

world.”

- OPEC Gusher to Hit Weakest Players, From Wildcatters to Iran.

Saudi Arabia and its OPEC allies’ firm stand against cutting crude

output to slow the plunge in oil prices has set the energy world on a

painful course that will leave the weakest behind, from governments to

U.S. wildcatters. A

grand experiment has begun, one in which the cartel of producing

nations -- sometimes called the central bank of oil -- is leaving the

market to decide who is strongest and how to cut as much as 2 million

barrels a day of surplus supply.

Wall Street Journal:

- Bond Funds Load Up on Cash. Portfolio Managers Gird for Volatility Amid Expected Rate Increase. Large bond funds are holding the most cash since the financial crisis as

portfolio managers brace for potential price swings and unruly trading

ahead of an expected Federal Reserve rate increase in 2015.

- Russian Firms Hire Lobbyists to Fight Senate Sanctions. Energy Company Partly Owned by Friend of Putin Spends at Least $280,000 on Effort. A Russian energy company partly owned by a friend of President

Vladimir Putin has spent at least $280,000 in lobbying fees in the U.S.

aimed in part at opposing a Senate bill that seeks to broaden U.S.

economic sanctions against Russia for invading Ukraine, according to

lobbying-disclosure records.

MarketWatch.com:

- China's slowdown hits iron-ore prices. China's hunger for minerals to build skyscrapers, cars and bridges

produced a decadelong surge in the price and production of key

commodities.

Now, exporting nations are feeling the hit as the China-fueled boom slows. Topping

the list are big commodity players Australia and Brazil, but also

smaller resource-rich countries, such as Guinea, Indonesia and Mongolia,

where minerals make up a disproportionate share of the economy and

employment.

CNBC:

- WHO: Ebola Toll Leaps Higher to Nearly 7,000 in West Africa. (video) The death toll from the worst Ebola outbreak on record has reached

nearly 7,000 in West Africa, the World Health Organization said on

Saturday. The toll of 6,928 dead showed a leap of just over 1,200 since

the WHO released its previous report on Wednesday. The U.N. health

agency did not provide any explanation for the abrupt increase, but the

figures, published on its website, appeared to include previously

unreported deaths. A WHO spokesperson was not immediately available for

comment.

NY Post:

- Terrorists Plotting to Blow Up 5 Planes in Christmas 'Spectacular': Report. Terrorists

are plotting to blow up five passenger planes from European cities as

part of a Christmas “spectacular,” according to a new report. “Everyone is expecting something catastrophic very soon,” a well-placed source told Britain’s Sunday Express.

“We’ve been told that five planes are being targeted in a high-profile

hit before Christmas. They’ve been waiting for the big one.” A source told The Post that London authorities were the first to uncover the threat, which would involve mid-air bombings. “There is a credible threat that they’re concerned about. They’ve known about it for awhile,’’ a source said.

Mainichi:

- Majority in Japan Say Abenomics Didn't Improve Economy. 70% of

Japanese say economy hasn't improved on Abenomics, according to a

Mainichi poll conducted Nov. 29- Nov. 30. Among those supporting the

Cabinet, 50% say economy hasn't improved on Abenomics; 91% of those

opposing the Cabinet say Abenomics hasn't improved the economy.

ABC:

- Australia Govt to Lower Assumed Iron Ore Price to $60/Ton.

Night Trading

- Asian indices are -1.50% to +.25% on average.

- Asia Ex-Japan Investment Grade CDS Index 102.0 +1.0 basis point.

- Asia Pacific Sovereign CDS Index 62.25 -.25 basis point.

- NASDAQ 100 futures -.25%.

Morning Preview Links

Earnings of Note

Company/Estimate

Economic Releases

9:45 am EST

- Final Markit US Manufacturing PMI for November is estimated to rise to 55.0 versus 54.7 in October.

10:00 am EST

- ISM Manufacturing for November is estimated to fall to 58.0 versus 59.0 in October.

- ISM Prices Paid for November is estimated to fall to 52.5 versus 53.5 in October.

Upcoming Splits

Other Potential Market Movers

- The

Fed's Dudley speaking, Eurozone Manufacturing PMI, Reserve Bank of

Australia Decision, Cowen Energy Conference, CSFB Tech Conference and

the (BEAV) investor meeting could

also impact trading today.

BOTTOM LINE: Asian indices are mostly lower, weighed down by commodity and technology shares in the region. I expect US stocks to open modestly lower and to maintian losses into the afternoon. The Portfolio is 50% net long heading into the week.

Week Ahead by Bloomberg.

Wall St. Week Ahead by Reuters.

Stocks to Watch Monday by MarketWatch.

Weekly Economic Calendar by Briefing.com.

BOTTOM LINE: I expect US stocks to finish the week modestly lower on global

growth worries, Russia/Ukraine tensions, rising European/Emerging

Markets debt angst, profit-taking and technical selling. My

intermediate-term trading indicators are giving neutral signals and the

Portfolio is 50% net long heading into the week.

The Weekly Wrap by Briefing.com.

*5-Day Change

Indices

- Russell 2000 1,173.23 +.21%

- S&P 500 High Beta 34.43 +.18%

- Wilshire 5000 21,463.11 +.68%

- Russell 1000 Growth 972.69 +1.32%

- Russell 1000 Value 1,024.03 +.09%

- S&P 500 Consumer Staples 506.50 +2.04%

- Solactive US Cyclical 143.37 -.08%

- Morgan Stanley Technology 1,019.24 +2.67%

- Transports 9,198.20 +1.60%

- Bloomberg European Bank/Financial Services 108.05 +2.43%

- MSCI Emerging Markets 41.73 +1.33%

- HFRX Equity Hedge 1,186.23 +.95%

- HFRX Equity Market Neutral 984.45 +.22%

Sentiment/Internals

- NYSE Cumulative A/D Line 231,815 +1.57%

- Bloomberg New Highs-Lows Index 25 +110

- Bloomberg Crude Oil % Bulls 22.73 -29.74%

- CFTC Oil Net Speculative Position 255,363 n/a

- CFTC Oil Total Open Interest 1,459,175 n/a

- OEX Put/Call 7.80 +622.22%

- ISE Sentiment 74.0 -10.84%

- Volatility(VIX) 13.33 -1.84%

- S&P 500 Implied Correlation 68.53 (new maturities)

- G7 Currency Volatility (VXY) 8.77 +.92%

- Emerging Markets Currency Volatility (EM-VXY) 8.03 +3.35%

- Smart Money Flow Index 17,547.81 +.16%

- ICI Money Mkt Mutual Fund Assets $2.662 Trillion +.32%

- ICI US Equity Weekly Net New Cash Flow -$3.622 Billion

Futures Spot Prices

- Reformulated Gasoline 182.76 -9.88%

- Heating Oil 216.12 -9.67%

- Bloomberg Base Metals Index 191.91 -2.50%

- US No. 1 Heavy Melt Scrap Steel 339.0 USD/Ton -8.9%

- China Iron Ore Spot 71.32 USD/Ton +1.44%

- UBS-Bloomberg Agriculture 1,239.63 -.63%

Economy

- ECRI Weekly Leading Economic Index Growth Rate -2.3% +10 basis points

- Philly Fed ADS Real-Time Business Conditions Index -.1719 +.116%

- S&P 500 Blended Forward 12 Months Mean EPS Estimate 127.58 +.04%

- Citi US Economic Surprise Index 6.10 -13.8 points

- Citi Eurozone Economic Surprise Index -21.50 +14.5 points

- Citi Emerging Markets Economic Surprise Index -.9 +.1 point

- Fed Fund Futures imply 44.0% chance of no change, 56.0% chance of 25 basis point cut on 12/17

- US Dollar Index 88.36 +.09%

- Euro/Yen Carry Return Index 154.20 +1.17%

- Yield Curve 170.0 -11.0 basis points

- 10-Year US Treasury Yield 2.16% -17.0 basis points

- Federal Reserve's Balance Sheet $4.446 Trillion -.15%

- U.S. Sovereign Debt Credit Default Swap 16.47 -1.29%

- Illinois Municipal Debt Credit Default Swap 176.0 +1.82%

- Western Europe Sovereign Debt Credit Default Swap Index 28.11 -8.43%

- Asia Pacific Sovereign Debt Credit Default Swap Index 62.35 -2.41%

- Emerging Markets Sovereign Debt CDS Index 250.11 +2.51%

- Israel Sovereign Debt Credit Default Swap 76.33 -5.57%

- Iraq Sovereign Debt Credit Default Swap 340.72 -3.16%

- Russia Sovereign Debt Credit Default Swap 314.31 +11.07%

- China Blended Corporate Spread Index 323.87 -.50%

- 10-Year TIPS Spread 1.80% -7.0 basis points

- TED Spread 22.0 -1.25 basis points

- 2-Year Swap Spread 20.75 -1.0 basis point

- 3-Month EUR/USD Cross-Currency Basis Swap -11.25 -1.75 basis points

- N. America Investment Grade Credit Default Swap Index 61.47 -3.77%

- European Financial Sector Credit Default Swap Index 59.42 -7.63%

- Emerging Markets Credit Default Swap Index 273.58 +1.35%

- CMBS AAA Super Senior 10-Year Treasury Spread to Swaps 87.0 +1.0 basis point

- M1 Money Supply $2.841 Trillion -.51%

- Commercial Paper Outstanding 1,090.70 unch.

- 4-Week Moving Average of Jobless Claims 294,000 +6,500

- Continuing Claims Unemployment Rate 1.7% -10 basis points

- Average 30-Year Mortgage Rate 3.97% -2 basis points

- Weekly Mortgage Applications 374.50 -4.29%

- Bloomberg Consumer Comfort 40.7 +2.2 points

- Weekly Retail Sales +4.0% +20 basis points

- Nationwide Gas $2.79/gallon -.05/gallon

- Baltic Dry Index 1,187 -10.35%

- China (Export) Containerized Freight Index 1,047.04 -.75%

- Oil Tanker Rate(Arabian Gulf to U.S. Gulf Coast) 32.50 +8.33%

- Rail Freight Carloads 269,373 -1.58%

Best Performing Style

Worst Performing Style

Leading Sectors

Lagging Sectors

Weekly High-Volume Stock Gainers (23)

- FPRX, KIRK, VEEV, EIGI, BWS, NGVC, CVTI, CBPX, POST, ZAYO, BLOX,

PANW, HIBB, BERY, OUTR, AVID, AERI, LORL, LQ, FIVE, CTRN, MTSI and SCAI

Weekly High-Volume Stock Losers (7)

- LQDT, LOCO, DCI, GMCR, ARUN, GME and WAIR

Weekly Charts

ETFs

Stocks

*5-Day Change

Evening Headlines

Bloomberg:

- Russian Recession Risk Seen at Record as Oil Saps Economy. Russia

will sink into recession at a Urals price of $80 a barrel, seven years

after its economy grew 8.5 percent when its chief export oil blend

averaged near $70, according to a Bloomberg survey of analysts. Urals at $80, or about $3 cheaper than its average in the month through November 15, will tip Russia into a contraction,

according to the median estimate of 32 economists. The

probability of a recession in the next 12 months rose to 75

percent, the highest since the first such survey more than two

years ago, according to another poll.

- Abe Tested by Weak Retail Sales as Japan Election Looms: Economy. Japan’s inflation slowed for a third month and retail sales fell more than forecast, showing the economy continues to struggle from a sales-tax

increase as Prime Minister Shinzo Abe heads into an election next month. The Bank of Japan’s key price gauge increased 2.9 percent in

October from a year earlier, equivalent to a 0.9 percent gain when the

effects of April’s tax bump are excluded. Retail sales dropped 1.4

percent from September, more than a 0.5 percent decline forecast in a

Bloomberg News survey.

- Kuroda’s Easing ‘Incomprehensible’ to Ex-BOJ Chief Economist.

Prime Minister Shinzo Abe has tied the Bank of Japan’s hands with a

delay in a sales-tax increase that’s hurt confidence in the nation’s

finances, a former chief economist at the central bank said. Damaged trust in Abe’s pledge to cut the deficit will make

it “extremely difficult” for the BOJ to exit record stimulus

without risking a bond yield surge, Hideo Hayakawa said in an

interview yesterday. More easing would also be tough because

Governor Haruhiko Kuroda effectively has made fiscal improvement

a premise for further monetary stimulus, he said.

- Record China Downgrades Test PBOC as More Defaults Seen. Rating companies say defaults in China will spread as the central

bank’s interest rate cut will do little to stop a wave of maturities

from worsening record debt downgrades. Chinese credit assessors

slashed grades on 83 firms this year, already matching the record number

in all of 2013, according to data compiled by Shenzhen-based China

Investment Securities Co. Companies must repay 2.1 trillion yuan ($342

billion) in the first six months of 2015, the most for any half, data

compiled by Bloomberg show.

- Cameron to Set Out Plan to Cut Migration, Raising EU Exit Threat. David

Cameron will raise the prospect of Britain leaving the European Union

if fellow leaders don’t agree to let him restrict access to welfare

payments for migrants. In a speech in central England today, the

prime minister will demand that Europeans arriving in the U.K. receive

no welfare payments or state housing until they’ve been resident for

four years. He’ll say they shouldn’t receive unemployment benefits and

should be removed from the country if they don’t

find work within six months.

- Commodities Slump to Five-Year Low as Crude Oil Drops on OPEC. Commodities retreated to a five-year

low as crude oil tumbled after OPEC refrained from cutting

output to ease a global glut. Gold and copper also declined. The

Bloomberg Commodity Index (BCOM) of 22 raw materials dropped as much as

1.9 percent to 115.2838, the lowest since July 2009, before trading at

115.29 by 1:26 p.m in Singapore. The index resumed trading today

after the U.S. Thanksgiving holiday yesterday when Brent crude dropped

6.7 percent after a meeting of the Organization of Petroleum Exporting

Countries in Vienna

took no action to relieve the supply glut.

Zero Hedge:

Business Insider:

Evening Recommendations

Night Trading

- Asian equity indices are -.50% to +.50% on average.

- Asia Ex-Japan Investment Grade CDS Index 101.0 -1.5 basis points.

- Asia Pacific Sovereign CDS Index 62.50 unch.

- NASDAQ 100 futures +.28%.

Morning Preview Links

Earnings of Note

Company/Estimate

Economic Releases

Upcoming Splits

Other Potential Market Movers

- The Eurozone CPI report could also impact trading today.

BOTTOM LINE: Asian indices are mostly higher, boosted by consumer and industrial shares in the region. I expect US stocks to open modestly higher and to weaken into the early close, finishing mixed. The Portfolio is 50% net long heading into the day.