- The ISM Manufacturing Index for November came in at 50.8 versus estimates of 50.8 and a reading of 50.9 in October.

- ISM Prices Paid for November rose to 67.5 versus estimates of 65.5 and a reading of 63.0 in October.

- The ISM Manufacturing Index for November came in at 50.8 versus estimates of 50.8 and a reading of 50.9 in October.

- ISM Prices Paid for November rose to 67.5 versus estimates of 65.5 and a reading of 63.0 in October.

Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes

Weekend Headlines

Bloomberg:

- US stocks posted their biggest weekly gain since March after Federal Reserve officials including Chairman Ben S. Bernanke signaled more interest rate cuts may be on the way.

- The US dollar gained the most in almost three years versus the yen and Swiss franc as global stocks rallied and traders boosted bets the Fed will cut borrowing costs a half-percentage point this month.

- The fuel standard for cars and light trucks will increase to 35 miles per gallon by 2020, US lawmakers said last night.

-

- OPEC may not need to increase oil supply when it convenes Dec. 5 to meet the expected advance in energy demand next year,

- Vivendi SA agreed to combine its games unit with Activision Inc.(ATVI), the maker of the “Guitar Hero” video games, in a transaction valued at $18.9 billion. Activision shareholders will receive $27.50 a share.

- Venezuelan President Hugo Chavez’s bid to overhaul the state and possibly stay in power for life will be decided today as his proposal to revamp the nation’s constitution goes to the voters.

- Chavez Threatens to Seize Banks, Media as Vote Nears.

- Online sales last week rose 18% as consumers hunted for bargains on electronics, toys and computers. Internet retail purchases jumped to $4.06 billion in the week ended Nov. 30, led by Yahoo!(YHOO) and Web sites for Target(TGT), Apple(AAPL), Circuit City(CC) and Toys “R” Us, Reston, Virginia-based ComScore(SCOR) said today. Online sales of video games and consoles jumped 170%, toy sales gained 36% and computer hardware rose 21%, ComScore said.

- Dell Inc.(DELL) awarded its advertising account, valued at $4.5 billion over three years, to WPP Group, giving one of the most-notable wins of 2007 to the London advertising company.

-

- China Shipping Container Lines Co., Asia’s second-largest container line, said it will beat its profit forecast after raising rates for shipments from Europe and carrying more cargo from the

NY Times:

- Citigroup(C) is closing in on a CEO and the board appears to be leaning toward an insider.

- The Long and Short of It at Goldman Sachs(GS). An analysis by a Goldman economist deserves its own analysis.

- Inexpensive broadband access has done far more for online video than enable the success of services like YouTube and iTunes. By unchaining video watchers from their TV sets, it has opened the floodgates to a generation of TV producers for whom the Internet is their native medium.

- If the Shoe Fits, Wear It. If Not, Design One That Does.

- Contrarians Make a Case for Gains in the Recent Turmoil. Don’t be too upset by the stock market’s recent decline. It may have been painful, but it’s probably just a stumble by a bull market that still has room to run.

TheStreet.com:

- Sears' Lampert Lashes Out.

MarketWatch.com:

- The last time bond timing newsletters were as optimistic about bonds as they are now was one year ago. That turned out to be a bad time to buy bonds.

- Citi cuts assets of sponsored SIVs by $17 billion. Moody’s warns it may downgrade investment vehicles advised by giant bank.

IBD:

- Treasury, Fed Ride To Rescue Lenders, Subprime Borrowers.

Business Week:

- The Dangerous Wealth of the Ivy League. Higher education is increasingly a tale of two worlds, with elite schools getting richer and buying up all the talent.

- Internships: The Best Places to Start. More than just resume-padding, these summer opportunities have become great tools for students and employers to find that perfect fit.

- S&P’s latest list finds the names with the lowest price-to-earnings growth ratios in each of the 10 S&P sectors.

- Meet This Year’s Tech Pioneers. The World Economic Forum as bestowed the coveted honor on 39 companies, which could become the Googles, a previous winner, of tomorrow.

- Google’s(GOOG) China Chief Sees Internet Boom.

- Media Predictions for 2008.

- Tech Giants Target Older Buyers – and Their Cash.

- Expert Tips Can Point the Way to Big Savings on Your Energy Bill.

CNNMoney.com:

- Why is housing in some cities still booming? The answers may help you navigate your own market.

- Most(and least) cost-effective hybrids.

- Apple Mac hits record 6.81% market share in Net Applications survey.

Reuters:

- RBC Upbeat About US Future, Despite Q4 Impact.

- The Federal Reserve would not hesitate to act to prevent financial strains from damaging the economy and any step it does take are not made to shield investors, a top Fed official said on Friday.

KWWL.com:

-

Finanz und Wirtschaft:

- Royal DSM NV Chief Executive Officer Feike Sijbesma said prices for antibiotics and vitamins have been falling since the end of the third quarter.

El Universal:

- The United Nations and human rights organizations said Venezuelan President Hugo Chavez’s proposed constitution threatens free speech and other civil rights. Analysts Hina Jilani, Ambey Ligabo and Leanddro Despouy, members of the UN’s human-rights council, said a clause allowing removal of

-

Straits Times:

- Hedge funds betting big on US presidential race.

Al Khaleej:

- The United Arab Emirates, the second-largest Arab economy, has no plans to abandon its currency’s peg to the dollar, citing the Gulf state’s central bank governor.

Weekend Recommendations

Barron's:

- Made positive comments on (WU).

- Made negative comments on (PRKR).

Citigroup:

- Reiterated Buy on (PTV), target $35.

- Reiterated Buy on (OI), raised target to $55.

- Rated (CVI) Buy, target $27.

- Maintain Buy on (SNDK), target $65.

- Our take from conference call with ICSC’s Mike Niemira:

Night Trading

Asian indices are -.25% to +1.25% on avg.

S&P 500 futures -.14%.

NASDAQ 100 futures -.33%

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Pre-market Stock Quote/Chart

Before the Bell CNBC Video(bottom right)

Global Commentary

WSJ Intl Markets Performance

Commodity Movers

Top 25 Stories

Top 20 Business Stories

Today in IBD

In Play

Bond Ticker

Economic Preview/Calendar

Daily Stock Events

Macro Calls

Upgrades/Downgrades

Rasmussen Business/Economy Polling

CNBC Guest Schedule

Earnings of Note

Company/Estimate

- (CPWM)/-.80

- (PVH)/1.03

- (BE)/.02

Upcoming Splits

- (DE) 2-for-1

- (LKQX) 2-for-1

- (RSTI) 2-for-1

- (

Economic Data

10:00 am EST

- ISM Manufacturing for November is estimated at 50.7 versus 50.9 in October.

Afternoon

- Total Vehicle Sales for November are estimated to fall to 16.0M versus 16.1M in October.

Other Potential Market Movers

- The Bear Stearns Real Estate Conference, (CDE) shareholders meeting, Bank of America Credit Conference, (LSTR) mid-quarter conference call, (MET) investor’s day, UBS Global Media Conference and (TRT) shareholder’s meeting could also impact trading today.

Click here for the Wall St. Week Ahead by Reuters.

Click here for Stocks in Focus for Monday by MarketWatch.com.

There are a few economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. – ISM Manufacturing, ISM Prices Paid, Total Vehicle Sales

Tues. – Weekly retail sales reports

Wed. – Weekly MBA Mortgage Applications report, weekly EIA energy inventory report, Challenger Job Cuts, ADP Employment Change, Final 3Q Non-farm Productivity, Final 3Q Unit Labor Costs, Factory Orders, ISM Non-Manufacturing

Thur. – Initial Jobless Claims, ICSC Chain Store Sales

Fri. – Change in Non-Farm Payrolls, Unemployment Rate, Average Hourly Earnings,

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. – Phillips-Van Heusen(PVH), Cost Plus(CPWM), BearingPoint(BE)

Tues. – Autozone(AZO),

Wed. – DSW Inc.(DSW),

Thur. – Korn/Ferry(KFI), UTi Worldwide(UTIW), National Semi(NSM), Synopsys(SNPS), Krispy Kreme(KKD), Quanex(NX, Toll Brothers(TOL), Pathmark Stores(PTMK)

Fri. – Kellwood(KWD)

Other events that have market-moving potential this week include:

Mon. – Fed’s Rosengren speaking, Fed’s Yellen speaking, (SLG) analyst meeting, (GKK) analyst meeting, Bear Stearns Real Estate Conference, Banc of America Credit Conference, (LSTR) mid-quarter conference call, (MET) Investor’s Day, UBS Global Media Conference

Tue. – (NOK) capital market day, (TXRH) analyst meeting, (ARBA) financial analyst day, (MDU) analyst meeting, (IFX) analyst meeting, BMO Healthcare Conference, Banc of America Credit Conference, Citigroup Basic Materials Conference, Bear Stearns Real Estate Conference, UBS Global Media Conference

Wed. – BOE Policy Meeting, (FTE) investor day, (XEL) investor meeting, (ATO) analyst meeting, (OREX) analyst luncheon, (BMY) investment meeting, BMO Healthcare Conference, Wachovia Global Real Estate Conference, UBS Global Media Conference, Lehman Brothers Global Tech Conference, ThinkEquity Alternative Energy Forum, Citigroup Basic Materials Conference, (XLNX) mid-quarter update

Thur. – ECB Policy Meeting, (PHG) analysts’ day, (FE) analyst meeting, (PRS) analyst meeting, (PH) investor day, (KNXA) analyst meeting, (SCUR) investor day, (SVVS) analyst meeting, (SFI) investor day, BOE Policy Meeting, Deutsche Bank Healthcare Tech Day, Stifel, Nicolaus Financial Institutions Conference, CIBC Communications Software 1-on-1 Conference, Citigroup ePayments Day, Lehman Brothers Tech Conference, ThinkEquity Alternative Energy Forum

Fri. – (SON) analysts’ meeting, (HSC) analysts conference, (RRGB) analyst meeting, Lehman Brothers Tech Conference

Indices

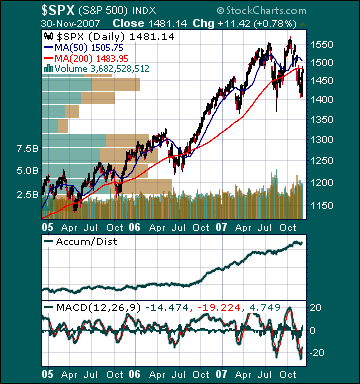

S&P 500 1,481.14 +2.81%

DJIA 13,371.72 +3.01%

NASDAQ 2,660.96 +2.48%

Russell 2000 767.77 +1.69%

Wilshire 5000 14,869.56 +2.80%

Russell 1000 Growth 614.82 +2.77%

Russell 1000 Value 805.77 +3.02%

Morgan Stanley Consumer 754.30 +2.22%

Morgan Stanley Cyclical 992.37 +3.94%

Morgan Stanley Technology 616.45 +1.94%

Transports 4,661.29 +4.72%

Utilities 532.25 +1.62%

MSCI Emerging Markets 153.66 +4.55%

Sentiment/Internals

NYSE Cumulative A/D Line 62,651 +4.65%

Bloomberg New Highs-Lows Index -293 -1,076.67%

Bloomberg Crude Oil % Bulls 32.14 -14.29%

CFTC Oil Large Speculative Longs 230,982 -2.14%

Total Put/Call 1.07 +27.4%

NYSE Arms .83 +112.82%

Volatility(VIX) 22.87 -10.70%

ISE Sentiment 96.0 -34.69%

AAII % Bulls 28.57 +11.69%

AAII % Bears 56.12 +6.47%

Futures Spot Prices

Crude Oil 88.71 -9.65%

Reformulated Gasoline 223.06 -9.51%

Natural Gas 7.30 -8.85%

Heating Oil 251.50 -7.37%

Gold 789.10 -5.13%

Base Metals 224.93 +2.81%

Copper 318.45 +5.12%

Economy

10-year US Treasury Yield 3.94% -6 basis points

4-Wk MA of Jobless Claims 335,300 +1.8%

Average 30-year Mortgage Rate 6.10% -10 basis points

Weekly Mortgage Applications 652.50 -4.28%

Weekly Retail Sales +2.4%

Nationwide Gas $3.08/gallon unch.

US Heating Demand Next 7 Days 5% above normal

ECRI Weekly Leading Economic Index 138.10 -.72%

US Dollar Index 76.15 +1.46%

CRB Index 339.84 -4.08%

Best Performing Style

Mid-cap Growth +3.49%

Worst Performing Style

Small-cap Value +.86%

Leading Sectors

Alternative Energy +7.09%

Construction +6.39%

Steel +5.96%

Biotech +5.38%

Banks +5.31%

Semis +.66%

Software -.03%

Energy -.14%

Gold -3.41%

Oil Service -5.61%