ECRI Weekly Leading Index 131.50 -.30%

Wholesale Inventories for June rose 1.1% versus estimates of a .6% increase and a rise of 1.4% in May. Consumer spending, that cooled by the most in almost three years during the month, helped give companies the chance to replenish inventories that had been drained to record lows earlier this year, Bloomberg reported. "We expect a general recovery in inventories relative to sales in the wholesale sector to provide solid support for GDP growth through the remainder of 2004," said Michael Englund, chief economist at Action Economics. Wholesalers had enough supply to last 1.15 months at the current sales pace, up from the record low of 1.12 months in April.

Preliminary 2Q Non-farm Productivity rose 2.9% versus estimates of a 2.0% rise and a 3.7% increase in 1Q. Preliminary 2Q Unit Labor Costs rose 1.9% versus estimates of a 2.0% increase and a .3% rise in 1Q. The gain in productivity suggests that companies have become efficient enough to hold down payrolls until the economy rebounds form a second-quarter lull, economists said. The second-quarter rise in productivity is in line with the average annual increase of 3% since 1996. By contrast, productivity rose an average 1.5% a year in the previous two decades, Bloomberg reported. The number "is still quite healthy, productivity is incredibly strong," Douglas Porter, senior economist at BMO Nesbitt Burns said. Labor costs, while increasing, are still at moderate levels, Bloomberg reported.

Federal Reserve policy makers raised the benchmark U.S. interest rate a quarter-point to 1.5% and restated a pledge to lift borrowing costs at a "measured" pace to suppress inflation without choking off growth, Bloomberg said. "Output growth has moderated and the pace of improvement in labor market conditions has slowed recently, however the economy appears poised to resume a stronger pace of expansion going forward," the Fed's rate-setting Open Market Committee said. The year's second rate increase was overshadowed by the decision to keep the "measured" pace language, which some investors expected the Fed to abandon, Bloomberg said.

The Import Price Index for July rose .2% versus estimates of a .4% rise and a .1% fall in June. The recent acceleration in core prices "has probably just about run its course," Joshua Shapiro, chief U.S. economist at MFR Inc. said. Imports account for about 15% of all goods and services bought in the U.S., Bloomberg reported.

Advance Retail Sales for July rose .7% versus estimates of a 1.2% increase and an upwardly revised .5% decline in June. Retail Sales Less Autos for July rose .2% versus estimates of a .4% increase and an upwardly revised .3% rise in June. Retailers said same-store sales rose in July and Wal-Mart boosted its annual earnings forecast, Bloomberg reported. "The slowing that was apparent in earlier months likely overstated the weakness in consumer spending," said Richard DeKaser, chief economist at National City. Consumer spending is now forecast to rise at a 3.2% annual rate in the third quarter, based on the median estimate of 48 economists polled by Bloomberg.

Initial Jobless Claims fell to 333K last week versus estimates of 340K and 337K the prior week. Continuing Claims were 2896K versus estimates of 2895K and 2901K prior. The figures on jobless claims "suggest that the recent weakness in payroll employment should be transitory," Steven Wood, president of Insight Economics said. Moreover, the four-week moving average of continuing claims fell to 2.88M, the lowest since the week that ended June 2, 2001.

Business Inventories rose .9% versus estimates of a .6% rise and an increase of .7% in May. The inventory-sales ratio rose to 1.31 months, boosted by more autos on dealer lots. From March through May, the ratio was at a record low of 1.3 months, Bloomberg said. "Companies are continuing to rebuild their inventories but are doing so basically in line with growing sales," said Steven Wood, chief economist at Insight Economics. The increase in stockpiles will add more to economic growth in the second quarter than the government initially reported, economists said.

The Producer Price Index for July rose .1% versus estimates of a .3% rise and a decrease of .3% in June. PPI Ex Food & Energy for July rose .1% versus estimates of a .1% increase and a .2% rise in June. Prices rose less than forecast in July, restrained by cheaper cars and the biggest drop in the cost of food in more than two years, Bloomberg reported. Moreover, the cost of dairy products fell 6.2%, the biggest decline since April 1999, Bloomberg said. Smaller increases in core prices support the central bankers' view and may make it possible for them to continue to raise the target benchmark interest rate at a "measured" pace.

The Preliminary Univ. of Mich. Consumer Confidence reading for August came in at 94.0 versus estimates of 97.2 and a reading of 96.7 in July. The Current Conditions Index, based on perceptions of consumers' financial situation and whether it's a good time to make big purchases, rose to 108.4 in August from 105.2 last month, Market News said. Sentiment was likely negatively affected by the many reports of terror plots across the globe, rather than by weaker payroll numbers and rising oil prices. Stephen Gallagher, chief economist at Societe Generale in New York, said the index is influenced more by the unemployment rate, which fell, than by job creation, Bloomberg reported. Furthermore, the average all-grades price of a gallon of gasoline has fallen since reaching a record in late May, Bloomberg said.

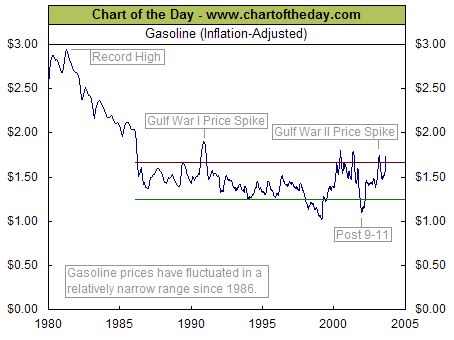

Bottom Line: Overall, the economic data last week were mixed. Inventories are rising slightly, which could be a positive or negative depending on final demand in future months. However, the inventory rebuilding will help boost GDP growth this quarter. Payroll increases will likely remain underwhelming until demand reaccelerates in the fourth quarter and productivity drops. Unit labor costs, the largest component of inflation, remain at relatively subdued levels. In my opinion, the Fed made a mistake by leaving the "measured" language in their policy statement without qualifying it. While I agree with the Fed that the economy will reaccelerate, current weakness resulting from anti-business political rhetoric and terrorism fears, will likely restrain growth through the election in November. With interest rates plunging, most commodity prices dropping and recent inflation readings decelerating, I believe the Fed should wait at least until the November 10th meeting to hike rates further. However, at this point it appears a September rate increase is likely. Retail Sales for June were revised higher and July saw a rebound from June's temporarily depressed levels. The July reading for the Current Conditions component of Univ. of Mich. Consumer Sentiment Index bodes well for retail sales during the third quarter. The fall in the overall index was a direct result of the multiple terror warnings and reports during the month. Negative political rhetoric and the media's intense focus on higher oil prices and slower payroll growth also contributed to the decline. There were very few stories on the recent deceleration in inflation readings and the fall in the Unemployment Rate. The Unemployment Rate is now back to levels seen right before the 9/11 terrorist attacks. Finally, the CRB Index(a broad-based measure of commodity prices) is now down almost 6% from its highs set in March. Oil comprises less than 5% of inflation, yet every story related to inflation or commodities revolves around it being at all-time highs. Crude oil and gasoline would have to rise by 70% each to just reach the inflation-adjusted levels seen in the late 70's/early 80's. Rising energy prices and decelerating payroll growth are definitely not good for the economy, but the media's intense focus on everything negative is currently far more destructive to economic growth, in my opinion.