S&P 500 1,151.74 -.89%

DJIA 10,151.13 -.89%

NASDAQ 1,927.44 -1.20%

Russell 2000 587.66 -1.47%

DJ Wilshire 5000 11,349.22 -.90%

S&P Barra Growth 557.33 -.88%

S&P Barra Value 590.06 -.91%

Morgan Stanley Consumer 571.95 -.91%

Morgan Stanley Cyclical 701.80 -1.58%

Morgan Stanley Technology 438.66 -1.15%

Transports 3,404.55 -1.91%

Utilities 365.61 -1.07%

Put/Call .75 -5.06%

NYSE Arms 1.78 +169.42%

Volatility(VIX) 14.91 +1.98%

ISE Sentiment 161.00 +25.78%

US Dollar 83.93 +.13%

CRB 309.78 +.36%

Futures Spot Prices

Crude Oil 54.36 -.38%

Unleaded Gasoline 162.70 -1.45%

Natural Gas 7.15 -.04%

Heating Oil 151.38 -.28%

Gold 438.60 +.64%

Base Metals 124.60 -.42%

Copper 145.70 -1.82%

10-year US Treasury Yield 4.26% +.42%

Leading Sectors

Gaming +2.57%

Broadcasting -.18%

Retail -.29%

Lagging Sectors

Tobacco -3.34%

Computer Hardware -3.64%

Steel -4.53%

Evening Review

Detailed Market Summary

Market Gauges

Daily ETF Performance

Style Performance

Market Wrap CNBC Video(bottom right)

S&P 500 Gallery View

Timely Economic Charts

PM Market Call

After-hours Movers

Real-time/After-hours Stock Quote

In Play

Afternoon Recommendations

Goldman Sachs:

- Reiterated Outperform on GILD and LVS.

Afternoon/Evening Headlines

Bloomberg:

- Amazon.com reported first-quarter net income fell to $78 million, hurt by new discounts on shipping and increased development costs.

Financial Times:

- The benefits of countries opening their borders to foreign service-providers will exceed any reduction in jobs, citing the OECD.

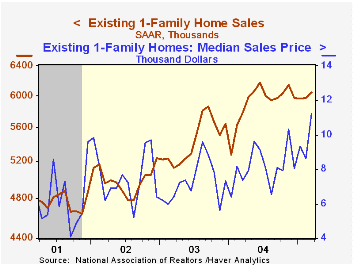

BOTTOM LINE: US stocks finished lower today on continuing worries over slowing global growth. The Portfolio finished slightly lower on losses in my Internet and Networking longs. I did not trade in the afternoon, thus leaving the Portfolio 75% net long. The tone of the market deteriorated into the afternoon as the advance/decline finished at its daily lows, almost every sector fell and volume was average. Measures of investor anxiety were mixed. Overall, today’s market action was negative, considering strong home sales, a rising US dollar, falling energy prices, good earnings reports and stable interest rates. Choppiness will likely continue until oil breaks below $50/bbl. or the Fed makes less hawkish comments. The fact that the Homebuilders declined today even with home sales substantially exceeding expectations, building costs declining, mortgage rates dropping and weather improving is a negative and illustrates the overly pessimistic environment that still dominates trading.