Earnings of Note

Company/Estimate

AMAT/.25

BJ/.37

BGP/.06

HD/.64

EL/.32

DKS/.33

DE/1.50

JCP/.23

TJX/.24

SPLS/.22

SKS/-.12

WIND/-.02

Splits

RNT 3-for-2

WIRE 3-for-2

Economic Data

Consumer Price Index for July estimated +.2% versus +.3% in June.

CPI Ex Food & Energy for July estimated +.2% versus +.1% in June.

Housing Starts for July estimated at 1895K versus 1802K in June.

Building Permits for July estimated at 1950K versus 1945K in June.

Industrial Production for July estimated +.5% versus -.3% in June.

Capacity Utilization for July estimated at 77.5% versus 77.2% in June.

Recommendations

Goldman Sachs reiterated Underperform on SGP. Goldman reiterated Outperform on BAX.

Late-Night News

Asian indices are quietly higher on a decline in energy prices and a rally in U.S. shares. OAO Yukos Oil, Russia's biggest oil exporter, posted a first-half loss of $2.7 billion, compared with a profit of $1.3 billion for the same period in 2003, the Financial Times reported. A crackdown by Pakistani security forces on Osama bin Laden's al-Qaeda terrorist network is forcing members of the group to flee the country, Agence France-Presse said. Microsoft may sign a three-year deal with the U.K. government that offers enhanced services and support to its basic software packages, the Financial Times reported. Former employees of MediaOne that hold AT&T Wireless stock options may sue Cingular for forcing them to exercise the options when Cingular completes its acquisition of AT&T Wireless, USA Today reported. China bank may raise interest rates as early as Oct. 1 as the government switches to market forces from administrative measures to cool the economy, the Securities Daily said. President Bush and Senator Kerry should concentrate on fighting terrorism if they want to help the U.S. economy, according to a National Association for Business Economics survey of its members.

Late-Night Trading

Asian Indices are unch. to +.50% on average.

S&P 500 indicated -.08%.

NASDAQ 100 indicated -.09%

BOTTOM LINE: I expect U.S. equities to open modestly higher on better-than-expected economic data and better earnings reports. The Portfolio is 75% net long heading into tomorrow.

Tuesday, August 17, 2004

Monday, August 16, 2004

Monday Close

S&P 500 1,079.34 +1.37%

NASDAQ 1,782.84 +1.46%

Leading Sectors

Airlines +5.56%

I-Banks +3.33%

Biotech +3.15%

Lagging Sectors

Hospitals +.33%

Foods +.23%

Restaurants +.18%

Other

Crude Oil 45.53 -.35%

Natural Gas 5.38 +.13%

Gold 404.90 -.07%

Base Metals 111.70 +.57%

U.S. Dollar 87.96 +.07%

10-Yr. T-note Yield 4.26% +.78%

VIX 17.57 -2.28%

Put/Call .84 -20.0%

NYSE Arms .37 -69.17%

After-hours Movers

PIR +5.85% after it was reported that Berkshire Hathaway held 8 million shares of its stock.

MANT +15.04% after beating 2Q sales estimates and raising 3Q outlook.

AMT -5.41% after announcing it is seeking to raise $300 million through an institutional placement of convertible notes.

Recommendations

Goldman Sachs reiterated Outperform on KO and KRB.

After-hours News

U.S. stocks finished higher today as the Venezuelan political situation calmed, opening Olympic ceremonies went smoothly and energy prices fell. After the close, Krispy Kreme Doughnuts COO John Tate will resign, the Wall Street Journal reported. Google asked the SEC to declare its IPO effective tomorrow at 4 p.m., CNBC reported. Senate Intelligence Committee Chairman Republican Pat Roberts said he would introduce a bill this week to create the position of U.S. intelligence director as three former heads of the CIA endorsed the idea, Bloomberg reported. The Bush administration informed the European Union it wants to scrap a 12-year-old agreement that let EU members subsidize Airbus SAS, the world's biggest plan manufacturer, Bloomberg reported.

BOTTOM LINE: The Portfolio finished slightly higher today and I covered a few of my Russian ADR shorts in the afternoon, leaving the Portfolio 75% net long. Today's market action appeared to be the result of oversold technical conditions and short covering. However, a better-than-expected CPI reading, a continuing drop in energy prices and better earnings reports could spur further gains.

NASDAQ 1,782.84 +1.46%

Leading Sectors

Airlines +5.56%

I-Banks +3.33%

Biotech +3.15%

Lagging Sectors

Hospitals +.33%

Foods +.23%

Restaurants +.18%

Other

Crude Oil 45.53 -.35%

Natural Gas 5.38 +.13%

Gold 404.90 -.07%

Base Metals 111.70 +.57%

U.S. Dollar 87.96 +.07%

10-Yr. T-note Yield 4.26% +.78%

VIX 17.57 -2.28%

Put/Call .84 -20.0%

NYSE Arms .37 -69.17%

After-hours Movers

PIR +5.85% after it was reported that Berkshire Hathaway held 8 million shares of its stock.

MANT +15.04% after beating 2Q sales estimates and raising 3Q outlook.

AMT -5.41% after announcing it is seeking to raise $300 million through an institutional placement of convertible notes.

Recommendations

Goldman Sachs reiterated Outperform on KO and KRB.

After-hours News

U.S. stocks finished higher today as the Venezuelan political situation calmed, opening Olympic ceremonies went smoothly and energy prices fell. After the close, Krispy Kreme Doughnuts COO John Tate will resign, the Wall Street Journal reported. Google asked the SEC to declare its IPO effective tomorrow at 4 p.m., CNBC reported. Senate Intelligence Committee Chairman Republican Pat Roberts said he would introduce a bill this week to create the position of U.S. intelligence director as three former heads of the CIA endorsed the idea, Bloomberg reported. The Bush administration informed the European Union it wants to scrap a 12-year-old agreement that let EU members subsidize Airbus SAS, the world's biggest plan manufacturer, Bloomberg reported.

BOTTOM LINE: The Portfolio finished slightly higher today and I covered a few of my Russian ADR shorts in the afternoon, leaving the Portfolio 75% net long. Today's market action appeared to be the result of oversold technical conditions and short covering. However, a better-than-expected CPI reading, a continuing drop in energy prices and better earnings reports could spur further gains.

Mid-day Update

S&P 500 1,076.38 +1.12%

NASDAQ 1,780.74 +1.34%

Leading Sectors

Airlines +4.60%

Biotech +2.70%

I-Banks +2.68%

Lagging Sectors

Restaurants +.42%

Hospitals +.14%

Foods -.29%

Other

Crude Oil 45.90 -.28%

Natural Gas 5.43 -1.95%

Gold 404.50 +.82%

Base Metals 112.48 +1.27%

U.S. Dollar 88.07 +.19%

10-Yr. T-note Yield 4.28% +1.24%

VIX 17.77 -1.17%

Put/Call .87 -17.14%

NYSE Arms .40 -66.67%

Market Movers

PRV +39.2% after saying LPNT agreed to buy it for $1.13 billion in cash and stock, LPNT -17.3%.

KMRT +13.8% on better-than-expected 2Q results.

LOW +6.1% after missing 2Q estimates and raising 3Q outlook.

SYY -7.8% after missing 4Q estimates and BB&T downgrade to Hold.

Economic Data

Empire Manufacturing for August came in at 12.57 versus estimates of 32.30 and a reading of 35.75 in July.

Recommendations

BRL rated Buy at Bank of America, target $46. JTX rated Buy at Bank of America, target $21. BLT rated Overweight at JP Morgan. BRO raised to Overweight at JP Morgan, target $50. EL raised to Buy at Oppenheimer, target $51. IPXL rated Buy at Bank of America, target $17. LPNT cut to Underweight at JP Morgan. Goldman Sachs raised KSS to Outperform. Goldman reiterated Outperform on AET, AMGN, KRB, FS, IGT. Goldman rated HEP Outperform. Citi SmithBarney downgraded LF to Sell, target $17. Citi upgraded DOW to Buy, target $46. Citi upgraded LYO to Buy, target $21. Citi reiterated Buy on NCX, target $30.37. Citi reiterated Buy on HAS, target $24. Citi upgraded MAT to Buy, target $21. Citi reiterated Buy on HCA, target $48. Citi reiterated Buy on SBUX, target $54.

Mid-day News

U.S. stocks are higher mid-day on short-covering and bargain-hunting after recent weakness. Micrel Inc., a Silicon Valley semiconductor maker, denied accusations of improper conduct made by an IRS auditor, the NY Times said. Gateway Inc. said CompUSA will begin selling its desktop computers this week, Bloomberg said. Panasonic and other high-definition tv makers are hoping the Olympics gives consumers a reason to try digital TV, the LA Times reported. Lowe's said second-quarter earnings rose 18%, helped by new stores in metro areas and record U.S. home sales, Bloomberg reported. Venezuelan President Chavez overcame a referendum to remove him from office two years before his term expires, Bloomberg said. Crude oil futures fell after Chavez's victory eased concerns that shipments from the country would be disrupted, Bloomberg said. The first two days of full competition in Athens were marked by near-empty stadiums in many sports, Bloomberg reported. International investors purchased a net $71.8 billion of U.S. Treasuries, stocks, corporate bonds and other securities in June, up from $65.2 billion in May, Bloomberg reported. The $53 billion U.S. missile defense shield being developed by Boeing, Lockheed Martin and Northrop Grumman may be derailed by a John Kerry presidency, Bloomberg said. Bank of America and Wachovia are among the banks doing business in Florida that stand to benefit from a rise in deposits and loans following Hurricane Charley, Bloomberg reported. Goldman Sachs economists call higher oil prices "excuses" in explaining the deceleration in U.S. consumer spending this year as the real culprit is the withdrawal of fiscal and monetary stimulus from the economy, Bloomberg reported.

BOTTOM LINE: The Portfolio is slightly higher mid-day as strength in my retail and internet longs is offsetting losses in my steel and Russian ADR shorts. I added a few technology longs this morning, bringing the Portfolio's market exposure to 50% net long. One of my new longs is CYMI and I am using a stop-loss of $24.30 on the position. The tone of the market is better today, but it appears to be mostly short-covering and a lack of sellers. However, the rally could gain legs on a further drop in energy prices and better earnings reports over the next couple of days. The odds of a major terrorist attack this year are diminishing with each passing day.

NASDAQ 1,780.74 +1.34%

Leading Sectors

Airlines +4.60%

Biotech +2.70%

I-Banks +2.68%

Lagging Sectors

Restaurants +.42%

Hospitals +.14%

Foods -.29%

Other

Crude Oil 45.90 -.28%

Natural Gas 5.43 -1.95%

Gold 404.50 +.82%

Base Metals 112.48 +1.27%

U.S. Dollar 88.07 +.19%

10-Yr. T-note Yield 4.28% +1.24%

VIX 17.77 -1.17%

Put/Call .87 -17.14%

NYSE Arms .40 -66.67%

Market Movers

PRV +39.2% after saying LPNT agreed to buy it for $1.13 billion in cash and stock, LPNT -17.3%.

KMRT +13.8% on better-than-expected 2Q results.

LOW +6.1% after missing 2Q estimates and raising 3Q outlook.

SYY -7.8% after missing 4Q estimates and BB&T downgrade to Hold.

Economic Data

Empire Manufacturing for August came in at 12.57 versus estimates of 32.30 and a reading of 35.75 in July.

Recommendations

BRL rated Buy at Bank of America, target $46. JTX rated Buy at Bank of America, target $21. BLT rated Overweight at JP Morgan. BRO raised to Overweight at JP Morgan, target $50. EL raised to Buy at Oppenheimer, target $51. IPXL rated Buy at Bank of America, target $17. LPNT cut to Underweight at JP Morgan. Goldman Sachs raised KSS to Outperform. Goldman reiterated Outperform on AET, AMGN, KRB, FS, IGT. Goldman rated HEP Outperform. Citi SmithBarney downgraded LF to Sell, target $17. Citi upgraded DOW to Buy, target $46. Citi upgraded LYO to Buy, target $21. Citi reiterated Buy on NCX, target $30.37. Citi reiterated Buy on HAS, target $24. Citi upgraded MAT to Buy, target $21. Citi reiterated Buy on HCA, target $48. Citi reiterated Buy on SBUX, target $54.

Mid-day News

U.S. stocks are higher mid-day on short-covering and bargain-hunting after recent weakness. Micrel Inc., a Silicon Valley semiconductor maker, denied accusations of improper conduct made by an IRS auditor, the NY Times said. Gateway Inc. said CompUSA will begin selling its desktop computers this week, Bloomberg said. Panasonic and other high-definition tv makers are hoping the Olympics gives consumers a reason to try digital TV, the LA Times reported. Lowe's said second-quarter earnings rose 18%, helped by new stores in metro areas and record U.S. home sales, Bloomberg reported. Venezuelan President Chavez overcame a referendum to remove him from office two years before his term expires, Bloomberg said. Crude oil futures fell after Chavez's victory eased concerns that shipments from the country would be disrupted, Bloomberg said. The first two days of full competition in Athens were marked by near-empty stadiums in many sports, Bloomberg reported. International investors purchased a net $71.8 billion of U.S. Treasuries, stocks, corporate bonds and other securities in June, up from $65.2 billion in May, Bloomberg reported. The $53 billion U.S. missile defense shield being developed by Boeing, Lockheed Martin and Northrop Grumman may be derailed by a John Kerry presidency, Bloomberg said. Bank of America and Wachovia are among the banks doing business in Florida that stand to benefit from a rise in deposits and loans following Hurricane Charley, Bloomberg reported. Goldman Sachs economists call higher oil prices "excuses" in explaining the deceleration in U.S. consumer spending this year as the real culprit is the withdrawal of fiscal and monetary stimulus from the economy, Bloomberg reported.

BOTTOM LINE: The Portfolio is slightly higher mid-day as strength in my retail and internet longs is offsetting losses in my steel and Russian ADR shorts. I added a few technology longs this morning, bringing the Portfolio's market exposure to 50% net long. One of my new longs is CYMI and I am using a stop-loss of $24.30 on the position. The tone of the market is better today, but it appears to be mostly short-covering and a lack of sellers. However, the rally could gain legs on a further drop in energy prices and better earnings reports over the next couple of days. The odds of a major terrorist attack this year are diminishing with each passing day.

Monday Watch

Earnings of Note

Company/Estimate

CEN/.19

KMRT/.14

LBTYA/-.24

LOW/.90

SYY/.45

Splits

QCOM 2-for-1

Economic Data

Empire Manufacturing for August estimated at 32.3 versus 36.54 in July.

NAHB Housing Market Index for August estimated at 66 versus 67 in July.

Weekend Recommendations

Barron's had positive comments on TWX, EMC, EK and negative comments on HPQ. Goldman Sachs reiterated Outperform on MRVL, EBAY and ALL. Bloomberg has a positive column by Caroline Baum on the exaggerated death of the U.S. consumer.

Weekend News

China sold 15.8 million cell phones in the second quarter, down 23 percent from a year earlier, Shanghai Daily said. The U.S. bipartisan Commission for Presidential Debates named the moderators for four events it will hold in late September and early October, the NY Times reported. The commission said Jim Lehrer of PBS, Bob Schieffer of CBS and Charles Gibson of ABC will each moderate one of the three presidential debates. PBS's Gwen Ifill will moderate the vice-presidential debate. Al-Qaeda is regrouping in Pakistan and planning attacks in the U.S. with a "motley collection of old hands and recent recruits," the Washington Post reported. President Bush on Monday will announce plans to transfer 70,000 to 100,000 troops from Europe and Asia as the U.S. military shifts its focus to the war on terrorism from the cold war, the Washington Post said. OAO Yukos Oil Co.'s share price is being manipulated by senior Kremlin officials for their own benefit, the Business newspaper reported. Iraq's Prime Minister Ayad Allawi ordered troops from the country's newly formed army to lead an attack against Shiite Muslim militia in Najaf, the Washington Post reported. Lawyers for Golan Cipel, the Israeli who was given $110,000-a-year job by New Jersey Democratic Governor James McGreevey, said Cibel is heterosexual and didn't consent to any intimate contact with McGreevey, the NY Times said. New Jersey residents' approval of Governor McGreevey actually rose 2% to 45% after a recent flurry of scandalous allegations, according to the Star-Ledger. OAO Yukos Oil may "very likely" file for bankruptcy in the next few days unless Russia eases the pressure it's been applying, the Financial Times said. Posco's record earnings may not last until the first half of next year as the Korean steelmaker faces a number of threats such as higher oil prices, the Seoul Economic Daily reported. U.S. gas prices fell about 4.9 cents in the past three weeks, the AP reported, citing the Lundberg Survey of about 8,000 gas stations. Electronic Arts may be interested in buying U.K. publisher Eidos Plc as part of its European expansion, the Financial Times reported. Caterpillar workers rejected a six-year contract proposal, the AP reported. Allstate Corp., State Farm Mutual and other insurers may lose about $5 billion from Hurricane Charley, less than initially forecast, Bloomberg said. A weakened Hurricane Charley, the most powerful storm to hit the U.S. in 12 years, left Florida with deaths and damage estimated in the billions of dollars as it headed for the South Carolina coast this morning, Bloomberg reported. Crude oil prices may fall to $30/bbl. next year as concerns about supply disruptions in Iraq, Russia and Venezuela ease and OPEC boosts output, the group's President said. China will provide low-interest loans to cable companies to convert 100 million urban households to digital television by 2008, Bloomberg said. Crude oil futures in New York rose to a record on concern violence may spread in Venezuela, the fourth-largest exporter to the U.S., as the nation votes in a referendum that could remove President Chavez from office, Bloomberg reported.

Late-Night Trading

Asian indices are lower, -1.0% to -.50% on average.

S&P 500 indicated -.26%.

NASDAQ 100 indicated -.27%.

BOTTOM LINE: I expect U.S. stocks to open modestly lower in the morning on worries over Venezuelan political unrest and terrorism fears. However, equities will likely rally higher by day's end on short-covering and bargain-hunting. The Portfolio is 25% net long heading into tomorrow.

Company/Estimate

CEN/.19

KMRT/.14

LBTYA/-.24

LOW/.90

SYY/.45

Splits

QCOM 2-for-1

Economic Data

Empire Manufacturing for August estimated at 32.3 versus 36.54 in July.

NAHB Housing Market Index for August estimated at 66 versus 67 in July.

Weekend Recommendations

Barron's had positive comments on TWX, EMC, EK and negative comments on HPQ. Goldman Sachs reiterated Outperform on MRVL, EBAY and ALL. Bloomberg has a positive column by Caroline Baum on the exaggerated death of the U.S. consumer.

Weekend News

China sold 15.8 million cell phones in the second quarter, down 23 percent from a year earlier, Shanghai Daily said. The U.S. bipartisan Commission for Presidential Debates named the moderators for four events it will hold in late September and early October, the NY Times reported. The commission said Jim Lehrer of PBS, Bob Schieffer of CBS and Charles Gibson of ABC will each moderate one of the three presidential debates. PBS's Gwen Ifill will moderate the vice-presidential debate. Al-Qaeda is regrouping in Pakistan and planning attacks in the U.S. with a "motley collection of old hands and recent recruits," the Washington Post reported. President Bush on Monday will announce plans to transfer 70,000 to 100,000 troops from Europe and Asia as the U.S. military shifts its focus to the war on terrorism from the cold war, the Washington Post said. OAO Yukos Oil Co.'s share price is being manipulated by senior Kremlin officials for their own benefit, the Business newspaper reported. Iraq's Prime Minister Ayad Allawi ordered troops from the country's newly formed army to lead an attack against Shiite Muslim militia in Najaf, the Washington Post reported. Lawyers for Golan Cipel, the Israeli who was given $110,000-a-year job by New Jersey Democratic Governor James McGreevey, said Cibel is heterosexual and didn't consent to any intimate contact with McGreevey, the NY Times said. New Jersey residents' approval of Governor McGreevey actually rose 2% to 45% after a recent flurry of scandalous allegations, according to the Star-Ledger. OAO Yukos Oil may "very likely" file for bankruptcy in the next few days unless Russia eases the pressure it's been applying, the Financial Times said. Posco's record earnings may not last until the first half of next year as the Korean steelmaker faces a number of threats such as higher oil prices, the Seoul Economic Daily reported. U.S. gas prices fell about 4.9 cents in the past three weeks, the AP reported, citing the Lundberg Survey of about 8,000 gas stations. Electronic Arts may be interested in buying U.K. publisher Eidos Plc as part of its European expansion, the Financial Times reported. Caterpillar workers rejected a six-year contract proposal, the AP reported. Allstate Corp., State Farm Mutual and other insurers may lose about $5 billion from Hurricane Charley, less than initially forecast, Bloomberg said. A weakened Hurricane Charley, the most powerful storm to hit the U.S. in 12 years, left Florida with deaths and damage estimated in the billions of dollars as it headed for the South Carolina coast this morning, Bloomberg reported. Crude oil prices may fall to $30/bbl. next year as concerns about supply disruptions in Iraq, Russia and Venezuela ease and OPEC boosts output, the group's President said. China will provide low-interest loans to cable companies to convert 100 million urban households to digital television by 2008, Bloomberg said. Crude oil futures in New York rose to a record on concern violence may spread in Venezuela, the fourth-largest exporter to the U.S., as the nation votes in a referendum that could remove President Chavez from office, Bloomberg reported.

Late-Night Trading

Asian indices are lower, -1.0% to -.50% on average.

S&P 500 indicated -.26%.

NASDAQ 100 indicated -.27%.

BOTTOM LINE: I expect U.S. stocks to open modestly lower in the morning on worries over Venezuelan political unrest and terrorism fears. However, equities will likely rally higher by day's end on short-covering and bargain-hunting. The Portfolio is 25% net long heading into tomorrow.

Sunday, August 15, 2004

Charts of the Week

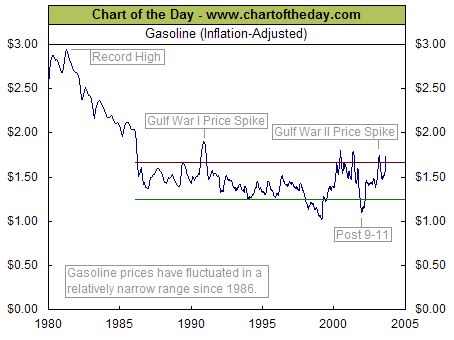

Bottom Line: As the top chart illustrates, gasoline prices on an inflation-adjusted basis are at the upper end of the trading range they have been in since 1986. Gas prices would have to soar another 70% to reach levels seen during the late 70's/early 80's. As well, the survey illustrated in the bottom chart seems to point to an overstatement by the media and some companies of the effects of gas prices on consumers at current levels.

Weekly Outlook

There are a few important economic reports and some significant corporate earnings reports scheduled for release this week. Economic reports this week include Empire Manufacturing, Housing Market Index, Consumer Price Index, Housing Starts, Building Permits, Industrial Production, Capacity Utilization, Initial Jobless Claims, Leading Indicators and Philadelphia Fed. Consumer Price Index, Housing Starts, Leading Indicators and Philly Fed. all have market-moving potential.

Lowe's(LOW), Kmart Holding(KMRT), BJ's Wholesale(BJ), Deere & Co.(DE), Home Depot(HD), J.C. Penney(JCP), Staples(SPLS), Applied Materials(AMAT), Brocade(BRCD), Intuit(INTU), Medtronic(MDT), Nortel(NT), Barnes & Noble(BKS), Limited Brands(LTD), The Gap(GPS), Nordstrom(JWN) and Novell(NOVL) are some of the more important companies that release quarterly earnings this week. There are also several other events that have market-moving potential. The CS First Boston Small Cap IT Services Conference and SEMI Book-to-Bill Report could also impact trading this week.

Bottom Line: I expect U.S. stocks to finish the week modestly higher, led by an oversold bounce in technology shares. However, equities will likely weaken the following week on terrorism fears ahead of the Republican Convention. I expect measures of investor anxiety to spike higher again during this period. I continue to believe stocks will make an intermediate-term bottom during the next 6 weeks, setting the stage for an exceptional fourth quarter. Short Funds with substantial gains for the year will likely begin to cover to protect profits. The Hennessee Hedge Fund US Short-biased Index rose 10.2% in July, its best performance since the terror-induced market sell-off of September 2001. Moreover, the 4 week average of Specialist Short Sales to Total Short Sales is at the lowest levels since at least the 1960's. I expect fundamental demand to snap back in the fourth quarter as political uncertainty lifts, terrorism fears subside, energy prices fall and businesses increase spending on capital equipment to take advantage of tax incentives before they expire at year-end. Many companies should beat their recently lowered earnings forecasts.

Lowe's(LOW), Kmart Holding(KMRT), BJ's Wholesale(BJ), Deere & Co.(DE), Home Depot(HD), J.C. Penney(JCP), Staples(SPLS), Applied Materials(AMAT), Brocade(BRCD), Intuit(INTU), Medtronic(MDT), Nortel(NT), Barnes & Noble(BKS), Limited Brands(LTD), The Gap(GPS), Nordstrom(JWN) and Novell(NOVL) are some of the more important companies that release quarterly earnings this week. There are also several other events that have market-moving potential. The CS First Boston Small Cap IT Services Conference and SEMI Book-to-Bill Report could also impact trading this week.

Bottom Line: I expect U.S. stocks to finish the week modestly higher, led by an oversold bounce in technology shares. However, equities will likely weaken the following week on terrorism fears ahead of the Republican Convention. I expect measures of investor anxiety to spike higher again during this period. I continue to believe stocks will make an intermediate-term bottom during the next 6 weeks, setting the stage for an exceptional fourth quarter. Short Funds with substantial gains for the year will likely begin to cover to protect profits. The Hennessee Hedge Fund US Short-biased Index rose 10.2% in July, its best performance since the terror-induced market sell-off of September 2001. Moreover, the 4 week average of Specialist Short Sales to Total Short Sales is at the lowest levels since at least the 1960's. I expect fundamental demand to snap back in the fourth quarter as political uncertainty lifts, terrorism fears subside, energy prices fall and businesses increase spending on capital equipment to take advantage of tax incentives before they expire at year-end. Many companies should beat their recently lowered earnings forecasts.

Subscribe to:

Posts (Atom)