There are some economic reports of note and a number of significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. - Empire Manufacturing

Tues. - Producer Price Index, Net Foreign Security Purchases, Industrial Production, Capacity Utilization, NAHB Housing Market Index

Wed. - Consumer Price Index, Housing Starts, Building Permits

Thur. - Initial Jobless Claims, Leading Indicators, Philly Fed.

Fri. - None of note

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. - BISYS Group(BSG), Commerce Bancorp(CBH), Eaton Corp.(ETN), Mattel(MAT), Sonic Corp.(SONC), Wachovia(WB)

Tues. - American Standard(ASD), AmSouth Bancorp(ASO), Charles Schwab(SCHB), CSX Corp.(CSX), EMC Corp.(EMC), Forest Labs(FRX), Freeport-McMoRan(FCX), Intel Corp.(INTC), IBM(IBM), Johnson & Johnson(JNJ), KeyCorp(KEY), Linear Technology(LLTC), Merrill Lynch(MER), Motorola(MOT), Novellus Systems(NVLS), Office Depot(ODP), State Street(STT), United Technologies(UTX), Wells Fargo(WFC), Yahoo!(YHOO)

Wed. - Abbott Labs(ABT), Advanced Micro Devices(AMD), Allstate(ALL), AMR Corp.(AMR), Apple Computer(AAPL), Boston Scientific(BSX), CDW Corp.(CDWC), E*Trade(ET), eBay(EBAY), General Dynamics(GD), Gilead Sciences(GILD), Illinois Toolworks(ITW), JPMorgan Chase(JPM), Juniper Networks(JNPR), Occidental Petroleum(OXY), Ryland Group(RYL), Seagate Technology(STX), St. Jude Medical(STJ)

Thur. - Armor Holdings(AH), Bank of America(BAC), Baxter Intl.(BAX), Broadcom Corp.(BRCM), Cerner Corp.(CERN), Citigroup(C), Coca-Cola(KO), Comerica(CMA), Eli Lilly(LLY), Freescale Semi(FSL), Google(GOOG), Honeywell(HON), McDonald’s Corp.(MCD), Nucor(NUE), Peabody Energy(BTU), Pfizer(PFE), SanDisk(SNDK), Southwest Air(LUV), United Parcel Service(UPS), United Health(UNH), Wyeth(WYE), Xilinx(XLNX), 3M Co.(MMM)

Fri. - Arch Coal(ACI), Caterpillar(CAT), Cheesecake Factory(CAKE), Golden West(GDW), Merck(MRK), Schering-Plough(SGP), Schlumberger(SLB)

Other events that have market-moving potential this week include:

Mon. - (TGT) sales release

Tue. - None of note

Wed. - None of note

Thur. - Deutsche Bank Energy Conference, (JBL) mid-year analyst meeting

Fri. - Deutsche Bank Energy Conference

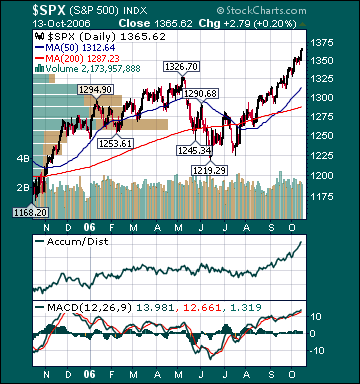

BOTTOM LINE: I expect US stocks to finish the week mixed as decelerating inflation readings, mostly positive economic data, mostly positive earnings reports, investment manager performance anxiety, short covering and less pessimism offsets profit-taking. My trading indicators are still giving bullish signals and the Portfolio is 100% net long heading into the week.