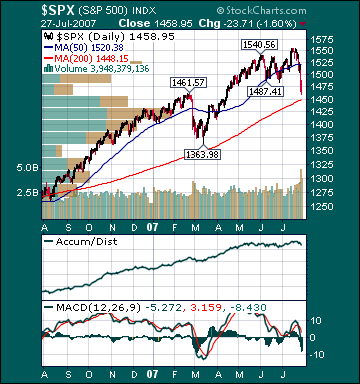

S&P 500 1,458.95 -4.90%*

*5-day % Change

Indices

S&P 500 1,458.95 -4.90%

DJIA 13,265.47 -4.22%

NASDAQ 2,562.24 -4.66%

Russell 2000 777.83 -7.0%

Wilshire 5000 14,663.63 -5.14%

Russell 1000 Growth 591.22 -3.79%

Russell 1000 Value 825.97 -4.78%

Morgan Stanley Consumer 707.25 -3.19%

Morgan Stanley Cyclical 1,033.69 -6.87%

Morgan Stanley Technology 637.95 -2.33%

Transports 5,039.17 -5.98%

Utilities 474.79 -7.24%

MSCI Emerging Markets 133.14 -5.80%

NYSE Cumulative A/D Line 68,092 -10.50%

Bloomberg New Highs-Lows Index -1056 -340.0%

Bloomberg Crude Oil % Bulls 35.0 -3.9%

CFTC Oil Large Speculative Longs 252,944 +2.5%

Total Put/Call 1.3 +5.7%

NYSE Arms 1.37 -35.98%

Volatility(VIX) 24.17 +42.60%

ISE Sentiment 132.0 unch.

AAII % Bulls 44.2 +5.8%

AAII % Bears 36.8 +.4%

Futures Spot Prices

Crude Oil 76.96 +1.84%

Reformulated Gasoline 211.25 -2.29%

Natural Gas 6.23 -4.83%

Heating Oil 207.32 -.95%

Gold 673.0 -3.64%

Base Metals 253.66 -5.1%

Copper 354.60 -4.46%

Economy

10-year US Treasury Yield 4.76% -19 basis points

4-Wk MA of Jobless Claims 308,500 -1.3%

Average 30-year Mortgage Rate 6.69% - 4 basis points

Weekly Mortgage Applications 609.0 -3.6%

Weekly Retail Sales +2.80%

Nationwide Gas $3.92/gallon -.08/gallon

US Cooling Demand Next 7 Days 12.0% above normal

ECRI Weekly Leading Economic Index 143.70 -.14%

US Dollar Index 81.0 +.82%

CRB Index 319.61 -1.49%

Best Performing Style

Large-Cap Growth -3.79%

Worst Performing Style

Small-Cap Value -6.64%

Telecom -.67%

Computer Services -1.57%

HMOs -1.67%

Defense -1.96%

Internet -2.30%

Lagging Sectors

Papers -8.65%

Gold -9.0%

Engineering & Construction -9.2%

Homebuilders -9.7%

Coal -10.4%

One-Week High-Volume Gainers

One-Week High-Volume Losers

- Advance 2Q GDP rose 3.4% versus estimates of a 3.2% gain and a .6% increase in 1Q.

- Advance 2Q Personal Consumption rose 1.3% versus estimates of a 1.5% gain and a 3.7% increase in 1Q.

- Advance 2Q GDP Price Index rose 2.7% versus estimates of a 3.4% increase and a 4.2% gain in 1Q.

- Advance 2Q Core PCE is estimated to rise 1.4% versus estimates of a 1.4% increase and a 2.4% rise in 1Q.

- Final July Univ. of

BOTTOM LINE: The US economy grew more than forecast last quarter, propelled by rising exports, commercials construction and government spending, Bloomberg said. The 3.4% gain in GDP was the best showing in more than a year. The Advance 2Q PCE Core, the Fed’s favorite gauge of inflation, rose only 1.4%, a meaningful decline from first quarter and the smallest increase in four years, even with oil in the $70s. Fed policy makers, including Bernanke, have said they prefer for the core pce to rise between 1-2%. Business Fixed Investment, which includes spending on commercial construction as well as equipment and software, rose at an 8.1% annual rate versus a 2.1% rate in 1Q. As I forecast back in March, when talk of an imminent recession was all the rage, growth came in above trend this quarter. I suspect growth will average around 3% for the remainder of the year as this quarter comes in slightly below trend and fourth quarter comes in slightly above trend. As well, inflation measures should continue to decelerate meaningfully, thus providing a very positive backdrop for stocks.

Confidence among US consumers rose in July as gasoline prices dropped from record highs and the labor market continued to show strength, Bloomberg said. The final index of confidence rose to 90.4 from 85.3 in June. The current conditions component of the index rose to 104.5 from 101.9 the prior month. The average price of a gallon of regular gas has fallen from $3.23 on May 23 to $2.92/gallon yesterday. I continue to believe both main gauges of consumer sentiment will reach new cycle highs over the intermediate-term as stocks rise further, gas prices fall meaningfully, inflation decelerates further, housing-related fears subside, wages continue to substantially outpace inflation and unemployment remains historically low.Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes

Late-Night Headlines

Bloomberg:

- Shares of AU Optronics Corp.(AUO), Taiwan’s largest marker of liquid-crystal displays, rose after the company reported a 33-fold jump in profit, beating analysts’ estimates, after prices for computer and TV screens increased.

- One measure of the

- Crocs(CROX), the maker of a colorful line of casual shoes, said second-quarter profit tripled as sales of its namesakes footwear and accessories climbed. The stock surged 15% in after-hours trading.

- Deckers Outdoor(DECK) reported second quarter sales increased 26.4%. The stock rose 9.4% in after-hours trading.

- The New York State Ethics Commission will investigate actions by Democratic Governor Eliot Spitzer’s staff to pressure state police to compile travel records on Senate Majority Leader Joseph Bruno.

- Bear Stearns(BSC) took control of debt securities held by one of its failed hedge funds to control their sale and guard against “further price declines.”

- US Treasury Secretary Henry Paulson said the decline in the subprime mortgage market reflects a reassessment of risk that doesn’t pose a threat to the economy. “I don’t think it poses any threat to the overall economy,” Paulson, a former CEO of Goldman Sachs(GS), said.

- Japan’s consumer prices declined for a fifth month, undermining the central bank’s case that inflation will take hold and interest rates need to be raised.

- Intel Corp.(INTC) broke antitrust laws by giving illegal rebates to computer makers to wrest sales away from rival Advanced Micro Devices(AMD), European regulators said.

- The yen fell from a three-month high against the US dollar on concern sliding Japanese stocks and declining consumer prices will cause the central bank to delay raising interest rates in coming months.

Wall Street Journal:

- The US government said China boosted transfers of sensitive military technology to Iran, harming efforts to pressure the Islamic Republic to abandon its nuclear program.

- The Federal Regulatory Commission accused collapsed hedge fund Amaranth Advisors LLC and two former traders of manipulating the US natural gas market early last year.

- Wireless provider Sprint Nextel Corp.(S) said it would include a range of Google Inc.’s(GOOG) Web and communications applications on its coming “WiMax” mobile devices, a boost for Sprint as it rolls out the new technology and a breakthrough for Google in the US wireless industry.

Business Week:

- Americans spend $41 billion a year on their pets, more than what they shell out for movies, video games and recorded music combined, citing research firm Packaged Facts.

Late Buy/Sell Recommendations

Citigroup:

- Upgraded (JWN) to Buy, target $58.

- Reiterated Buy on (RTN), target $68.

- Reiterated Buy on (GT), target $45.

- Reiterated Buy on (BWA), target $100.

- Upgraded (NLY) to Buy, target $16.

Business Week:

- Shares of Starbucks Corp.(SBUX) will probably emerge from a slump after hitting bottom last month. McAdams Wright Ragen’s Dan Gelman said the stock could climb 57% to $44 in the next 12 months.

Night Trading

Asian Indices are -2.25% to -1.5% on average.

S&P 500 futures +.32%.

NASDAQ 100 futures +.12%.

Morning Preview

US AM Market Call

NASDAQ 100 Pre-Market Indicator/Heat Map

Pre-market Commentary

Pre-market Stock Quote/Chart

Before the Bell CNBC Video(bottom right)

Global Commentary

WSJ Intl Markets Performance

Commodity Movers

Top 25 Stories

Top 20 Business Stories

Today in IBD

In Play

Bond Ticker

Economic Preview/Calendar

Daily Stock Events

Macro Calls

Upgrades/Downgrades

Rasmussen Business/Economy Polling

CNBC Guest Schedule

Earnings of Note

Company/EPS Estimate

- (AXL)/.61

- (BHI)/1.10

- (CVX)/2.28

- (CCU)/.45

- (CEG)/.73

- (FO)/1.44

- (IDXX)/.84

- (IR)/.95

- (ITT)/.90

- (MHS)/.78

- (MSTR)/1.20

Upcoming Splits

- (DIOD) 3-for-2

- (GMCR) 3-for-1

Economic Releases

8:30 am EST

- Advance 2Q GDP is estimated to rise 3.2% versus a .7% gain in 1Q.

- Advance 2Q Personal Consumption is estimated to rise 1.5% versus a 4.2% gain in 1Q.

- Advance 2Q GDP Price Index is estimated to rise 3.4% versus a 4.2% gain in 1Q.

- Advance 2Q Core PCE is estimated to rise 1.4% versus a 2.4% gain in 1Q.

10:00 am EST

-

Other Potential Market Movers

- The Morgan Keegan Insurance Conference could also impact trading today.