S&P 500 1,114.02 +.53%

NASDAQ 1,936.52 +1.31%

Leading Sectors

Software +2.37%

Boxmakers +1.93%

Biotech +1.69%

Lagging Sectors

Iron/Steel -1.46%

Oil Service -1.71%

Airlines -2.25%

Other

Crude Oil 53.54 -.24%

Natural Gas 6.80 -.09%

Gold 418.40 +.19%

Base Metals 113.12 -1.23%

U.S. Dollar 87.02 -.08%

10-Yr. T-note Yield 4.05% -.14%

VIX 14.71 -2.19%

Put/Call .77 -12.50%

NYSE Arms 1.03 -26.43%

After-hours Movers

CKFR +5.63% after beating 1Q estimates and raising 2Q forecast.

TXN +5.07% after beating 3Q estimates, reiterating 4Q guidance and making positive comments.

LF -36.81% after cutting 3Q/04 forecast.

CGNX -7.03% after meeting 3Q estimates and lowering 4Q outlook.

Recommendations

Goldman Sachs upgraded MMM to Outperform. Goldman reiterated Underperform on DJ and Outperform on DEX, BBY, KO.

After-hours News

U.S. stocks finished higher today as energy prices declined and investors became more optimistic on technology shares. After the close, International Business Machines said third-quarter sales rose to $23.4 billion from $21.5 billion in the same period a year earlier, Bloomberg said. Texas Instruments said profit rose to $563 million as third-quarter sales reached their highest point for the period in nine years, Bloomberg reported. Lockheed Martin called on the U.S. Air Force to cancel at least four contracts worth more than $6 billion awarded to Boeing after a former Pentagon official told federal prosecutors she improperly favored Boeing, Bloomberg said. The FDA plans to meet with outside medical advisers as early as January to discuss any questions about the safety of Pfizer's painkillers, Celebrex and Bextra, Bloomberg said. Robert Mondavi said it is considering an unsolicited offer to buy the company, Bloomberg reported. Marsh & McLennan said the payments it will forgo because of a lawsuit by New York Attorney General Spitzer amounted to $845 million, or 7% of revenue last year, Bloomberg reported.

BOTTOM LINE: The Portfolio finished substantially higher today on strength in my wireless, internet and telecom equipment longs. I added a few new longs from various sectors in the afternoon, leaving the Portfolio 125% net long. One of my new longs is KMRT and I am using a $89.25 stop-loss on this position. The tone of the market improved throughout the afternoon as technology stocks outperformed and the advance/decline line improved. It is quite possible the large 4Q rally I thought would begin within the next 10 days has already begun. However, I am not ruling out the possibility of one more pull-back in the near-term. I continue to believe the major U.S. indices will post double digit returns for the quarter as economic growth accelerates, political uncertainty and negativity subsides, domestic terrorism fears diminish, interest rates remain low, inflation stays contained and energy prices fall. Technology stocks should continue to outperform in this environment.

Monday, October 18, 2004

Mid-day Update

S&P 500 1,111.48 +.28%

NASDAQ 1,925.82 +.75%

Leading Sectors

Software +1.73%

Biotech +1.4%

Retail +1.31%

Lagging Sectors

Papers -1.27%

Airlines -1.49%

Oil Service -1.81%

Other

Crude Oil 53.46 -2.69%

Natural Gas 6.79 +1.21%

Gold 417.60 -.60%

Base Metals 113.12 -1.23%

U.S. Dollar 87.10 +.01%

10-Yr. T-note Yield 4.06% +.14%

VIX 14.94 -.66%

Put/Call .79 -10.23%

NYSE Arms 1.16 -17.14%

Market Movers

MMC -8.8% on continuing worries over Spitzer probe.

CHKP +16.4% after beating 3Q estimates and raising 4Q/04 guidance.

MMM -4.4% after missing 3Q estimates, lowering 4Q guidance and Prudential downgrade to Neutral.

ODSY -43.0% after cutting 3Q/04 forecasts and announcing Dept. of Justice civil investigation.

SEM +23.0% after agreeing to be taken private for $1.82 billion excluding debt.

JQH +15.4% after saying it had received a proposal from Barcelo Crestline Corp. to acquire it for $13.00 in cash per class A share.

APOL +4.5% on Morgan Stanley upgrade to Overweight, target $85.

PLMO +7.9% on JP Morgan upgrade to Overweight.

ICUI -16.5% after missing 3Q estimates.

CHE -8.6% and HALTED, boosting forecast, indicated $53-56.

BGG -6.9% after lowering 1Q/05 forecast.

MNC -8.8% after cutting 3Q forecast.

TZOO -5.8% after American Technology downgrade to Sell.

ASD -4.2% after missing 3Q estimates and lowering 4Q forecast.

GIVN -3.7% on negative Barron's mention.

Economic Data

NAHB Housing Market Index for October rose to 72 versus estimates of 68 and a reading of 67 in September.

Recommendations

Goldman Sachs reiterated Outperform on INTC, AMD, MDT, MET, FS and IGT. Goldman reiterated Underperform on EK and FRX. Citi SmithBarney reiterated Buy on MDT, target $62. Citi reiterated Buy on GDT, target $55. Citi reiterated Buy on AMGN, target $90. Citi raised VECO to Buy, target $26. Citi reiterated Buy on FON, target $22. Citi reiterated Buy on L, target $11.50. Citi reiterated Buy on WB, target $53. Citi reiterated Buy on WMT, target $65. Citi reiterated Buy on PEG, target $45. OSUR raised to Outperform at Thomas Weisel, target $11. VRTS rated Outperform at CSFB, target $25. PLMO raised to Overweight at JP Morgan. VRX rated Buy at Merrill Lynch, target $32. PEP raised to Buy at Merrill, target $55. KZL raised to Outperform at Bear Stearns, target $54.

Mid-day News

U.S. stocks are mostly higher mid-day on a decline in energy prices. Kraft Foods is considering selling Oscar Mayer meats and Post cereals, the NY Post reported. Increased terrorist attacks in Iraq are aimed at U.S. President Bush personally, as terrorists seek to keep him from getting re-elected, Russian President Putin said, the Itar-Tass news agency reported. Blue Coat Systems, whose devices thwart computer viruses and filter Internet content, is enhancing its proxy servers with software to block spyware and adware programs, which disrupt computer users' Internet activity, the Wall Street Journal reported. Video-game makers have created a format that allows advertisers to insert changeable information into "virtual billboards" within the game, the Wall Street Journal reported. Fannie Mae's plan to report third quarter earnings by Nov. 15 instead of its typical mid-October timeframe suggests the company will have to restate profit, the Financial Times said. Kojo Annan, the son of United Nations Secretary-General Kofi Annan, is among people and companies under investigation by a federal grand jury looking into the massive corruption in Iraq's $64 billion UN oil-for-food program, the NY Post reported. Lexmark Intl., the No.2 maker of computer printers, said third-quarter profit rose 50% on a tax benefit and sales of higher-profit machines, Bloomberg reported. SynCardia Systems won FDA approval to sell an artificial heart, the first such device available for commercial use in the U.S., Bloomberg said. Kmart Holding named Yum! Brands executive Lewis as CEO, replacing Julian Day, to improve retail operations, Bloomberg said. Harmony Gold Mining made a hostile offer to buy Gold Fields for $8.2 billion in stock to create the world's largest producer of the precious metal, Bloomberg reported. Crude oil is dropping after reaching $55.33/bbl. in NY amid concern that rising prices will reduce the growth of demand for petroleum products, Bloomberg reported.

BOTTOM LINE: The Portfolio is higher mid-day on strength in my wireless, internet and retail longs. I added a few new longs this morning, bringing the Portfolio's market exposure to 100% net long. One of my new longs is ARO and I am using a stop-loss of $28 on this position. The tone of the market is mildly positive. I continue to expect technology stocks to outperform at least through year-end. It is a big positive to see gasoline futures with a significant decline. On the negative-side, measures of investor anxiety are falling and the advance/decline line is relatively weak. I expect U.S. stocks to rise modestly from currently levels into the afternoon on short-covering and optimism over a possible peak in energy prices.

NASDAQ 1,925.82 +.75%

Leading Sectors

Software +1.73%

Biotech +1.4%

Retail +1.31%

Lagging Sectors

Papers -1.27%

Airlines -1.49%

Oil Service -1.81%

Other

Crude Oil 53.46 -2.69%

Natural Gas 6.79 +1.21%

Gold 417.60 -.60%

Base Metals 113.12 -1.23%

U.S. Dollar 87.10 +.01%

10-Yr. T-note Yield 4.06% +.14%

VIX 14.94 -.66%

Put/Call .79 -10.23%

NYSE Arms 1.16 -17.14%

Market Movers

MMC -8.8% on continuing worries over Spitzer probe.

CHKP +16.4% after beating 3Q estimates and raising 4Q/04 guidance.

MMM -4.4% after missing 3Q estimates, lowering 4Q guidance and Prudential downgrade to Neutral.

ODSY -43.0% after cutting 3Q/04 forecasts and announcing Dept. of Justice civil investigation.

SEM +23.0% after agreeing to be taken private for $1.82 billion excluding debt.

JQH +15.4% after saying it had received a proposal from Barcelo Crestline Corp. to acquire it for $13.00 in cash per class A share.

APOL +4.5% on Morgan Stanley upgrade to Overweight, target $85.

PLMO +7.9% on JP Morgan upgrade to Overweight.

ICUI -16.5% after missing 3Q estimates.

CHE -8.6% and HALTED, boosting forecast, indicated $53-56.

BGG -6.9% after lowering 1Q/05 forecast.

MNC -8.8% after cutting 3Q forecast.

TZOO -5.8% after American Technology downgrade to Sell.

ASD -4.2% after missing 3Q estimates and lowering 4Q forecast.

GIVN -3.7% on negative Barron's mention.

Economic Data

NAHB Housing Market Index for October rose to 72 versus estimates of 68 and a reading of 67 in September.

Recommendations

Goldman Sachs reiterated Outperform on INTC, AMD, MDT, MET, FS and IGT. Goldman reiterated Underperform on EK and FRX. Citi SmithBarney reiterated Buy on MDT, target $62. Citi reiterated Buy on GDT, target $55. Citi reiterated Buy on AMGN, target $90. Citi raised VECO to Buy, target $26. Citi reiterated Buy on FON, target $22. Citi reiterated Buy on L, target $11.50. Citi reiterated Buy on WB, target $53. Citi reiterated Buy on WMT, target $65. Citi reiterated Buy on PEG, target $45. OSUR raised to Outperform at Thomas Weisel, target $11. VRTS rated Outperform at CSFB, target $25. PLMO raised to Overweight at JP Morgan. VRX rated Buy at Merrill Lynch, target $32. PEP raised to Buy at Merrill, target $55. KZL raised to Outperform at Bear Stearns, target $54.

Mid-day News

U.S. stocks are mostly higher mid-day on a decline in energy prices. Kraft Foods is considering selling Oscar Mayer meats and Post cereals, the NY Post reported. Increased terrorist attacks in Iraq are aimed at U.S. President Bush personally, as terrorists seek to keep him from getting re-elected, Russian President Putin said, the Itar-Tass news agency reported. Blue Coat Systems, whose devices thwart computer viruses and filter Internet content, is enhancing its proxy servers with software to block spyware and adware programs, which disrupt computer users' Internet activity, the Wall Street Journal reported. Video-game makers have created a format that allows advertisers to insert changeable information into "virtual billboards" within the game, the Wall Street Journal reported. Fannie Mae's plan to report third quarter earnings by Nov. 15 instead of its typical mid-October timeframe suggests the company will have to restate profit, the Financial Times said. Kojo Annan, the son of United Nations Secretary-General Kofi Annan, is among people and companies under investigation by a federal grand jury looking into the massive corruption in Iraq's $64 billion UN oil-for-food program, the NY Post reported. Lexmark Intl., the No.2 maker of computer printers, said third-quarter profit rose 50% on a tax benefit and sales of higher-profit machines, Bloomberg reported. SynCardia Systems won FDA approval to sell an artificial heart, the first such device available for commercial use in the U.S., Bloomberg said. Kmart Holding named Yum! Brands executive Lewis as CEO, replacing Julian Day, to improve retail operations, Bloomberg said. Harmony Gold Mining made a hostile offer to buy Gold Fields for $8.2 billion in stock to create the world's largest producer of the precious metal, Bloomberg reported. Crude oil is dropping after reaching $55.33/bbl. in NY amid concern that rising prices will reduce the growth of demand for petroleum products, Bloomberg reported.

BOTTOM LINE: The Portfolio is higher mid-day on strength in my wireless, internet and retail longs. I added a few new longs this morning, bringing the Portfolio's market exposure to 100% net long. One of my new longs is ARO and I am using a stop-loss of $28 on this position. The tone of the market is mildly positive. I continue to expect technology stocks to outperform at least through year-end. It is a big positive to see gasoline futures with a significant decline. On the negative-side, measures of investor anxiety are falling and the advance/decline line is relatively weak. I expect U.S. stocks to rise modestly from currently levels into the afternoon on short-covering and optimism over a possible peak in energy prices.

Monday Watch

Earnings of Note

Company/Estimate

MMM/.98

CHKP/.25

CKFR/.26

DPH/-.12

ET/.18

FRX/.76

IBM/1.14

ITT/1.15

LXK/.97

LNCR/.69

MCHP/.29

SWK/.71

TXN/.27

Splits

NUE 2-for-1

Economic Data

NAHB Housing Market Index for October estimated at 68 versus 68 in September.

Weekend Recommendations

Wall Street Week w/Fortune had guests that were positive on IMGC, CEG, ZMH and IACI. Cashin' In had guests that were positive on IPR, TROW, TXN and mixed on C. Louis Rukeyser's Wall Street had guests that were positive on NOVL, SIRI, XMSR, MSFT, TWX, SEE and IMA. Barron's had positive comments on NVS, ACN, ISTA, DOVP and negative comments on GIVN, MNKD, INTC. Goldman Sachs reiterated Outperform on AMGN, ALL, AIG, RE, ENG, UDR, ASN and MUR. Goldman reiterated Underperform on PPS, PSA, EQR and MMC.

Weekend News

Abercrombie & Fitch agreed to stop using Australian wool after being pressured by an animal rights group, People for the Ethical Treatment of Animals, the Australian Broadcasting Corp. said. Citigroup and American Express blocked their credit cards in the U.K. from being used to pay for online gambling to prevent fraud and reduce indebtedness, the Financial Times reported. Hundreds of British soldiers may be moved to Baghdad within a few weeks to help boost U.S.-led operations in the run-up to Iraq's elections in January, the London-based Times reported. About 70,000 refugees in Sudan's western Darfur region have died from malnutrition and disease, the NY Times reported, citing the World Health Organization. Senator Kerry and President Bush's campaign commercials use the most ominous imagery seen in presidential ads in a generation, the NY Times said, citing analysts and historians. California's Bay Area residents are experiencing the cleanest air quality in 35 years, the San Jose Mercury News reported. Iraq's power grid now has more megawatts than before the U.S.-led invasion, which should boost Iraqis trust in their government, the NY Times reported. South Korea plans to extend the deployment of its troops in Iraq by a year, Yonhap news reported. Airbus SAS CEO Forgeard said he is seeking a U.S. partner to help in a $23 billion bid to supply the U.S. Air Force with aircraft-refueling tanker planes, the Sunday Telegraph said. Merrill Lynch and Morgan Stanley may be forced to merge with larger commercial firms as the two investment banks' share prices have declined by 20% from their 2004 highs, the NY Times reported. More than 25,000 poll watchers are being mobilized across the U.S. to scrutinize the Nov.2 presidential election for voting irregularities, the LA Times reported. Ford will offer Sirius Satellite Radio as an option in more of its cars and trucks, the NY Times said. Afghan President Karzai maintained his lead over the main opposition candidate Qanooni in early results from the Oct. 9 presidential election, Bloomberg reported. An estimated 75% of the more than 10 million Afghans eligible to vote took part in the country's first direct presidential election, just three years after the Taliban were ousted in the U.S.-led war on terror, Bloomberg said. SBC Communications is offering new and existing customers of its high-speed Internet service free wireless Web access through April to boost demand for its offerings, Bloomberg reported.

Late-Night Trading

Asian indices are mostly lower, -.50% to +.25% on average.

S&P 500 indicated +.01%.

NASDAQ 100 indicated +.21%

BOTTOM LINE: I expect U.S. stocks to open modestly higher in the morning on short-covering and follow-through on Friday's rally. The Portfolio is 75% net long heading into the week.

Company/Estimate

MMM/.98

CHKP/.25

CKFR/.26

DPH/-.12

ET/.18

FRX/.76

IBM/1.14

ITT/1.15

LXK/.97

LNCR/.69

MCHP/.29

SWK/.71

TXN/.27

Splits

NUE 2-for-1

Economic Data

NAHB Housing Market Index for October estimated at 68 versus 68 in September.

Weekend Recommendations

Wall Street Week w/Fortune had guests that were positive on IMGC, CEG, ZMH and IACI. Cashin' In had guests that were positive on IPR, TROW, TXN and mixed on C. Louis Rukeyser's Wall Street had guests that were positive on NOVL, SIRI, XMSR, MSFT, TWX, SEE and IMA. Barron's had positive comments on NVS, ACN, ISTA, DOVP and negative comments on GIVN, MNKD, INTC. Goldman Sachs reiterated Outperform on AMGN, ALL, AIG, RE, ENG, UDR, ASN and MUR. Goldman reiterated Underperform on PPS, PSA, EQR and MMC.

Weekend News

Abercrombie & Fitch agreed to stop using Australian wool after being pressured by an animal rights group, People for the Ethical Treatment of Animals, the Australian Broadcasting Corp. said. Citigroup and American Express blocked their credit cards in the U.K. from being used to pay for online gambling to prevent fraud and reduce indebtedness, the Financial Times reported. Hundreds of British soldiers may be moved to Baghdad within a few weeks to help boost U.S.-led operations in the run-up to Iraq's elections in January, the London-based Times reported. About 70,000 refugees in Sudan's western Darfur region have died from malnutrition and disease, the NY Times reported, citing the World Health Organization. Senator Kerry and President Bush's campaign commercials use the most ominous imagery seen in presidential ads in a generation, the NY Times said, citing analysts and historians. California's Bay Area residents are experiencing the cleanest air quality in 35 years, the San Jose Mercury News reported. Iraq's power grid now has more megawatts than before the U.S.-led invasion, which should boost Iraqis trust in their government, the NY Times reported. South Korea plans to extend the deployment of its troops in Iraq by a year, Yonhap news reported. Airbus SAS CEO Forgeard said he is seeking a U.S. partner to help in a $23 billion bid to supply the U.S. Air Force with aircraft-refueling tanker planes, the Sunday Telegraph said. Merrill Lynch and Morgan Stanley may be forced to merge with larger commercial firms as the two investment banks' share prices have declined by 20% from their 2004 highs, the NY Times reported. More than 25,000 poll watchers are being mobilized across the U.S. to scrutinize the Nov.2 presidential election for voting irregularities, the LA Times reported. Ford will offer Sirius Satellite Radio as an option in more of its cars and trucks, the NY Times said. Afghan President Karzai maintained his lead over the main opposition candidate Qanooni in early results from the Oct. 9 presidential election, Bloomberg reported. An estimated 75% of the more than 10 million Afghans eligible to vote took part in the country's first direct presidential election, just three years after the Taliban were ousted in the U.S.-led war on terror, Bloomberg said. SBC Communications is offering new and existing customers of its high-speed Internet service free wireless Web access through April to boost demand for its offerings, Bloomberg reported.

Late-Night Trading

Asian indices are mostly lower, -.50% to +.25% on average.

S&P 500 indicated +.01%.

NASDAQ 100 indicated +.21%

BOTTOM LINE: I expect U.S. stocks to open modestly higher in the morning on short-covering and follow-through on Friday's rally. The Portfolio is 75% net long heading into the week.

Sunday, October 17, 2004

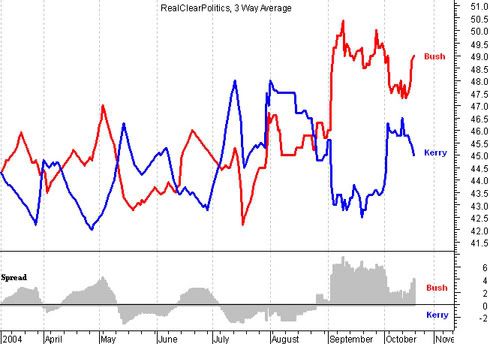

Chart of the Week

2004 Presidential Race - RealClearPolitics Poll Average

RCP Poll Average (10/13 - 10/16): Bush 49.0%, Kerry 45.0%, Nader 1.7% | Bush +4.0

Bottom Line: The above graph is an average of all the major Presidential polls from RealClearPolitics.com. It is my contention that the Presidential election is having a much more profound effect on the economy than is generally believed. Historically bitter and divisive rhetoric, 24-7 negative media coverage, domestic terrorism fears and uncertainty over the very different directions the candidates plan to lead the country are having a significant impact on the psychology of consumers and corporate decision-makers.

RCP Poll Average (10/13 - 10/16): Bush 49.0%, Kerry 45.0%, Nader 1.7% | Bush +4.0

Bottom Line: The above graph is an average of all the major Presidential polls from RealClearPolitics.com. It is my contention that the Presidential election is having a much more profound effect on the economy than is generally believed. Historically bitter and divisive rhetoric, 24-7 negative media coverage, domestic terrorism fears and uncertainty over the very different directions the candidates plan to lead the country are having a significant impact on the psychology of consumers and corporate decision-makers.

Weekly Outlook

There are a number of important economic reports and significant corporate earnings reports scheduled for release this week. Economic reports include Net Foreign Security Purchases(Mon.), Housing Market Index(Mon.), Consumer Price Index(Tues.), CPI Ex Food & Energy(Tues.), Housing Starts(Tues.), Building Permits(Tues.), Initial Jobless Claims(Thur.), Continuing Claims(Thur.), Leading Indicators(Thur.) and Philly Fed.(Thur.). The CPI, Housing Starts, Jobless Claims, Leading Indicators and Philly Fed. all have market-moving potential.

Intl. Business Machines(IBM-Mon.), Lexmark Intl.(LXK-Mon.), Texas Instruments(TXN-Mon.), 3M(MMM-Mon.), Altria(MO-Tues.), Electronic Arts(ERTS-Tues.), Motorola(MOT-Tues.), Taser Intl.(TASR-Tues.), Boston Scientific(BSX-Tue.), McDonald's(MCD-Tues.), JP Morgan(JPM-Wed.), EBay(EBAY-Wed.), Harrah's Entertainment(HET-Wed.), Honeywell(HON-Wed.), United Technologies(UTX-Wed.), Microsoft(MSFT-Thur.), SBC Communications(SBC-Thur.), Caterpillar(CAT-Thur.), Merck(MRK-Thur.), American Intl. Group(AIG-Thur.), Coca Kola(KO-Thur.) and Amazon(AMZN-Fri.) are some of the more important companies that release quarterly earnings this week. There are also some other events that have market-moving potential. The Semi Book-to-Bill report(Mon.), Fed's Poole speaking(Tues.), Fed's Greenspan speaking(Tues.), Fed's Poole speaking(Thur.) could also impact trading this week.

Bottom Line: I expect U.S. stocks to finish the week mixed-to-weaker as worries over earnings, energy prices, lawsuits and politics offset diminishing domestic terrorism fears, optimism over future economic growth and an improvement of the big picture in Iraq. I continue to believe the major indices are consolidating recent gains before another more significant move higher, beginning within the next 10 days. Oil above $60/bbl., a major terrorist attack or a delay in the outcome of the Presidential election would change my positive view for this quarter. My short-term trading indicators are giving mixed signals and the Portfolio is 75% net long heading into the week.

Intl. Business Machines(IBM-Mon.), Lexmark Intl.(LXK-Mon.), Texas Instruments(TXN-Mon.), 3M(MMM-Mon.), Altria(MO-Tues.), Electronic Arts(ERTS-Tues.), Motorola(MOT-Tues.), Taser Intl.(TASR-Tues.), Boston Scientific(BSX-Tue.), McDonald's(MCD-Tues.), JP Morgan(JPM-Wed.), EBay(EBAY-Wed.), Harrah's Entertainment(HET-Wed.), Honeywell(HON-Wed.), United Technologies(UTX-Wed.), Microsoft(MSFT-Thur.), SBC Communications(SBC-Thur.), Caterpillar(CAT-Thur.), Merck(MRK-Thur.), American Intl. Group(AIG-Thur.), Coca Kola(KO-Thur.) and Amazon(AMZN-Fri.) are some of the more important companies that release quarterly earnings this week. There are also some other events that have market-moving potential. The Semi Book-to-Bill report(Mon.), Fed's Poole speaking(Tues.), Fed's Greenspan speaking(Tues.), Fed's Poole speaking(Thur.) could also impact trading this week.

Bottom Line: I expect U.S. stocks to finish the week mixed-to-weaker as worries over earnings, energy prices, lawsuits and politics offset diminishing domestic terrorism fears, optimism over future economic growth and an improvement of the big picture in Iraq. I continue to believe the major indices are consolidating recent gains before another more significant move higher, beginning within the next 10 days. Oil above $60/bbl., a major terrorist attack or a delay in the outcome of the Presidential election would change my positive view for this quarter. My short-term trading indicators are giving mixed signals and the Portfolio is 75% net long heading into the week.

Market Week in Review

S&P 500 1,108.20 -1.24%

Click here for the Weekly Wrap by Briefing.com

Bottom Line: Market action last week was mostly negative as insurance and base metal stocks led the major indices lower. Considering energy's continuing rise, a tightening of the Presidential polls, the debacle in the insurance sector and mixed economic data, the major indices relatively muted declines likely disappointed the Bears. NY Attorney General Spitzer's attacks on the insurance industry, while warranted, unfortunately resulted in major losses for investors and will likely cause future job losses in the industry. It is becoming harder and harder to find sectors to investment in that are not under major legal duress, which is a significant burden on the U.S. economy. In my opinion, executives need to be held more personally liable for their illegal actions and the companies themselves less liable, to minimized job losses and investor pain. The carnage in the base metal stocks, as a result of reports that China's economy is slowing, appears overdone to me. Barring a recession brought on by higher energy prices, which I do not currently anticipate, these stocks shouldn't head substantially lower from current levels. On the positive side, most measures of investor anxiety rose, interest rates fell, the CRB Index declined, technology stocks outperformed and the advance/decline line only fell modestly.

Click here for the Weekly Wrap by Briefing.com

Bottom Line: Market action last week was mostly negative as insurance and base metal stocks led the major indices lower. Considering energy's continuing rise, a tightening of the Presidential polls, the debacle in the insurance sector and mixed economic data, the major indices relatively muted declines likely disappointed the Bears. NY Attorney General Spitzer's attacks on the insurance industry, while warranted, unfortunately resulted in major losses for investors and will likely cause future job losses in the industry. It is becoming harder and harder to find sectors to investment in that are not under major legal duress, which is a significant burden on the U.S. economy. In my opinion, executives need to be held more personally liable for their illegal actions and the companies themselves less liable, to minimized job losses and investor pain. The carnage in the base metal stocks, as a result of reports that China's economy is slowing, appears overdone to me. Barring a recession brought on by higher energy prices, which I do not currently anticipate, these stocks shouldn't head substantially lower from current levels. On the positive side, most measures of investor anxiety rose, interest rates fell, the CRB Index declined, technology stocks outperformed and the advance/decline line only fell modestly.

Subscribe to:

Posts (Atom)