Click here for Market Outlook by CNBC.

Click here for Stocks in Focus for Monday by MarketWatch.com.

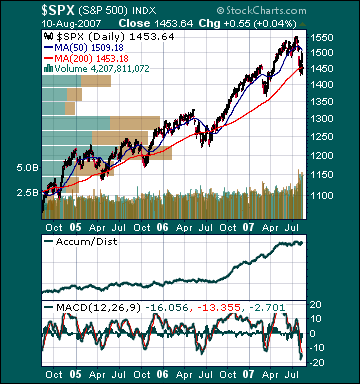

There are several economic reports of note and some significant corporate earnings reports scheduled for release this week.

Economic reports for the week include:

Mon. – Advance Retail Sales, Business Inventories

Tues. – Trade Balance, Producer Price Index, IBD/TIPP Economic Optimism, weekly retail sales

Wed. – Weekly MBA mortgage applications report, Consumer Price Index, Empire Manufacturing, weekly EIA energy inventory report, NET Long-term TIC Flows, Industrial Production, Capacity Utilization, NAHB Housing Market Index

Thur. – Housing Starts, Building Permits, Initial Jobless Claims, Philly Fed

Fri. –

Some of the more noteworthy companies that release quarterly earnings this week are:

Mon. – Blackstone Group(BX), Bob Evans(BOBE), DeVry Inc.(DV), Netease.com(NTES), SYSCO Corp.(SYY)

Tues. – Agilent(A), Applied Materials(AMAT), Dillard’s(DDS), Fortress Investment Group(FIG), Fossil Inc.(FOSL), Harman Intl.(HAR), Home Depot(HD), TJX Cos(TJX), Wal-Mart Stores(WMT)

Wed. – Affiliated Computer Services(ACS), Daktronics(DAKT), Deere(DE), Dick’s Sporting Goods(DKS), Longs Drug(LDG), Macy’s(M), Network Applicance(NTAP), PetSmart Inc.(PETM), Salesforce.com(CRM), Sara Lee(SLE)

Thur. – Autodesk(ADSK), Estee Lauder(EL), Grube & Ellis(GBE), Guess ?(GES), Hewlett-Packard(HPQ), JC Penney(JCP), Kohl’s Corp.(KSS), Nordstrom(JWN), Red Robin(RRGB), Zumiez(ZUMZ)

Fri. – Focus Media(FMCN), JM Smucker(SJM)

Other events that have market-moving potential this week include:

Mon. – Keefe Bruyette & Woods Bank Conference

Tue. – CSFB Communications Conference, UBS Engineering & Construction Conference, Jeffries Industrials Conference, Keefe Bruyette & Woods Bank Conference

Wed. – CSFB Communications Conference, (YUM) Investor Day

Thur. – CSFB Communications Conference, (IVGN) Annual Investor Day

Fri. – None of note