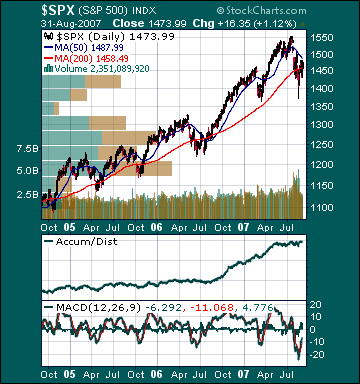

S&P 500 1,473.99 -.36%*

*5-day Change

Indices

S&P 500 1,473.99 -.36%

DJIA 13,357.74 -.16%

NASDAQ 2,596.36 +.76%

Russell 2000 792.86 -.76%

Wilshire 5000 14,807.65 -.32%

Russell 1000 Growth 594.19 +.46%

Russell 1000 Value 824.45 -1.04%

Morgan Stanley Consumer 714.29 -.67%

Morgan Stanley Cyclical 1,027.35 -.44%

Morgan Stanley Technology 636.04 +1.0%

Transports 4,878.75 -.76%

Utilities 484.79 -2.81%

MSCI Emerging Markets 134.35 +3.65%

Sentiment/Internals

NYSE Cumulative A/D Line 65,004 -.58%

Bloomberg New Highs-Lows Index -137 +5.52%

Bloomberg Crude Oil % Bulls n/a

CFTC Oil Large Speculative Longs 202,843 -2.0%

Total Put/Call 1.03 -3.74%

NYSE Arms .59 -4.83%

Volatility(VIX) 23.38 +12.83%

ISE Sentiment 122.0 +6.1%

AAII % Bulls 40.30 -2.37%

AAII % Bears 46.27 +7.31%

Futures Spot Prices

Crude Oil 73.88 +4.12%

Reformulated Gasoline 196.55 +3.15%

Natural Gas 5.43 -4.42%

Heating Oil 205.70 +2.20%

Gold 682.0 +.69%

Base Metals 242.78 +3.77%

Copper 340.20 +.98%

Economy

10-year US Treasury Yield 4.53% -9 basis points

4-Wk MA of Jobless Claims 324,500 +1.9%

Average 30-year Mortgage Rate 6.45% -7 basis points

Weekly Mortgage Applications 615.20 -4.0%

Weekly Retail Sales +2.3%

Nationwide Gas $2.77/gallon -.01/gallon

US Cooling Demand Next 7 Days 17.0% above normal

ECRI Weekly Leading Economic Index 139.20 -.36%

US Dollar Index 80.81 +.15%

CRB Index 308.76 +1.02%

Best Performing Style

Large-cap Growth +.46%

Worst Performing Style

Large-cap Value -1.04%

Leading Sectors

Computer Hardware +2.45%

Engineering & Construction +2.02%

Wireless +1.99%

Computer Services +1.87%

Disk Drives +1.79%

Lagging Sectors

Coal -1.71%

Insurance -2.46%

Banks -2.79%

Utilities -2.81%

Homebuilders -3.28%

Bloomberg:

- President Bush today pledged to help people who’ve fallen behind in their mortgages keep their homes and to tighten safeguards against predatory lending, while rejecting a bailout for “speculators.”

- Senator Charles Schumer said Treasury Secretary Henry Paulson expressed interest in allowing Fannie Mae(FNM) and Freddie Mac(FRE) to exceed limits on their combined $1.4 trillion mortgage portfolios in order to help distressed borrowers refinance their home loans.

- The Brazilian real gained as a pledge by President Bush to help delinquent US mortgage holders keep their homes eased concern that the housing slump will throttle global economic growth.

- The risk of owning corporate bonds fell 3.5 basis points today to 69 basis points, according to traders of credit-default swaps.

- A benchmark subprime mortgage ABX index tied to risky home loans made in last year’s second half is rising 9.5% today.

- Federal Reserve Chairman Ben Bernanke, in his first public remarks in six weeks, said the central bank will do what’s needed to prevent this month’s credit market rout from undoing the six-year expansion.

- Investors added $83 million to high-yield bond funds, the first infusion in 12 weeks, seeking to capitalize on gains in high-risk debt, JPMorgan Chase(JPM) said, citing AMG Data Services.

- Norman Hsu, a Democratic fundraiser wanted for fraud, turned himself in to California authorities, according to a statement by his lawyer.

- Cree Inc.(CREE) shares jumped the most since June and options trading surged on speculation that the maker of semiconductors that light dashboards and cellular phones may be acquired by General Electric(GE).

- Intel Corp.(INTC) rose to its highest in six weeks after Dell Inc.(DELL) profit beat estimates and a Caris & Co. analyst said Intel’s memory chip venture will probably be approved by regulators.

Wall Street Journal:

- Russian officials are pleased that the country’s capital markets seem to have withstood a $10 billion net outflow in the past three weeks without negative consequences.

- Vulture Funds Start Circling Credit Markets.

-

NY Post:

- Apple Inc.(AAPL) is working with record labels to offer ringtones on iPhones from its iTunes online music service.

- Personal Income for July rose .5% versus estimates of a .3% gain and a .4% rise in June.

- Personal Spending for July rose .4% versus estimates of a .3% increase and an upwardly revised .2% gain in June.

- The PCE Core for July rose .1% versus estimates of a .2% increase and an upwardly revised .2% increase in June.

- The Chicago PMI for August rose to 53.8 versus estimate of 53.0 and 53.4 in July.

- Factory Orders for July rose 3.7% versus estimates of a 3.3% gain and an upwardly revised 1.0% increase in June.

-

BOTTOM LINE: Consumer spending in the

Orders placed with

Market Snapshot Commentary

Market Performance Summary

Style Performance

Sector Performance

WSJ Data Center

Top 20 Biz Stories

IBD Breaking News

Movers & Shakers

Upgrades/Downgrades

In Play

NYSE Unusual Volume

NASDAQ Unusual Volume

Hot Spots

Option Dragon

NASDAQ 100 Heatmap

DJIA Quick Charts

Chart Toppers

Intraday Chart/Quote

Dow Jones Hedge Fund Indexes